SUV’s continue to drive growth in Europe’s Big 5 markets

- Big 5 markets registrations totalled 1.36 million new cars in March

- First quarter total up by 8%, to 2.89 million units

- Italy posts an impressive 18% year-on-year increase in registrations

- Renault was the biggest improver among top 5 brands

- SUVs continued to gain popularity, with registrations up by 22% in March

- Fiat 500, Opel/Vauxhall Astra were the only models within top 10 to gain market share

The latest figures for Germany, UK, Italy, France and Spain show further positive results for March 2016. Thanks to the traditional registrations peak in the UK, the total for the Big 5 markets surpassed the one million units mark, rising to 1.36 million new cars, up by 5% over March 2015. First quarter registrations advanced 8% to 2.89 million cars, while the March SAAR came in at 11.04 million across the five markets. SUV registrations ranked first, accounting for more than one out of four passenger cars registered.

However, last month’s growth can be attributed to different factors across different regions. Italy saw the highest increase, with registrations recording a 18% jump compared to the same month last year. This was possible thanks mostly to higher company car and private purchases. Despite this big increase, Italy was only the fourth largest market of the Big 5, ahead of Spain. Volumes in the UK advanced 5% to a March record of 518,700 units, taking its year-to-date total to 771,800 cars. France was the other big market to register a monthly increase (+7%), with YTD growth at 8% over the first quarter of 2015. March registrations in Germany and Spain stalled at 0% and -1% respectively, though their YTD volumes were still positive at +4% in Germany and +8% in Spain.

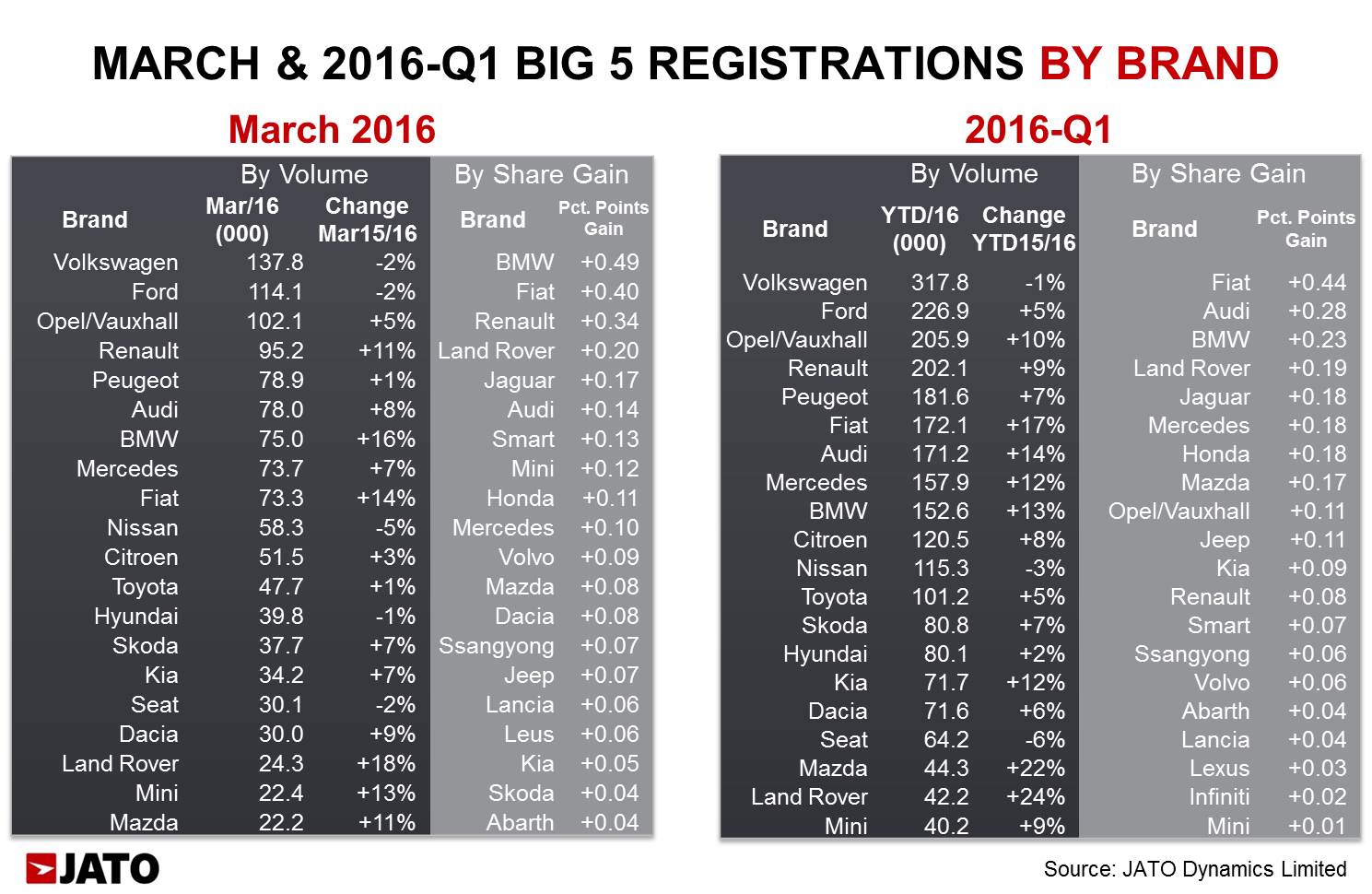

Volkswagen remained the best-selling brand with 137,800 new cars, though registrations dipped 2%, losing ground on its competitors by 0.77 percentage points. The German brand’s market share has now slipped for nine straight months, as the company continues to deal with the emissions issue. Volkswagen registrations dropped by 6% in Germany and 17% in Spain, and the brand lost market share in the UK and France. Only its subcompact and compact ranges posted positive numbers. But it was not the only big brand to lose ground, as second placed Ford also suffered from lower demand in Spain (-27%) and in the UK (-5%), taking its Big 5 total to 115,800 units, down by 2% from March 2015. Meanwhile, Opel/Vauxhall and Peugeot posted small gains, leaving Renault as the best improver among the top 5 best-selling brands. The French car maker was boosted by strong double-digit growth in Italy (+31%), France and the UK, as its SUV range continues to gain popularity (+65% in March).

The top 5 mainstream brands were followed by the three German premiums, which gained market share thanks mostly to their SUV registrations, and were collectively up by 37%. Sales of BMW’s ‘X’ family grew 43%, accounting for almost 24% of its total registrations in March. That was higher than the comparative shares for Audi’s Q-range (21.7%, up by 16%) and Mercedes’ SUV family (20.8%, up by 61%). Fiat occupied ninth place, with 5.4% market share and a 14% jump in March, thanks mostly to its popularity (+22%) in the Italian market. Italy accounted for 57% of Fiat’s volumes within Europe’s big 5. The top 10 was completed by Nissan, which experienced a 5% drop, reducing its market share from 4.8% in March 2015 to 4.3% as of last month.

The premium segment was boosted by strong sales increases coming from Land Rover, Volvo and Jaguar, as well as Infiniti, which more than doubled its volume over March 2015. Other key improvers included Ssangyong, Honda, Mini, Smart, Abarth and Lancia.

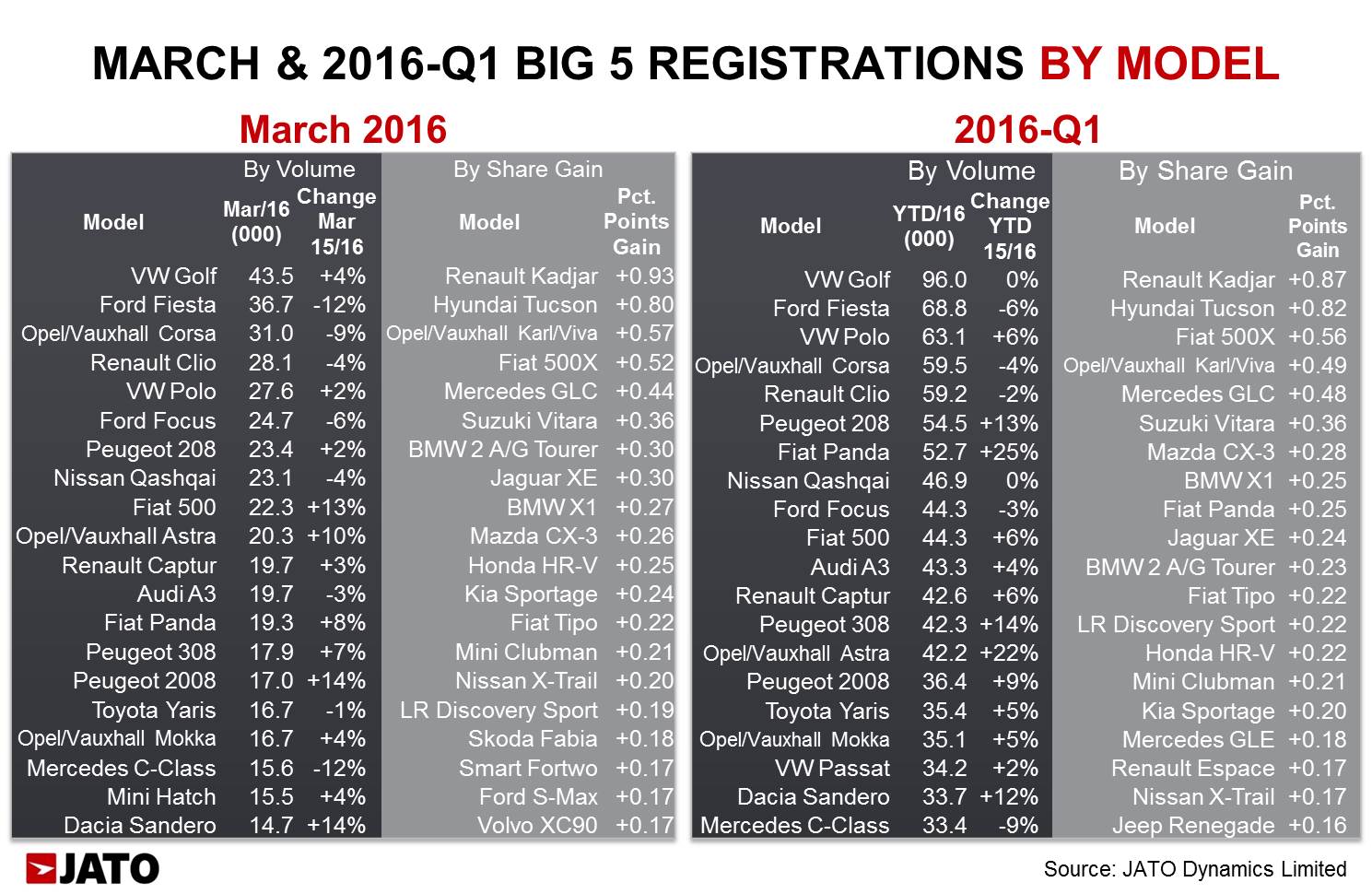

The SUV boom continued at an impressive pace, with the segment gaining even more market share, thanks to sales growth of 22% during March, and an overall 25% increase in Q1 of 2016. Last month its registrations in the big 5 European markets totalled 343,400 units, making up over 25% of the total. In contrast to this positive trend, sales of subcompacts fell 1% over March 2015 and grew by only 3% during the first quarter. Meanwhile registrations of compact vehicles were up 4% in the month, and 7% in the quarter. However, these two segments were not the biggest casualties of the SUV segments surge, as the MPV figures show that their volumes have dropped by 8% in March, and 3% since January 2016. The same occurred in the large sedan/SW segment, with registrations down by 7% in March and 5% in the first quarter.

The Volkswagen Golf topped the model ranking, with registrations rising 4% to 43,500 units, while its cumulative results since January remained stalled (+0%). Despite its low growth rate, Volkswagen’s model did better than others at the top of the table, as Ford recorded a 12% drop on its Fiesta registrations, similar to the Opel/Vauxhall Corsa (-9%) and Renault Clio (-4%). In fact, there were only two models among the top 10 to gain market share: the Fiat 500 and Opel/Vauxhall Astra. The small Fiat re-entered the top 10 with a 13% rise, due largely to strong increases in Italy, France and Spain, while the Astra recorded a 10% increase. Among the big market share winners were the Renault Kadjar, Hyundai Tucson, Opel/Vauxhall Karl/Viva, Fiat 500X and Mercedes GLC.

“With lower increases across the Big 5 markets, we have seen an overall slowdown in growth. However the situation continues to be positive, with an overall growth rate of 8% for Q1 in 2016. The shift from traditional segments to SUVs continues, as more carmakers invest in what has proved to be an impressively popular and high-growth segment” concluded Felipe Munoz, Global Automotive Analyst at JATO Dynamics.

Download file: Big 5 EU Markets March 2016 Release - Final.pdf