Latin American car market continues its upturn, with sales up by 7% in H1 2018

- Brazil, Argentina and Chile boost overall sales

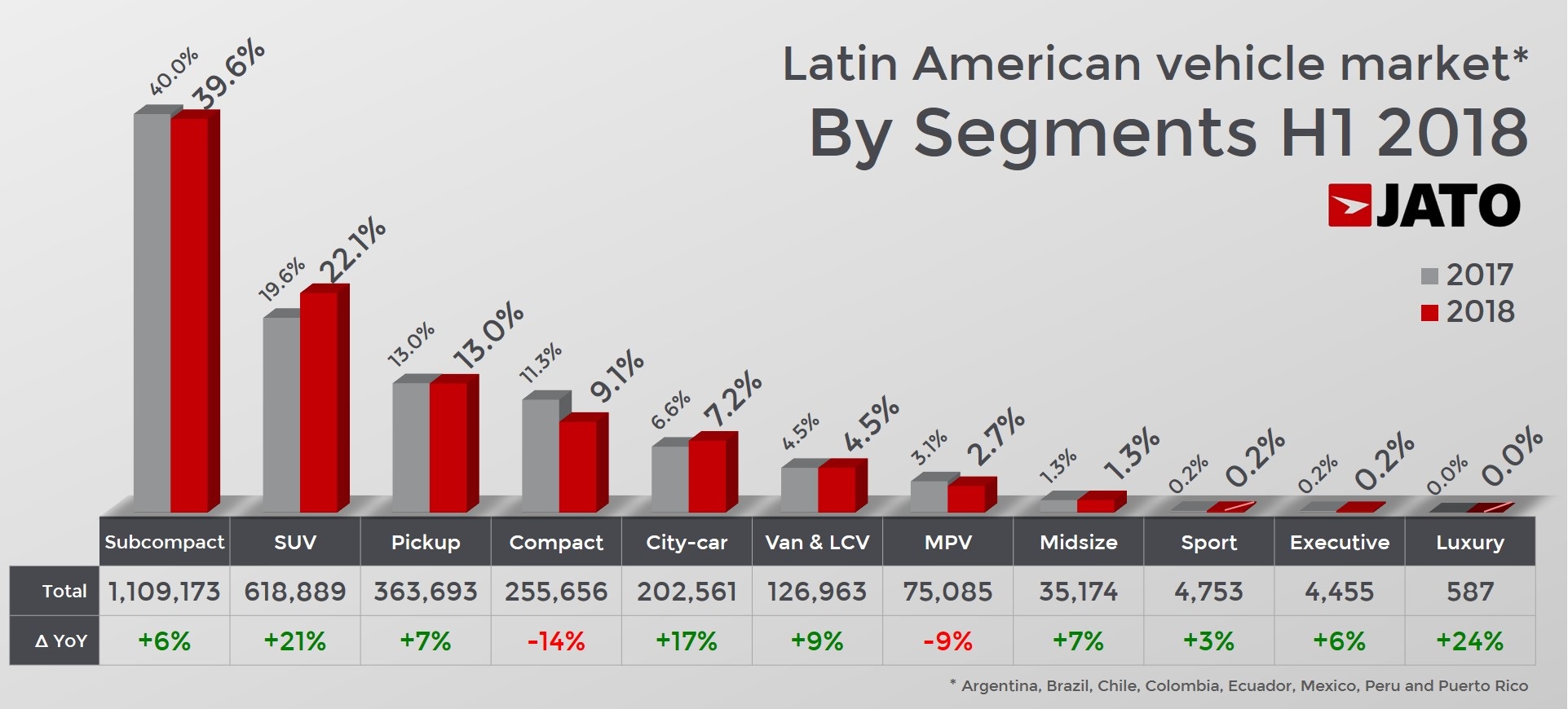

- Subcompacts continue to dominate with 40% market share, but SUV demand soars

- FCA, VW Group and Hyundai-Kia among the top winners

After posting a good first quarter, the Latin American car market continued the positive trend into the first six months of the year, with sales growing by 7% compared to H1 2017. The outlook continues to be positive for the region, with passenger car and light commercial vehicles sales totaling 2.83 million units. “The results are good, but the economies in the region must grow faster in order to have an even stronger and bigger market. Despite the upturn, Latin America continues to be a marginal market when compared to the world’s developed countries,” comments Felipe Munoz, global analyst at JATO Dynamics.

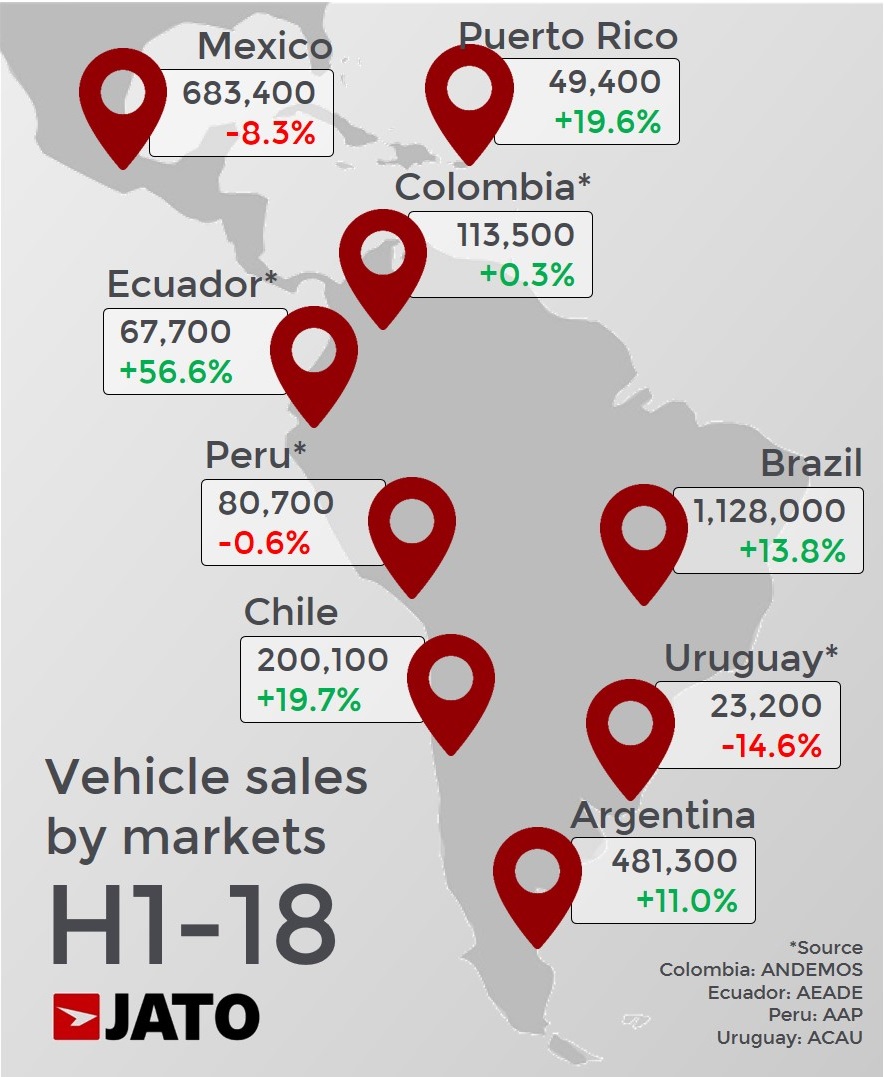

In fact, the figures for the first half of the year are still far from the record posted in 2013. While the markets in Argentina and Chile recorded their best ever first half in terms of car sales, Brazil is still a way off from the volume it recorded in H1 2013 with 1.71 million units. “Increased sales and local production mean a significant 1.43 million units were produced in H1 and we anticipate further expansion during the rest of the year. As the market becomes more vibrant with more manufacturers, models and choice available for the consumer we expect results to continue to be positive.” adds Vitor Klizas, president of JATO Dynamics Brazil.

In Mexico, the market posted a 8.3% decline compared to the record registered in H1 2017. Gerardo San Roman, president of JATO Dynamics Latin America comments, “More than just a fall in sales, there was a deceleration in the Mexican market in H1 2018. But we do still see positive signs in key segments such as SUVs, premiums and alternative fuel vehicles. Mexico will continue to be a solid market of around 1.4 million units.”

Despite posting an 11% increase, the market in Argentina still faces a challenging time ahead. In June, total sales fell by 17% in anticipation of difficult conditions in the coming months, as the currency continues to fluctuate and the effects of the Government’s austerity plans are felt.

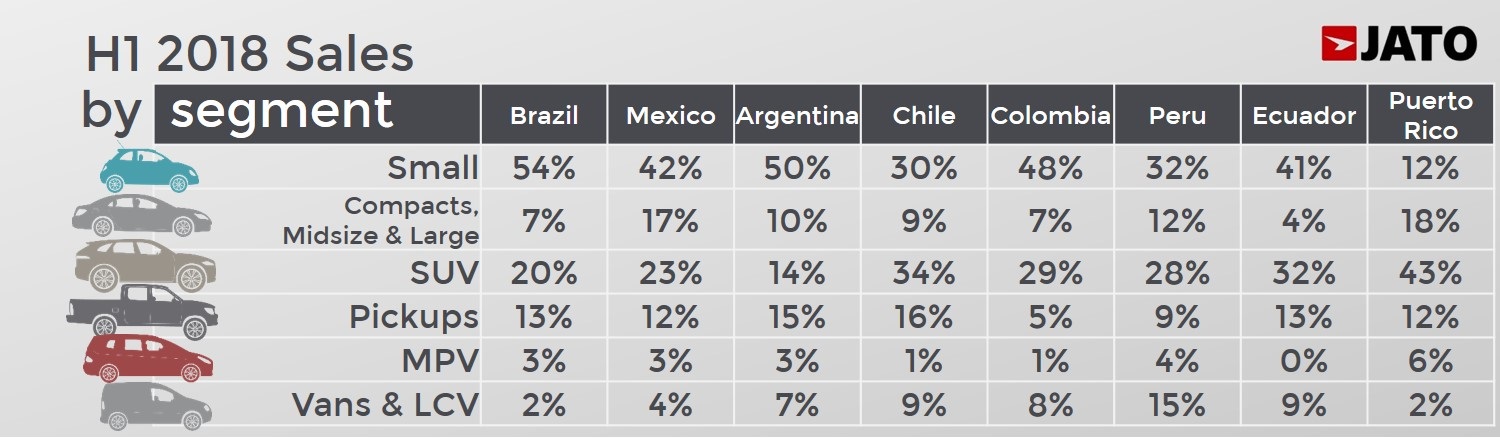

Sales in Chile were boosted by a favorable currency exchange and a wider array of models on the market for consumers to choose from. For the first time ever, the market reached the 200,000 units mark in the first half of the year. As is the case in the developed markets, Chile’s growth was boosted by the SUV boom, which accounted for 34% of total sales.

In Colombia, the fifth largest market in the region, the situation improved after posting a negative result in Q1 2018. According to Oliverio Garcia, president of Andemos, “The vehicle market is already stabilising so we can be hopeful of reaching the 250,000 units sales target, as long as the value of the dollar keeps falling”.

It is also important to note the strong performance in Ecuador, where consumers now have more options than ever. The array of models on offer continues to widen and prices continue to fall as a result of the free trade agreements signed with Colombia and the European Union. According to AEADE data, the drivers of growth were SUVs (+64%), subcompacts (+47%) and pickups (+39%), which combined made up 74% of total sales.

There was no change in consumers’ segment preferences. Subcompact cars continued to dominate with 1.11 million units sold, meaning they accounted for 40% of the total market. This segment was led by the Chevrolet Onix, which was the region’s top-seller. Other strong performers in the segment incldued the new Fiat Argo and Volkswagen Polo, which entered the top 10 of the B segment, outselling the Chevrolet Aveo/Sonic and Nissan March. This was the best-selling segment in Brazil, Mexico, Argentina and Colombia.

However, the real driver of growth was the SUV segment, which was also responsible for boosting the markets in Europe, China and the USA. Results from the first half shows that almost 619,000 SUVs were sold, up by 20.9% compared to the first half of last year. With 22% market share, there has never been so many SUVs in Latin America before. “The arrival of more affordable SUVs is tempting more consumers to take part in the boom”, comments Felipe Munoz. However, their market share still lags behind the numbers posted in Europe (34%), the USA (44%) and China (43%).

However, the real driver of growth was the SUV segment, which was also responsible for boosting the markets in Europe, China and the USA. Results from the first half shows that almost 619,000 SUVs were sold, up by 20.9% compared to the first half of last year. With 22% market share, there has never been so many SUVs in Latin America before. “The arrival of more affordable SUVs is tempting more consumers to take part in the boom”, comments Felipe Munoz. However, their market share still lags behind the numbers posted in Europe (34%), the USA (44%) and China (43%).

The SUV segment is led by Renault-Nissan with a 20% market share thanks to the Nissan Kicks (Latin America’s top-selling SUV), and the popular Renault Duster and Captur. Hyundai-Kia came second in the segment, due to the popularity of the Hyundai Creta and Kia Sportage, and FCA posted a big increase of 28%, outselling Honda thanks to the excellent results of the Jeep Compass, the best-selling compact SUV in the region, and the Renegade.

Pickups were also an important and popular segment in Latin America. Despite losing ground in terms of market share, they continued to be the third best-selling segment. Through June, their sales totalled 363,700 units, of which 58% were midsize pickups, led by the Toyota Hilux. However, the biggest driver of growth was the small pickup subsegment, as sales jumped from 71,600 to 81,800 units, led by the Fiat Strada.

Renault-Nissan continued to dominate the Latin American car market with a market share of 17.6%, thanks to the strong presence of Renault in South America and Nissan in Mexico. It also has one of the largest SUV lineups in the market. It was followed by General Motors, whose Chevrolet Brand was the market leader in Brazil, Colombia and Ecuador. Volkswagen group came in third with 365,500 units, equating to a 7.2% increase than in the same period of 2017.

In contrast to its performance in Europe, FCA group was the top market share winner in Latin America during the first half of the year. The latest launches of the Fiat Argo, Cronos, Mobi, along with the brilliant results from Jeep, which became the region’s top-selling SUV Brand, explains the good results of the Italian-American automaker. The Korean Hyundai-Kia also showed a big improvement, taking their market share up to almost 10% during the first six months of the year.

Chinese manufacturers also deserve some recognition. Despite posting a marginal market share, they still posted a significant increase, jumping from from 1.9% in H1 2017 to 2.5% this year, a result that confirms Latin America is one of the top export markets for Chinese cars. Chinese manufacturers are especially popular in markets where the car industry is not a key part of the economy, such as Chile, Ecuador and Peru.

In terms of models, the Chevrolet Onix continued to shine by increasing its sales as a result of double-digit growth in Argentina, Colombia and Chile. The Ford Ka/Figo, Chevrolet Spark/Beat and Prisma also recorded big increases. The new Renault Kwid, Fiat Argo and Volkswagen Polo continued to climb the rankings and hit the top 25.

Outside the top 25 it is important to mention the +28% posted by the Jeep Renegade, the 19,700 units sold of the Volkswagen Virtus, and the 16,800 of its rival the Fiat Cronos. Sales of the Renault Captur were up by 67%, while sales of the new Hyundai Accent registered 55% growth. The Volkswagen Tiguan Allspace recorded 12,300 new sales, and demand for the new Suzuki Swift soared by 54%. Full ranking in our blog.

Many thanks to Oliverio Garcia from ANDEMOS Colombia, Alfredo de las Casas from AAP and Oscar Calahorrano from AEADE.

Version en español: H1 2018 Latinoamerica Comunicado de prensa – Final

Versão em português: H1 2018 America Latina Comunicado de imprensa – Final

More Articles

- European demand for electrified vehicles continues in June

- JATO Dynamics Appoints Chief Data & Digital Officer

- Knock-on effects of WLTP sinks European car market during September and causes major shakeup in the industry rankings

- JATO reveals industry impact as correlated NEDC values are shown to be higher than NEDC tested

- Renault Clio becomes the best-selling car in Europe, outselling the Volkswagen Golf in May