Brexit uncertainty caused UK registrations to decline in H1 2017, as Europe’s other large markets continued to grow

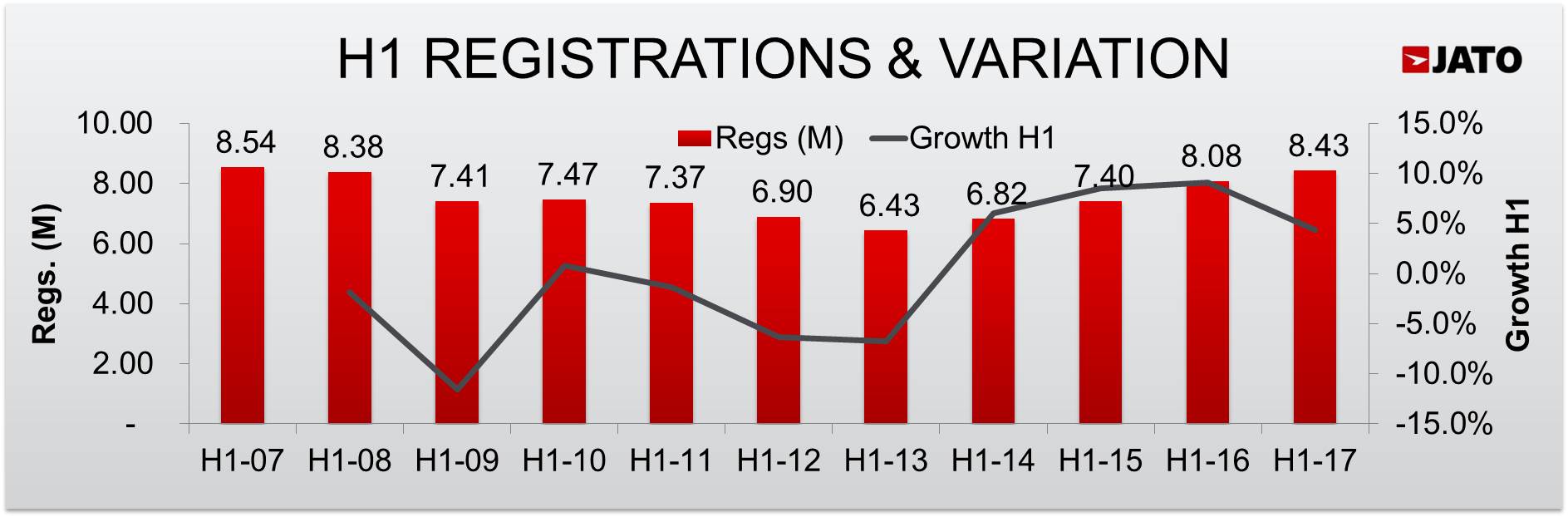

- European car registrations experienced the highest H1 total since 2007, with a total of 8.4 million registrations, meaning Europe was a region helping to drive growth in terms of automotive sales

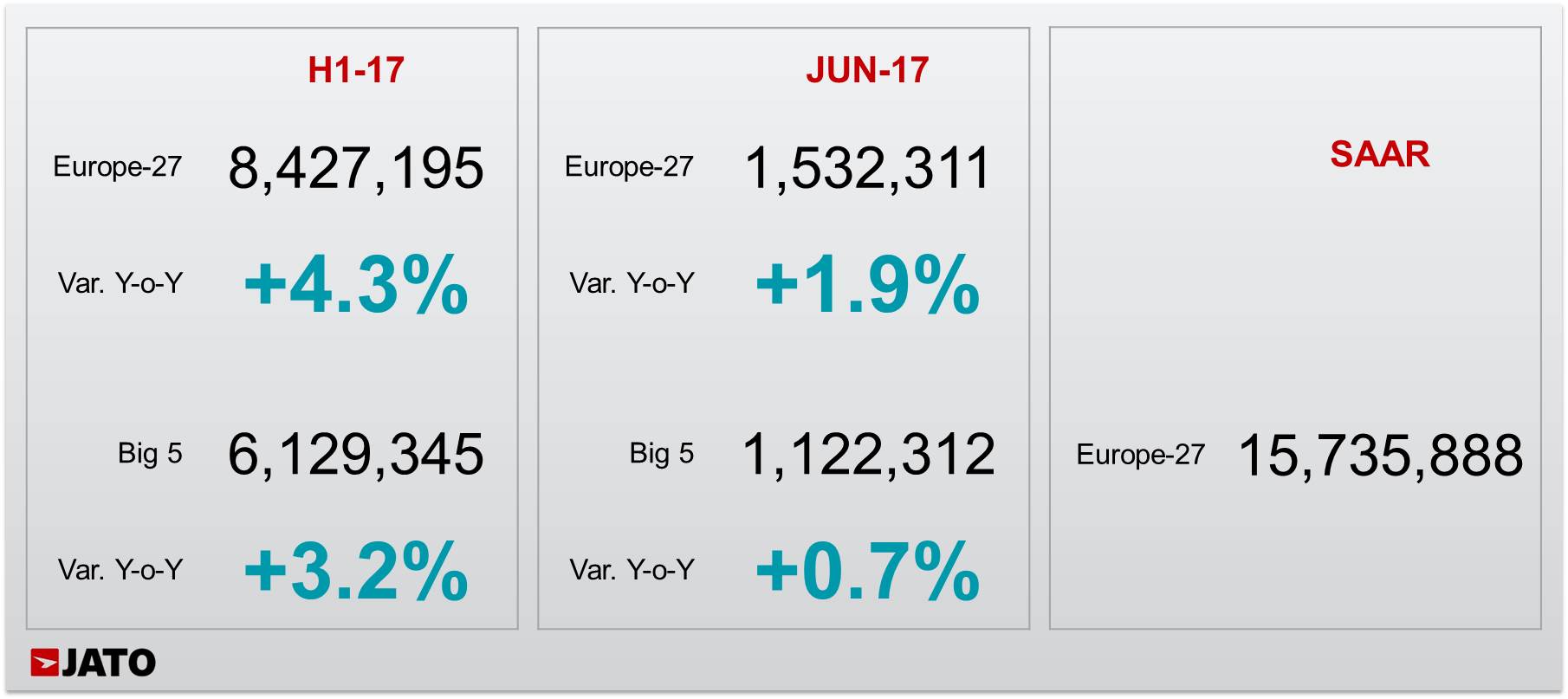

- Registrations totalled 1.5 million units in June 2017, an increase of 1.9% when compared to the same month last year, and the highest June total for a decade

- The Volkswagen Golf, Europe’s most popular car model, saw its volume drop by 11.6% for H1 2017

The European car industry continued to grow in June 2017, with new registrations for the month totalling 1.5 million – an increase of 1.9% when compared to the same month last year. In terms of volume this represents the highest total for June in the last decade, and is only 22,000 units behind the record total which occurred in June 2007. This performance concluded the strongest H1 since 2007, with a total of 8.4 million registrations for the half year, an increase of 4.3% on H1 2016. However, growth in the region is slowing following the exceptional performance of recent years; in comparison, 2016 saw growth of 9.1% on the previous year.

Four of Europe’s five largest markets – Germany, France, Italy and Spain – led this growth, with their collective H1 registrations up by 4.7% to 4.7 million units. This can largely be attributed to the healthy economic performance of Germany, and Italy’s increased stability and economic recovery. The European region is helping to drive growth in terms of automotive registrations, in comparison, the USA experienced a fall in car sales of 2.1% over the same period, whilst China saw registrations grow by a modest 2.6%.

Despite the strong performance across Europe, the UK was one of only five markets that posted a decline in registrations for H1 2017. The UK posted a fall in registrations of 1.3% compared to H1 2016. This decline comes after five consecutive periods of H1 growth for the UK – registrations jumped from 1.0 million units in H1 2011 to 1.4 in H1 2016. The negative performance demonstrates that Brexit has begun to impact the automotive market, with consumers delaying purchase amidst economic uncertainty.

“Overall, the market is looking healthy in Europe, with the strongest H1 performance since 2007. In particular, the Central and Eastern European markets have grown strongly this year and with some of them recording record levels of employment this trend looks set to continue. However, it’s notable that the UK is experiencing a slowdown in registrations which can be attributed to uncertainty about the nature of the country’s exit from the EU. Until there is clarity over how Brexit will work and what the UK’s relationship with the EU will look like, the UK market may continue to decline, whilst the rest of Europe continues to grow.” commented Felipe Munoz, Global Automotive Analyst at JATO Dynamics.

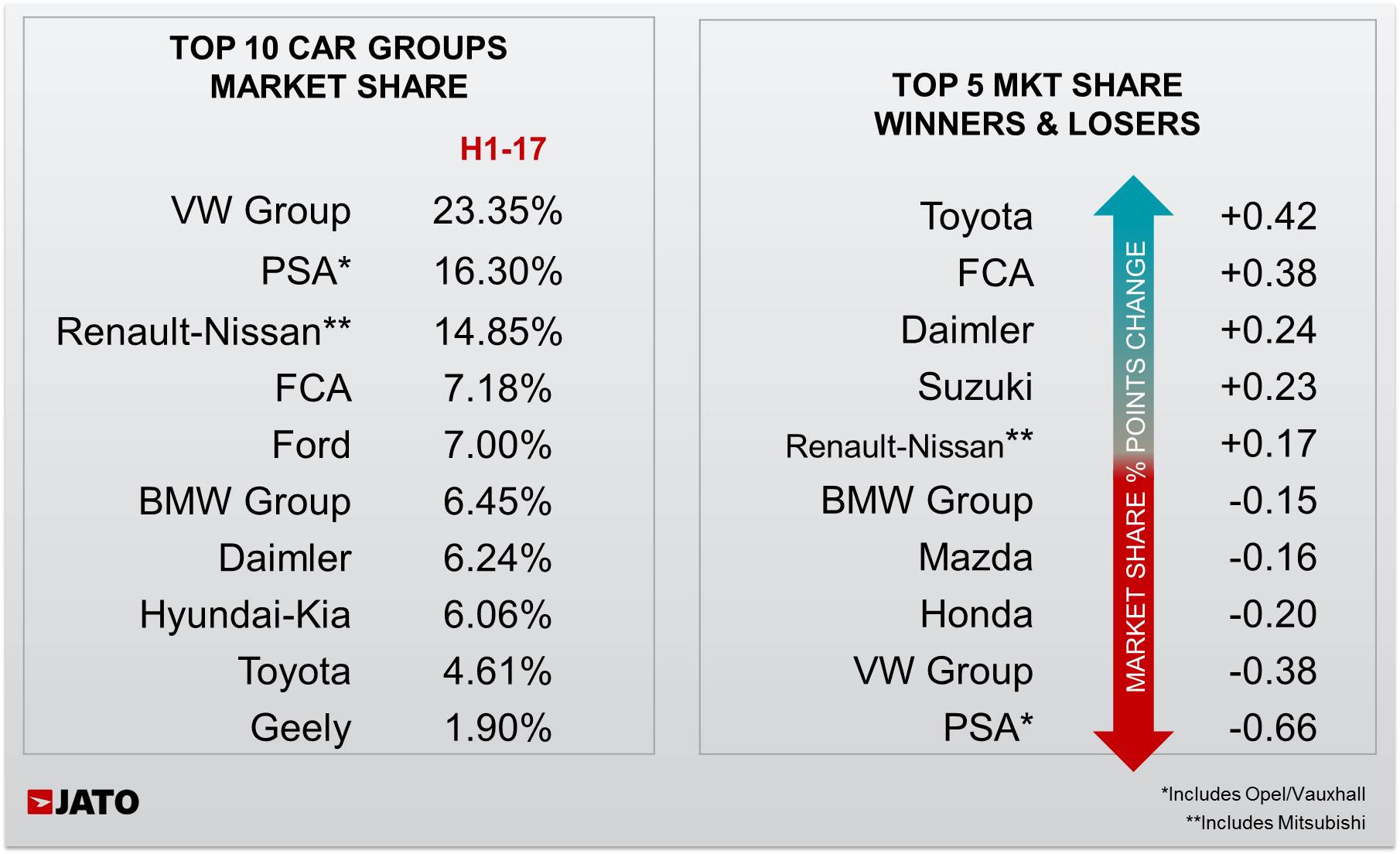

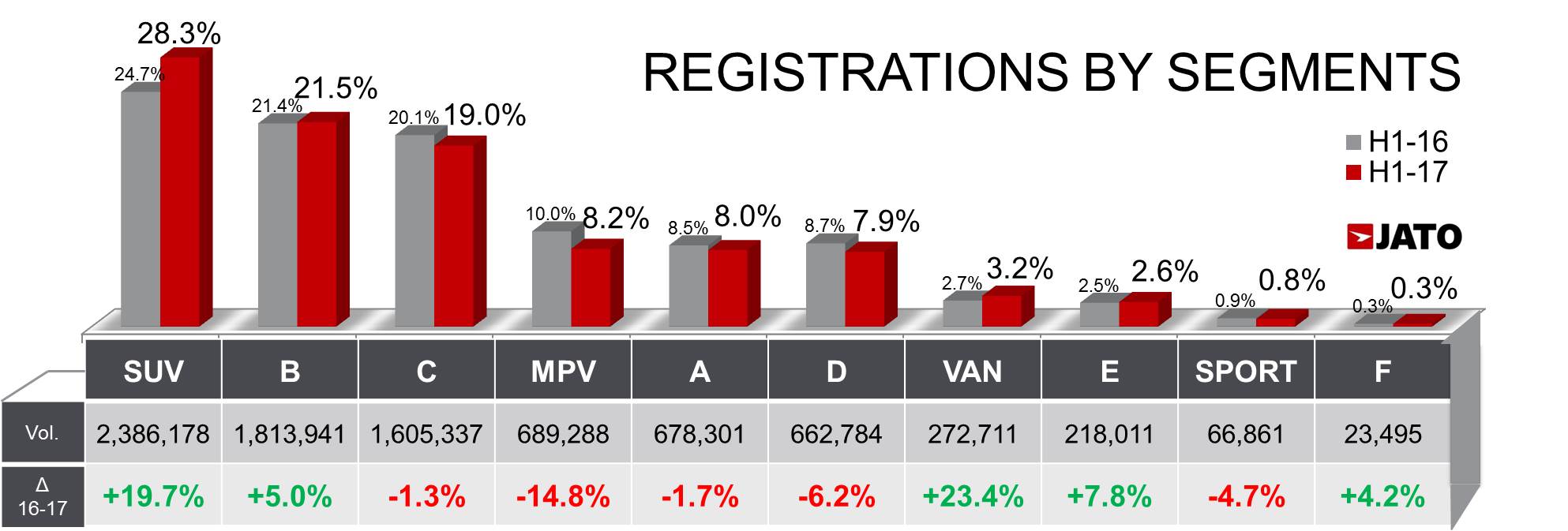

VW Group’s market share decreased – it fell from 23.7% in H1 2016 to 23.3% in H1 2017. This was the second highest fall in market share, only PSA experienced a larger decline with its market share declining by 0.6 percentage points of share. The market continued to be driven by SUVs such as the VW Tiguan and Peugeot 3008. In the compact segment, the VW Golf leads, but its volume for H1 2017 fell by 11.6%, whilst the Renault Megane experienced growth of 32.7%.

Download file: h1-2017-europe-reg-release-final.pdf