AFVs recorded second highest market share ever following 9.9% decline in diesel registrations in Europe during October 2017

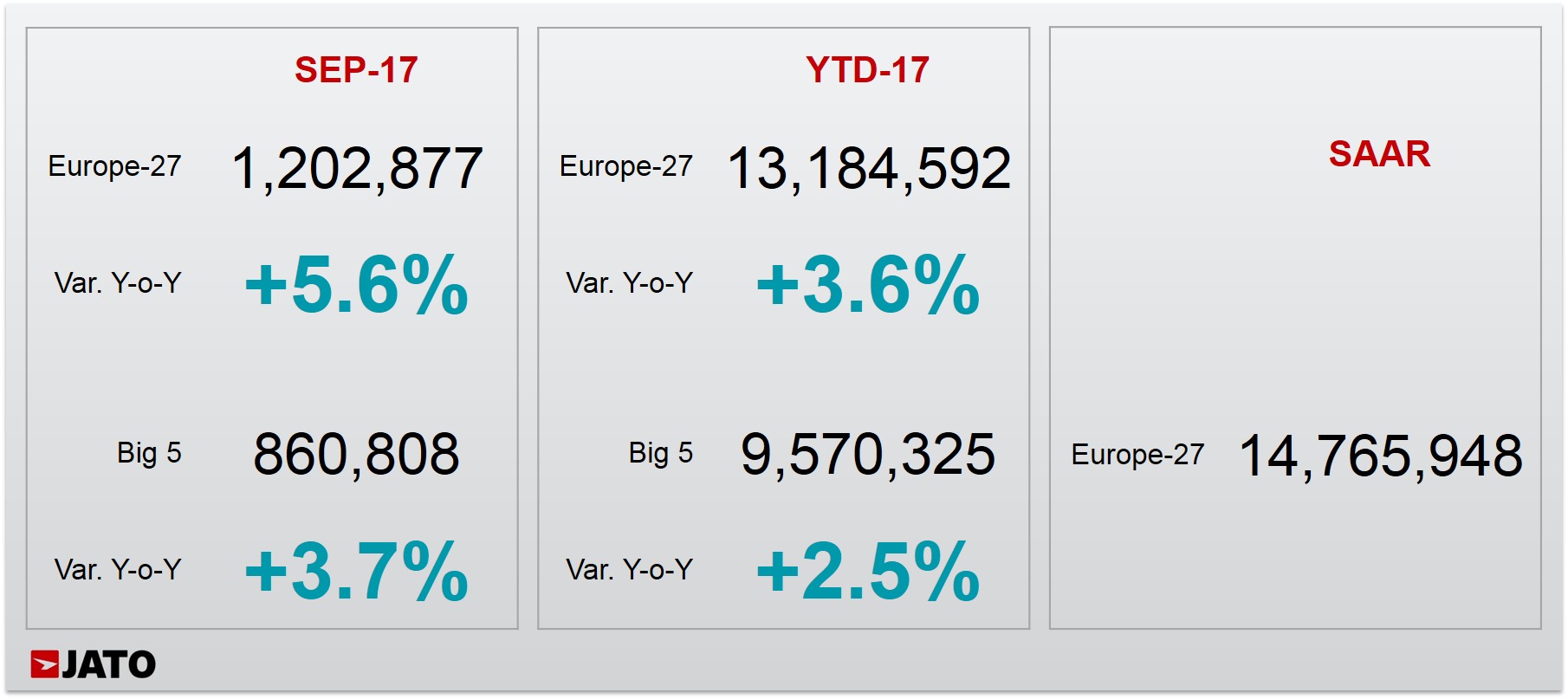

- European car registrations increased by 5.6%, with a total of 1,202,877 registrations in October 2017

- AFVs (alternative fuel vehicles) recorded a 5.5% share of the market, the fuel type’s second highest market share ever

- The VW Golf maintained its top spot, with a significant 24% increase in registrations

The European car industry showed its resilience in October 2017, with new registrations totalling 1,202,877, an increase of 5.6% when compared to October 2016. This is the highest volume recorded for October since 2009, when 1.26 million units were registered. Despite a turbulent 2017, results for the first ten months of the year show an overall increase in registrations of 3.6%, with 13.18 million units registered over the period. This is the highest volume recorded since 2007, when 13.62 million vehicles were registered during the same ten month timeframe.

Growth was driven by increased demand for gasoline, electric and hybrid vehicles, and the stellar performance of SUVs. Strong results in major European markets including France, Italy, Spain, Poland and the Netherlands all contributed to October’s positive performance. The performance of these markets offset the decline in demand for diesel vehicles, and the decline in the UK market where registrations were down by 12.2% compared to October 2016.

There was significant variation in the performance of fuel types in October. 619,300 gasoline vehicles were registered during the month, meaning the fuel type accounted for 51.5% of the market, an increase in market share of 5.1 percentage points. In contrast, demand for diesel vehicles declined, with 498,500 units registered, a decline in volume of 9.9%. As a result, the fuel type accounted for 41.4% of the total market, the lowest market share for October in the last ten years. In contrast, AFVs reported the second highest market share ever recorded in October 2017, with 66,000 electric and hybrid vehicles registered. As a result, the category accounted for 5.5% of total registrations. In contrast, ten years ago in October 2007, AFVs accounted for only 0.3% of the market.

“Demand for diesel vehicles has declined following a series of initiatives to reduce diesel use, and subsequent confusion around proposed bans. This shift has boosted gasoline and AFV registrations. Growth of electric and hybrid vehicles has accelerated during the last four months and consumers are more aware of the choices available. But, despite a series of launches, there’s still limited AFV choice in categories such as the SUV segment. When looking at the AFV data,[1] hybrids still lead the way, accounting for 59% of the total volume for the AFV category, compared to PHEV and fully electric (BEV) vehicles, which accounted for 23% and 17% respectively,” commented Felipe Munoz, Global Automotive Analyst at JATO Dynamics.

The performances of mainstream brands contributed to the positive October performance. In contrast, premium brands recorded a 1% decline, and accounted for 23.5% of total registrations, as the growth of the three German premium brands slowed.

The VW Golf held on to its number one position, following an increase in registrations of 24%, compared to the same month last year. As a result, the Golf was the best-selling vehicle in nine markets. Meanwhile, the Peugeot 208 occupied a historic third position.

[1] AFV data is available for: Austria, Belgium, Croatia, Czech Rep., Denmark, France, Germany, Ireland, Italy, Norway, Netherlands, Slovenia, Spain, Sweden, Switzerland and UK.

More Articles

- Car Registrations decreased by 0.5% across Europe’s Big 5 Markets in October

- Global Car sales up by 5.6% in 2016 due to soaring demand in China, India and Europe

- European car registrations up by 9.0% to 1.34 million, while growth returns to uk market

- European car market remains stable for the second month in a row in May, due to strong demand for small and compact SUVs

- Global car market remains stable during 2018, as continuous demand for SUVs offsets decline in sales of Compact cars and MPVs