A market brand analysis of the C-SUV HEV segment to track who’s maximising Monthly Payments data for better performing finance strategies

With 80 – 90% of new vehicles sold through some form of automotive finance, OEM finance managers need to track and analyse the monthly instalment to ensure they compete effectively in their segments and markets. To illustrate how that works in practice, this analysis focuses on the Nissan Qashqai as the benchmark vehicle, set against its closest C-SUV HEV competitors in Great Britain to demonstrate how four manufacturers can pursue four very different finance strategies to win the same buyer.

Four brands, four strategies

Filtering the C-SUV HEV basket to 36 – 37 months, 10,000 miles per year and zero deposit and four very different competitive strategies come into focus. None of them are accidental.

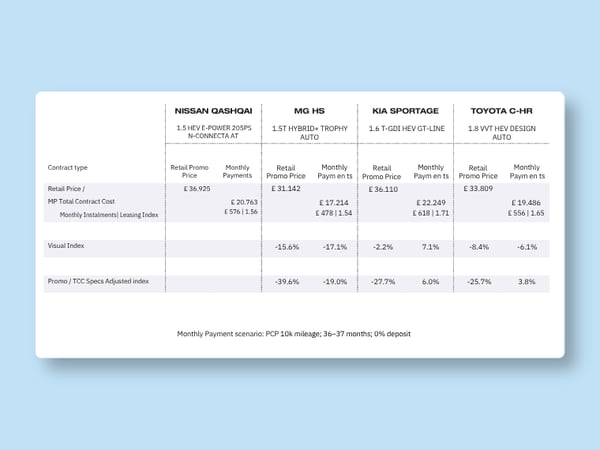

Nissan Qashqai — £616/month

The Qashqai serves as a useful illustration of a balanced, controlled approach. Sitting in the middle of the segment on APR at approximately 2.5%, it carries a residual value of around 42% which is below most of its peers. Rather than engineering affordability through a high RV or heavy discounting, this approach uses a balanced mix of both levers. A recent Q2 programme rebalance deliberately reduced both APR and RV simultaneously, holding the monthly payment steady within the core segment band of £600 – £650 while reducing residual value risk exposure. It is a strategy built on stability and control rather than aggressive market positioning. Nissan is not chasing short-term volume through a headline rate. It is actively managing the long-term cost and risk profile of its finance programme.

MG HS — £558 → £470/month

The MG HS illustrates the opposite end of the strategic spectrum. Between February and April 2026, MG executed a coordinated pricing reset. It dropped APR from 6.9% to approximately 2.9% while discounting increased from around zero to approximately £2,000. The combined effect was a significant step-change in monthly payments, repositioning the model firmly in value-leader territory. With an RV broadly in line with the segment at around 45%, the strategy relies on front-end support of lower APR and higher discount rather than residual value to drive volume.

Toyota C-HR — £586/month

The C-HR demonstrates a different approach. Carrying the highest sustained discounting in the basket at approximately £4,000, combined with a higher APR of around 4.9% and a declining RV, the logic is to protect finance margin by keeping the rate high while using price reduction and residual engineering to remain competitive on the monthly payment. It is a margin-first strategy that uses the discount tool to compensate for the cost of higher finance rates.

Kia Sportage — £666/month

At the top of the basket, the Sportage operates with an APR of approximately 5.9% and a strong RV of around 48%, making minimal use of discounting or finance rate subsidy. This reflects confidence in the vehicle’s residual value strength and the brand’s ability to command a premium positioning within the segment, while protecting margin.

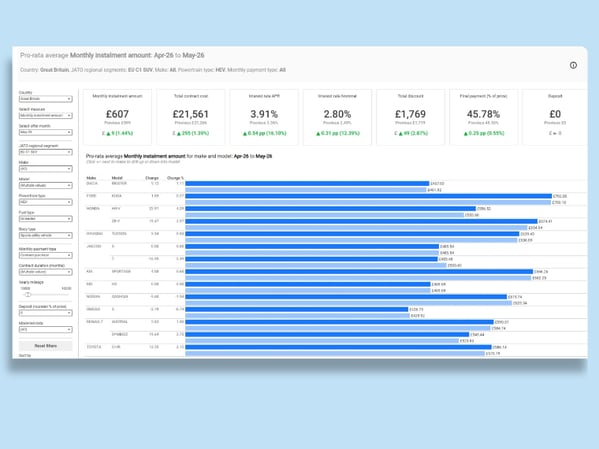

Reading the market via monthly instalment amount

Average monthly payment across the basket sits at £607, up 1.4% month on month, with most competitors clustered within a narrow £600 – £670 band. The Dacia Bigster anchors the lower end of the range, with the Kia Sportage and Ford Kuga positioned at the upper end.

Headline affordability appears stable at a , but underlying cost pressures are increasing. APR is up 0.54 percentage points month on month, total contract cost is up 1.4%, and discounts are slightly increasing. These are signals that the segment is becoming incrementally more expensive to compete in, and that context is directly relevant to any programme decisions being made in this period.

For Nissan, the Qashqai sits within the central cluster of that £600 – £670 band, a position that reflects deliberate programme management rather than competitive drift. With cost pressures building across the segment, understanding precisely which levers competitors are using to hold or improve their monthly instalment position becomes the critical next step.

The hidden differentiator

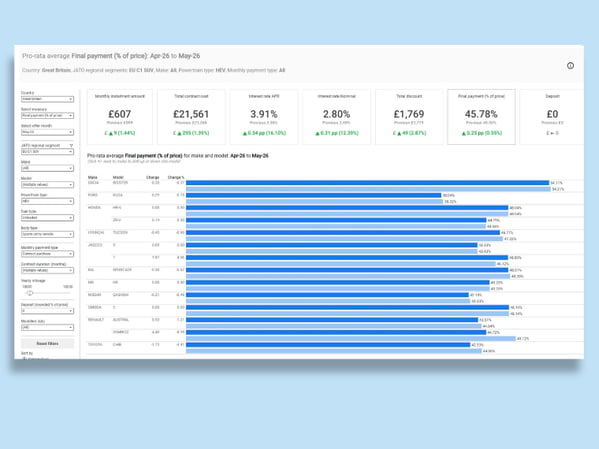

This monthly payments analysis shows the wide variation in RV strategies across the segment example. The Dacia Bigster sits at approximately 54%, a strong statement of confidence in future used values. The Ford Kuga sits at the opposite extreme at around 38%, accepting a less competitive monthly payment in exchange for reduced residual value exposure. The Qashqai sits at around 42%, towards the lower end of the 42–48% range occupied by most competitors. The Q2 programme data shows Nissan actively choosing to reduce RV further as part of the APR rebalance, a deliberate risk management decision that is only visible when both levers are tracked in combination over time.

APR as a volume driver or margin protector?

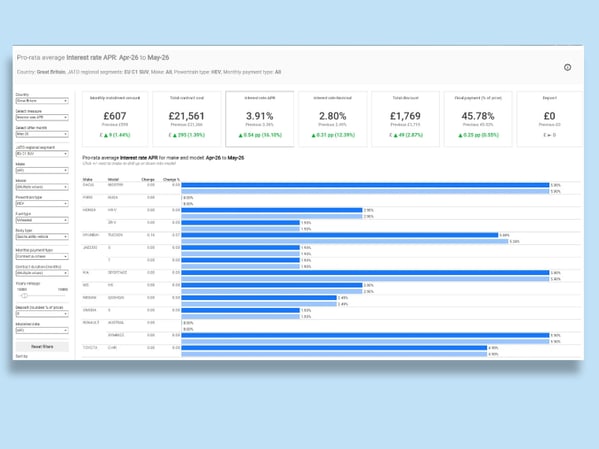

A low APR rate subsidises the monthly payment without touching the vehicle price or residual value, but it comes at a cost to the finance house.

The spread across this single segment basket is interesting. The Ford Kuga offers 0.0% APR, a clear volume-driving strategy that sacrifices finance margin entirely. Jaecoo and Omoda sit at approximately 1.9%. However, mid-range positions around 2.5% to 2.9% are occupied by several models including the Qashqai, MG HS and Honda HR-V, where APR is used as one lever among several rather than the primary competitive tool. At the higher end, Hyundai Tucson operates at approximately 5.1% and the Dacia Bigster at approximately 5.9%, positions that protect margin but require other levers, such as high RV or heavy discounting, to remain competitive on the monthly instalment. For Nissan, the post-rebalance position of 2.49% alongside a reduced RV represents a considered balance between affordability and risk management.

Evolving strategies in basket trend analysis

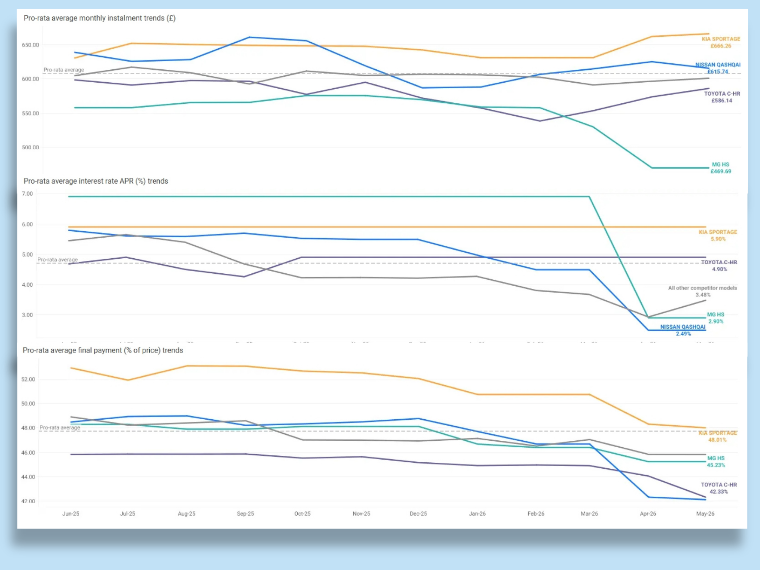

Tracking the monthly instalment, residual value and APR across the basket over the past 12 months reveals two distinct strategic narratives.

The Qashqai’s Q2 programme data shows APR reduced significantly while RV was simultaneously lowered, yet the monthly payment remained stable. Nissan restructured the underlying finance architecture without moving the consumer-facing number. The risk profile of the programme changed. The headline monthly payment did not. That kind of move is not visible in a price comparison and does not appear in end-of-month reporting. It only becomes identifiable when all three levers are tracked together over time.

MG’s strategy is equally deliberate but more aggressive. Between February and April 2026, APR dropped from 6.9% to approximately 2.9% in a coordinated move accompanied by a step-change increase in discounting. The outcome was a sharp reduction in monthly payments, from £558 to approximately £470, representing a clear and measurable repositioning into value-leader territory.

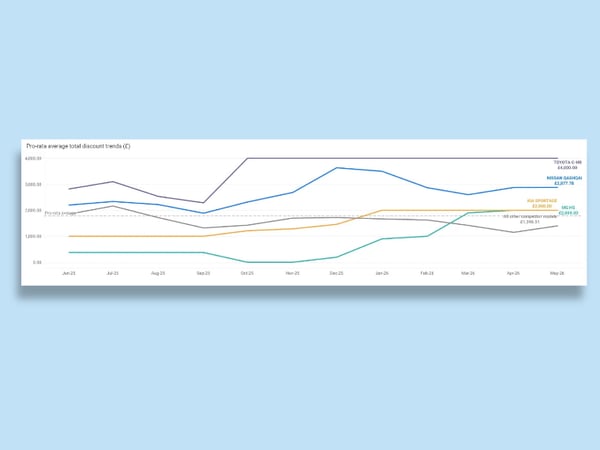

Selective and strategic discounting

By tracking total discount levels across the basket over 12 months, we can see how they are used selectively and in combination with other levers.

The Toyota C-HR has maintained the highest sustained discounting in the basket at approximately £4,000. But that discount is deployed alongside a higher APR and declining RV, functioning as the primary tool for staying competitive on the monthly instalment without subsidising the finance rate.

In comparison, MG HS discounting rose from near zero to approximately £2,000 between December 2025 and March 2026, deployed in tandem with the APR reduction to drive the dramatic fall in monthly instalment visible in our trend analysis.

The strategy is in the (version-level) detail

%20detail-2.png?width=600&height=450&name=The%20strategy%20is%20in%20the%20(version-level)%20detail-2.png)

At version level, the Qashqai’s stable, controlled positioning is confirmed, holding mid-pack with no significant swings in either direction. MG’s aggressive repositioning becomes even more pronounced when stripped of model-level noise, with the scale of its February to April reset clearly visible. The Sportage and Kuga hold their upper-band positions consistently, while the C-HR demonstrates competitiveness through sustained discounting rather than finance rate support.

What version-level granularity confirms is that none of this is accidental. Each brand is making deliberate, coordinated decisions about how to construct its monthly payment, and MPA makes those decisions visible. For Nissan, the version-level view validates that its Q2 programme shift was a precisely engineered move, adjusting APR and RV in combination to maintain consumer-facing affordability while managing the underlying cost and risk profile of its finance programme.

Ownership versus usage

When specifications are normalised, the competitive landscape shifts considerably. A model that appears to offer strong value on headline monthly payment may be including significantly more standard equipment than its competitors, and JATO’s specs-adjusted index makes that visible. This level of analysis is essential for OEMs wanting to understand the true value of a specification using real life data.

Non-captive finance analysis

.png?width=599&height=449&name=Non-captive%20finance%20analysis%20(2).png) The provider dispersion charts add a further layer of insight, giving finance managers a complete overview of the market and offering validation that their strategy is working and driving volumes across both captive and non-captive markets.

The provider dispersion charts add a further layer of insight, giving finance managers a complete overview of the market and offering validation that their strategy is working and driving volumes across both captive and non-captive markets.

The non-captive data reveals the Qashqai and Sportage sit relatively close to each other, highlighting how the Qashqai’s competitiveness holds up under different finance structures. The MG HS, however, tells a contrasting story. At £427 in the non-captive set, it is the highest monthly instalment in the core basket and a sharp contrast to its captive position.

What this means in practice

Monthly payments analysis ensures finance managers have a strategic view of where the market is but the intelligence to understand why it has moved, whether a competitor’s action represents a tactical campaign or a structural shift, and what a proportionate, profitable response looks like. It is not a decision that happens by instinct. It is the product of having the right data, at the right granularity, at the right time.

JATO’s Monthly Payments solution tracks and analyses the entire market in real time, enabling finance managers to define and adapt their pricing strategies in line with market dynamics as it happens.