From the marketing desk

April is over, which means we’re over a quarter of the way through 2026. Time really flies when you’re creating revolutionary new products and services and supplying class-leading data to customers around the globe.

This month our anticipated European passenger car volumes press release was released. Compared to January where there was a decline in sales, February's figures showed that the market grew slightly, primarily driven by battery electric vehicle sales. Find out more

Our Advisory team also shared fresh insights, including a standout article by Ashwin Amberkar on how India’s GST 2.0 reform is reshaping the automotive sector. More on that later but also be sure to check out the ‘News and insights’ section on the JATO site.

We also used the month to gear up for must attend global events. More on that later. Enjoy the read and the insights shared.

Yours in motoring,

Mark Talmage-Rostron

Content Lead

OEM news

In April, the JATO Advisory team produced two automotive reports. The first is full of valuable insights into JAECOOs success story in the UK SUV segment, and the second a comprehensive analysis of the Japanese automotive market in 2025.

In the JAECOO 7’s report, we examine how the models’ finance strategy has allowed it to gain ground on established models not by undercutting on price, but rather using a calculated finance strategy built around stable monthly payments and a low APR. Download the report today and get in touch if you'd like to trial our Monthly Payments solution for yourself (available for OEMs only). Get the insight

In this second report, we look at how Japan’s automotive market is navigating a pivotal transition with constrained domestic growth, accelerating electrification, and mounting competitive pressure from Chinese brands. Discover more

Further reports are already in development. The next two will focus on the US market and EU5 respectively and will be released in the coming weeks. Follow us on LinkedIn to be the first to know when they go live.

Advisory news

As a growing and ever-changing automotive market, India drew a lot of focus, as GST is reforming the transformative impact on strategic implications for 2026. Obviously in the article there are many points to unpack but, in a nutshell, India’s GST 2.0 is creating a stable pricing environment by reducing volatility and improving affordability, thus setting a stronger foundation for long‑term sector growth.

Read more about how the tax reform shift is triggering a sharp rebound in retail momentum.

Retail news

The main thing to come out of the Retail camp in April is that the team are gearing up for the Autosbuzz event taking place from 19-20 May in Sitges, Spain. We’ll be on Stand 3 so make sure you stop by for a chat.

Returning as a Platinum Sponsor this year, we’re looking forward to connecting with leading automotive e‑commerce businesses and marketplaces and bringing our products to the forefront of the ever‑evolving retail landscape.

If you’re attending on the 19th, don’t miss the engaging session “From Lead to Lifetime Value: Fixing the Marketplace–Dealer Disconnect.” The discussion will be chaired by our own Paul Hilton, Head of Retail, alongside Tim Smith, Chief Strategic Officer at Keyloop, as they explore how stronger alignment can unlock long‑term value across the marketplace ecosystem.

Leasing and fleet news

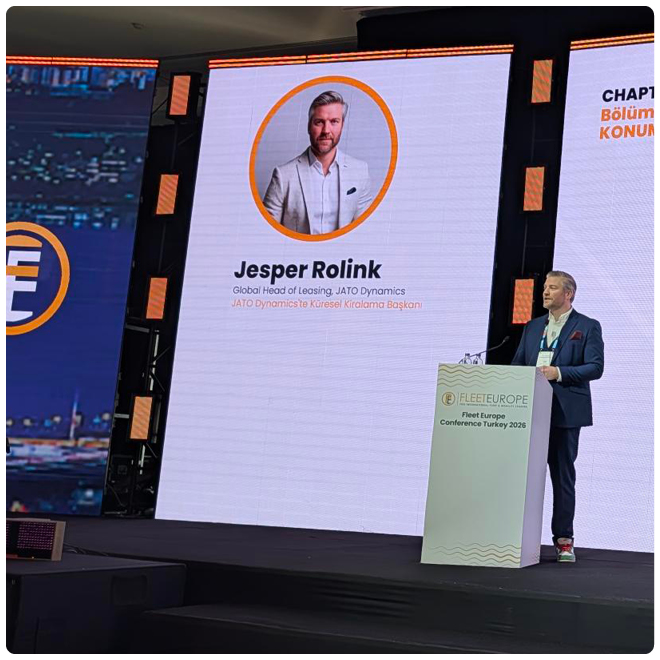

JATO was pleased to take part in Fleet Europe Istanbul, where industry leaders gathered to discuss the evolving dynamics of the Turkish automotive and leasing market.

Our Global Head of Sales, Jesper Rolink, delivered a data-led presentation exploring the growing presence of Chinese automotive brands in Turkey. Drawing on JATO’s datasets, the session highlighted the pace of market entry and expansion, how pricing and positioning strategies differ from established players, and the early signals of the impact on fleet purchasing decisions

Beyond the headline numbers, the presentation focused on the insights behind the data — helping local stakeholders understand not just what is happening, but what it could mean next for the Turkish market.

Professional Services news

JATO recently participated in the Neudata Summit in London, engaging with data buyers, analysts, and investors. Visitors had the opportunity to access our newly launched Financial Navigator Tool, which focusses on highlighting patterns and shifts behind the data, helping investors interpret what these trends may mean for future performance.

They also grabbed a copy of our Teaser Intelligence Series, a set of short, data-led insights designed to surface signals from the automotive market. Throughout the event, we had valuable conversations with executives from across the financial ecosystem.

These conversations highlighted rising demand for contextualised, forward-looking insights and clearer interpretation of market signals. For JATO, the summit was an opportunity to showcase our capabilities while gaining deeper insight into how automotive data is shaping investment decisions in a complex market.

Overview of local markets

As an established global company operating across 51+ countries, it stands to reason that there will be a lot happening in all the geographies that we have a presence in. That ongoing activity has brought about the aggregation of a lot of meaningful and actionable data that will be beneficial for you and your business. We’ve been busy putting together an overview of the regions we operate across, so read on to see what has been happening across Europe, Asia Pacific, and The Americas this month.

Europe

European automotive markets gained renewed momentum in April 2026, driven primarily by rising electrification amid elevated fuel prices and continued geopolitical volatility. According to ACEA, new EU car registrations rose 4.0% in Q1 2026, with March acting as a decisive catalyst following a weak January and mixed February performance.

The most pronounced shift remains powertrain-related. Battery‑electric vehicles (BEVs) accounted for 19.4% of EU registrations in Q1, up from 15.2% a year earlier, while hybrid‑electric vehicles retained leadership with 38.6% market share. Combined petrol‑diesel registrations fell to just over 30%, confirming the accelerating structural decline of combustion engines. Reuters data shows BEV registrations across 15 major European markets jumped 29.4% YoY in Q1 and surged over 50% YoY in March alone, with particularly strong gains in Germany, France, Italy and Spain. Total new‑car registrations in the EU, UK, and EFTA rose 11.1% YoY in March to 1.58 million units, the strongest monthly growth in nearly two years. Electrified powertrains (BEV, PHEV, HEV) collectively represented close to 70% of registrations, while petrol and diesel volumes continued to contract by double digits.

Fuel economics remain a decisive demand driver. Reuters notes that the Iran conflict contributed to one of Europe’s sharpest petrol price increases in recent years, pushing cost‑sensitive consumers toward EVs and hybrids not just for environmental reasons, but increasingly for energy‑security considerations. E‑Mobility Europe estimates that Q1 EV adoption alone could reduce annual oil demand by 2 million barrels.

From an industrial standpoint, S&P Global Mobility flagged growing downside risks for European production outlooks. Elevated transport costs, higher commodity prices and supply‑chain disruptions linked to Middle‑East instability have prompted limited production revisions for late‑2026 and early‑2027. OEMs are increasingly cautious on capacity expansion, focusing instead on margin protection and technology recalibration.

Financially, pressure on margins persists. While premium OEMs benefit from strong electrified demand, tariffs and battery‑related costs continue to weigh on profitability, prompting selective strategy reassessments across EV portfolios.

On the regulatory front, Europe maintained its technology‑neutral stance, with policymakers and industry bodies continuing to emphasize the role of hybrids and plug-in hybrids alongside BEVs to meet CO2 targets, especially as the average manufacturer emissions level remains close to (but still above) official fleet benchmarks.

Overall, April confirmed Europe’s electrification trajectory is accelerating structurally, but remains vulnerable to geopolitical shocks, energy costs and margin pressure.

.jpg)

Asia Pacific

Asia‑Pacific automotive markets in April 2026 reflected a widening divergence between strong export performance and uneven domestic demand. According to Reuters, China’s light‑vehicle market remains under pressure following subsidy reductions and price competition, despite continued leadership in EV technology and global exports.

Early‑year demand softness persists. Industry data shows Chinese passenger‑vehicle sales declined notably at the start of 2026, with NEV retail demand also retreating amid reduced tax incentives. However, April reporting emphasised that exports are stabilising the broader market with EVs accounting for a growing share of outbound shipments, particularly toward Europe and emerging markets.

Technologically, Chinese OEMs continue to set global benchmarks. Reuters reported intensified government backing for "AI Plus" industrial policy, triggering a race among automakers to embed AI‑driven systems into vehicles. OEMs such as Xpeng and Xiaomi unveiled advanced AI platforms enabling mapping‑free autonomous navigation, conversational vehicle assistants, and software‑defined driving updates. Industry officials described the shift as a structural transformation blurring the line between automakers and technology companies.

In Japan and South Korea, automakers remain exposed to trade and logistics disruption. Higher energy prices linked to Middle Eastern instability are weighing on production economics, while shipping delays continue to impact export strategy. S&P Global Mobility assessments published in April reaffirm downward revisions to 2026 regional output forecasts due to supply‑chain and cost volatility.

Southeast Asia shows a more resilient trajectory. Thailand continued positioning itself as a regional EV manufacturing hub, supported by continued investment from Japanese OEMs and domestic electrification incentives. In India, intensified industry appeals for entry‑level EV incentives ahead of FY 2026‑27 budget planning, as affordability emerged as a key adoption bottleneck despite strong headline growth.

From a macro‑economic standpoint, the Asian Development Bank warned in its April 2026 Outlook that higher oil prices and geopolitical fragmentation could slow regional growth to 5.1% in 2026, raising operating costs for automakers and consumers alike. Inflation expectations were revised upward to 3.6% as energy costs feed through supply chains.

In summary, Asia‑Pacific markets remain innovation‑led and export‑oriented, nonetheless face increasing demand volatility and policy‑driven uncertainty domestically.

The Americas

North American automotive markets in April 2026 were shaped by tariff fallout, regulatory shifts and a deepening pivot away from full battery‑electric strategies. According to JD Power and GlobalData, U.S. Q1 light‑vehicle sales fell around 7% YoY, reflecting pull‑forward demand ahead of tariff implementation and rising affordability pressures.

Tariffs remain central. Following the U.S. Supreme Court’s February ruling invalidating aspects of prior tariff frameworks, automakers began booking refunds. Reuters and CNBC confirmed that General Motors recorded a roughly USD 500 million benefit, lifting its full‑year profit outlook despite higher raw‑material and logistics costs linked to the Iran conflict.

EV adoption continues to cool. With federal EV tax credits expired since late‑2025 and emissions rules relaxed, BEVs now account for roughly 6 - 7% of U.S. new‑vehicle sales, according to Morningstar and Cox Automotive analysis. Traditional hybrids, by contrast, exceeded 12% market share, reinforcing OEM decisions to rebalance product portfolios.

Industrial realignment is accelerating. PwC reports that over 55% of vehicles sold in the U.S. are now produced domestically, with on‑shoring driven by tariff uncertainty and supply‑chain risk mitigation. OEMs such as GM and Ford are adjusting production schedules to bolster high‑margin truck and hybrid output.

Regulatory signals remain accommodative. The eased enforcement and penalty exposure related to fuel‑economy targets has eased compliance pressure, allowing automakers greater flexibility in model planning, but analysts warn that long‑term electrification competitiveness could be delayed as a result.

Overall, April underscored that the Americas are transitioning toward a hybrid‑led, protectionist‑influenced market, marked by cautious EV investment, stronger domestic manufacturing, and persistent geopolitical cost risk.

Behind the

wheel Newsletter

Subscribe to our monthly newsletter to get the latest industry news sent straight to your inbox.

Every month, we bring you a round-up of industry updates, including:

- Automotive markets overview

- Retail news

- Leasing news

- Professional services news