Following June’s registrations results for Europe, JATO Dynamics shares H1 figures for 26 markets.

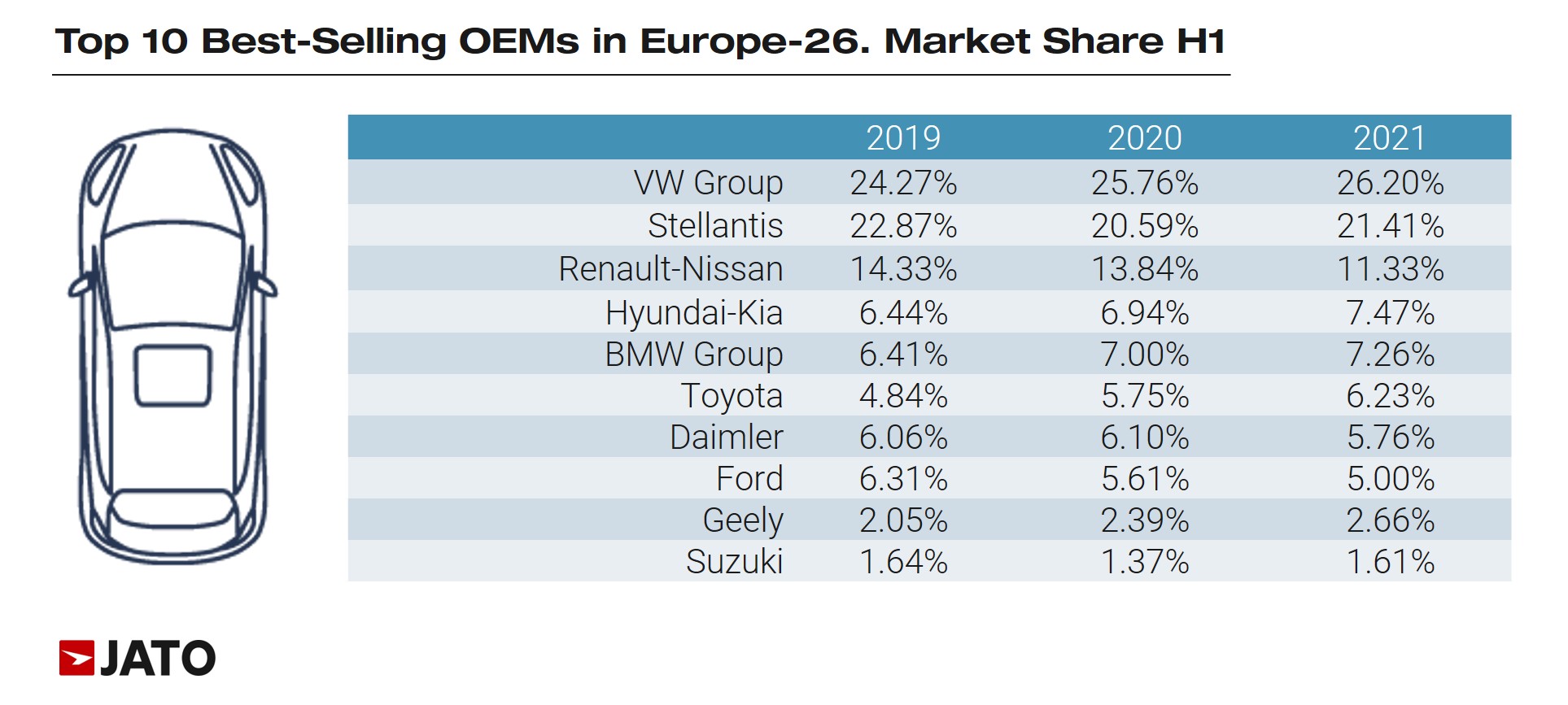

Unsurprisingly, in comparison to the same period in 2020 – when the impact of the pandemic and its various local lockdowns were in full force – the majority of OEMs operating in Europe posted positive volume upticks in H1 2021. However, the real differentiators can be seen when compared to H1 2019, in particular, with Volkswagen Group securing first place for market share this year.

H1 2021 vs H1 2019 results

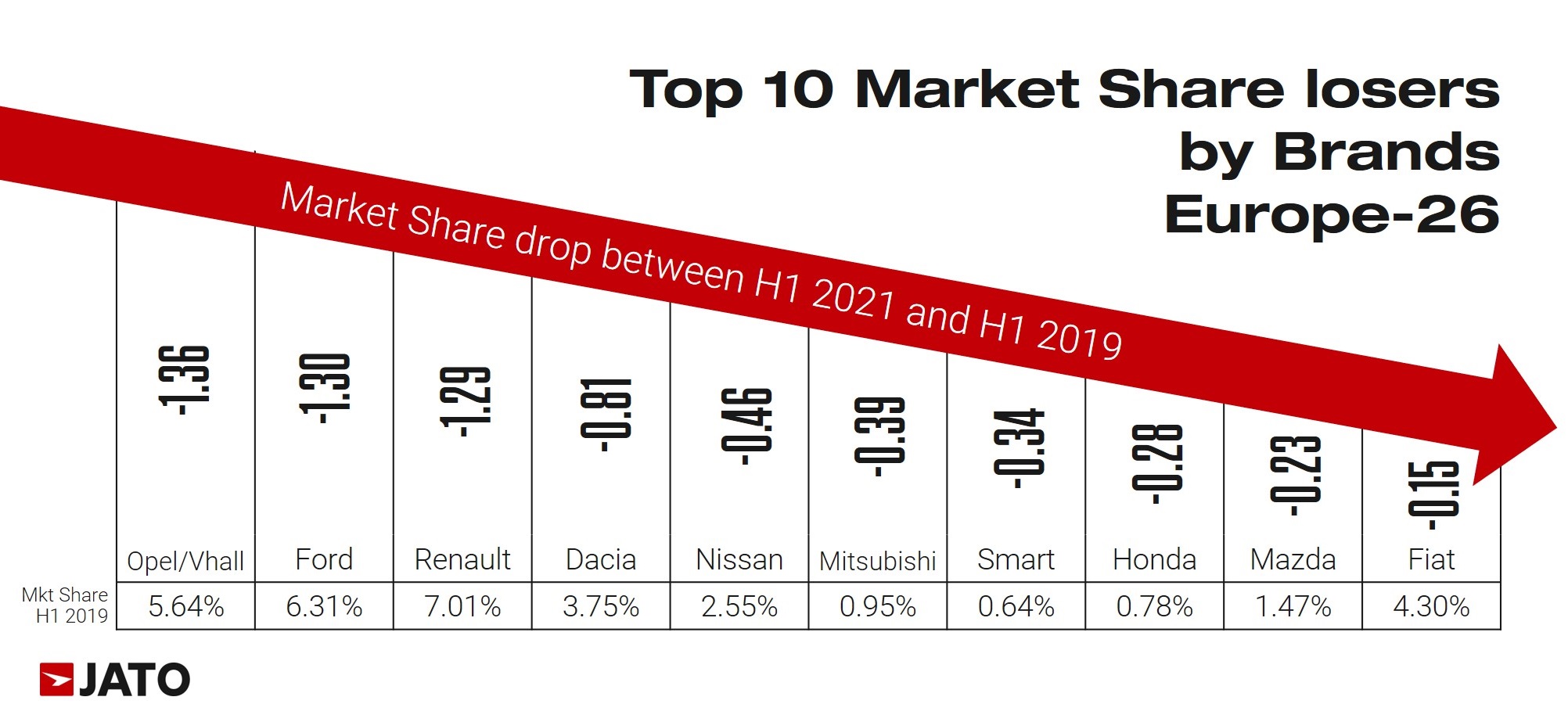

The variation in registrations between the first half of 2021 and 2020 show clear, strong increases. Last year, volume dropped during April and May, meaning that – only two out of the 18 biggest OEMs in Europe did not post double- and triple-digit growth rates in 2021 – volume still increased. The two OEMs to achieve this were Renault-Nissan-Mitsubishi alliance (+4%) and Honda (+2%).

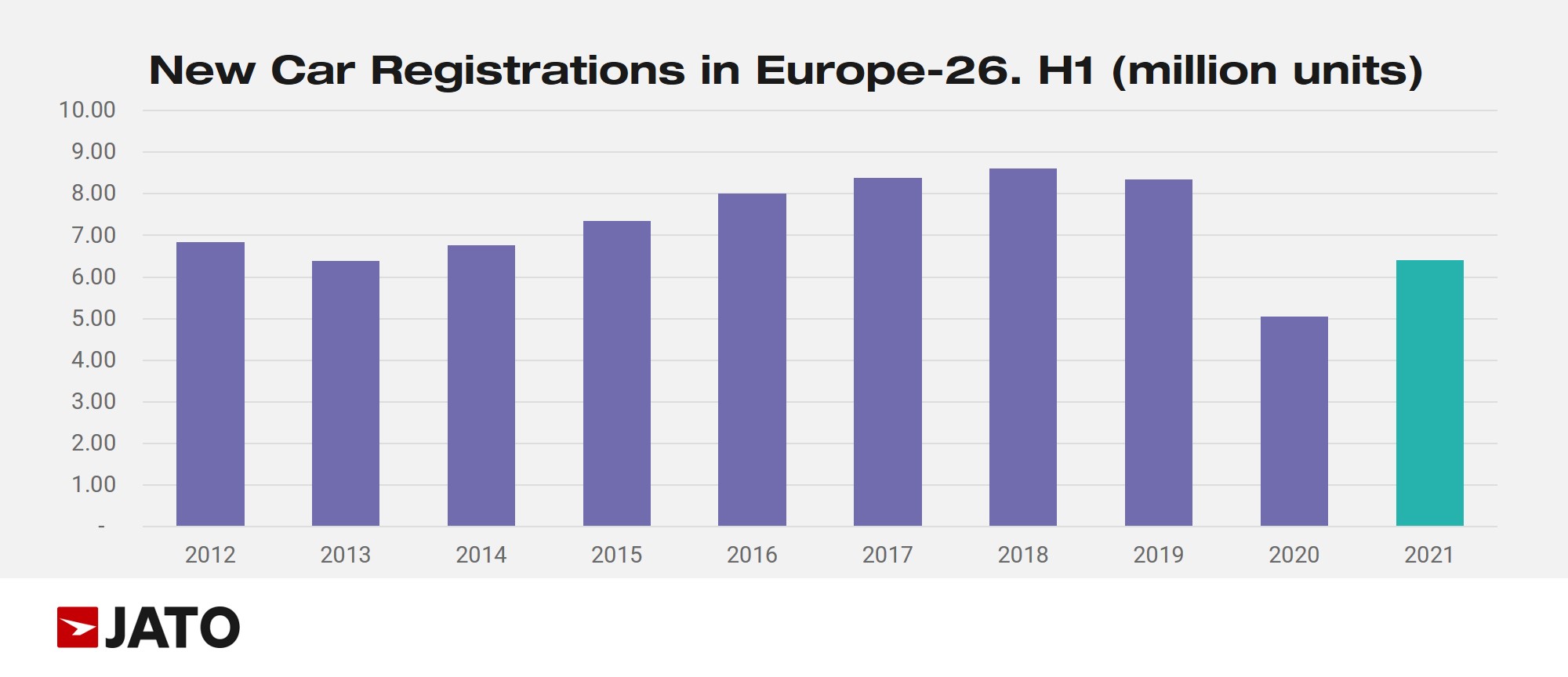

When compared to pre-Covid levels in 2019, a clearer picture emerges. In H1 2019, 8.34 million passenger cars were registered in Europe-26. In 2020, it fell to 5.05 million, and bounced back to 6.42 million in 2021. Between 2019 and 2021, the volume dropped by 23%, demonstrating that the industry has not yet surpassed the Covid-19 crisis. In fact, excluding 2020’s results, 2021 recorded the lowest registrations volume for H1 since 2013.

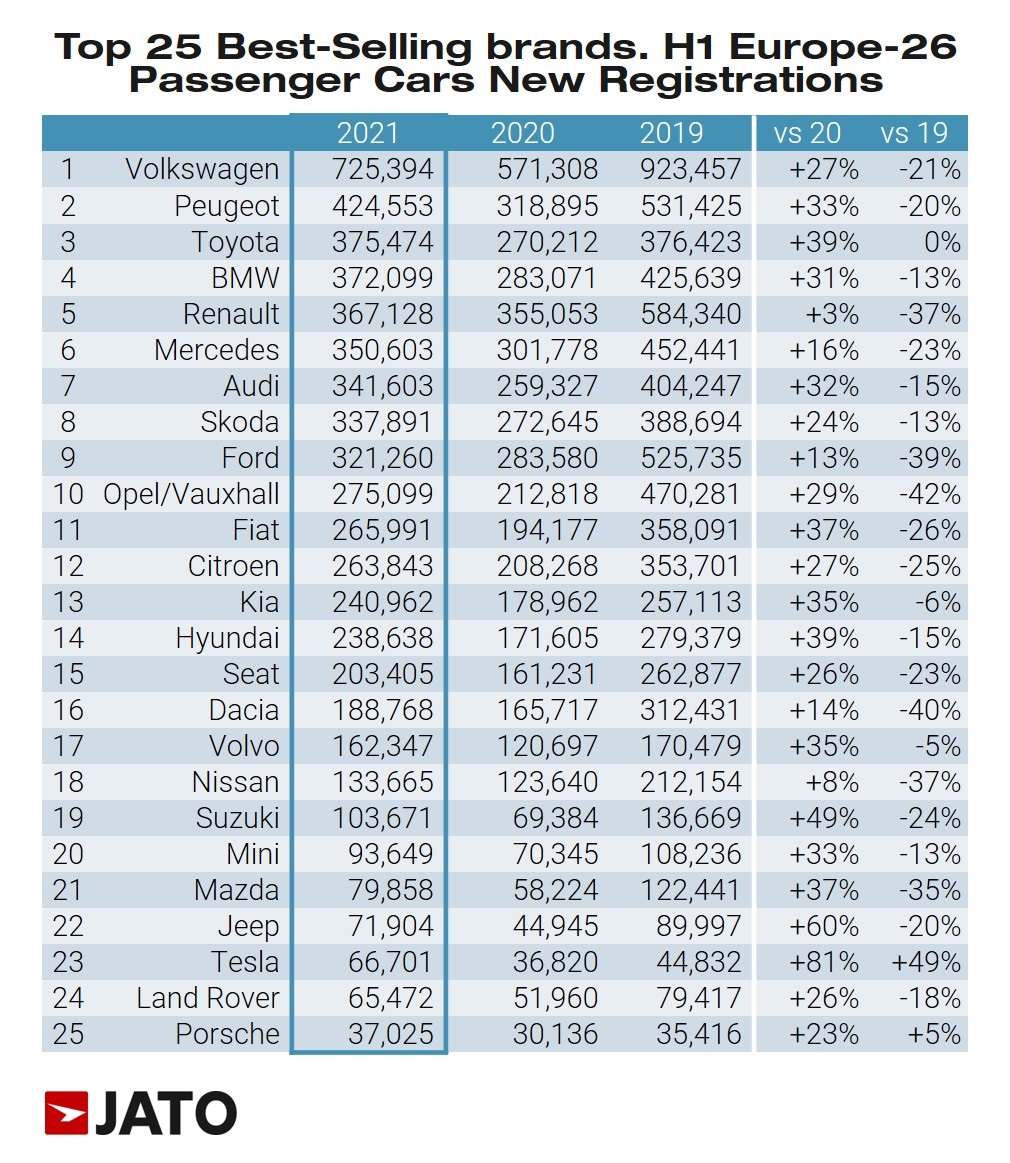

Volkswagen Group takes the crown

Once again, out of turmoil, Volkswagen Group has emerged successful. The German OEM secured the highest increase in market share between H1 2019 and H1 2021 – with the percentage jumping from 24.3% to 26.2%. However, its volume fell by 17%.

Arguably, Volkswagen Group started on its EV journey at the right moment, jumping on the market trend when consumers started to adopt the new technology. Its electric line-up is selling well, leading the EV market ahead of Tesla. They have also worked hard on their SUV offering, continuing to produce models in the segment that attract new clients across Europe.

Volkswagen was followed by Toyota Group (which secured +1.4 points of share) and Hyundai-Kia (with +1.0 points). Toyota’s hybrid line-up – along with the new generation Corolla and Yaris – boosted the group’s presence in Europe. Growth for Hyundai and Kia was spurred on by the popularity of the Hyundai Kona and other electrified models.

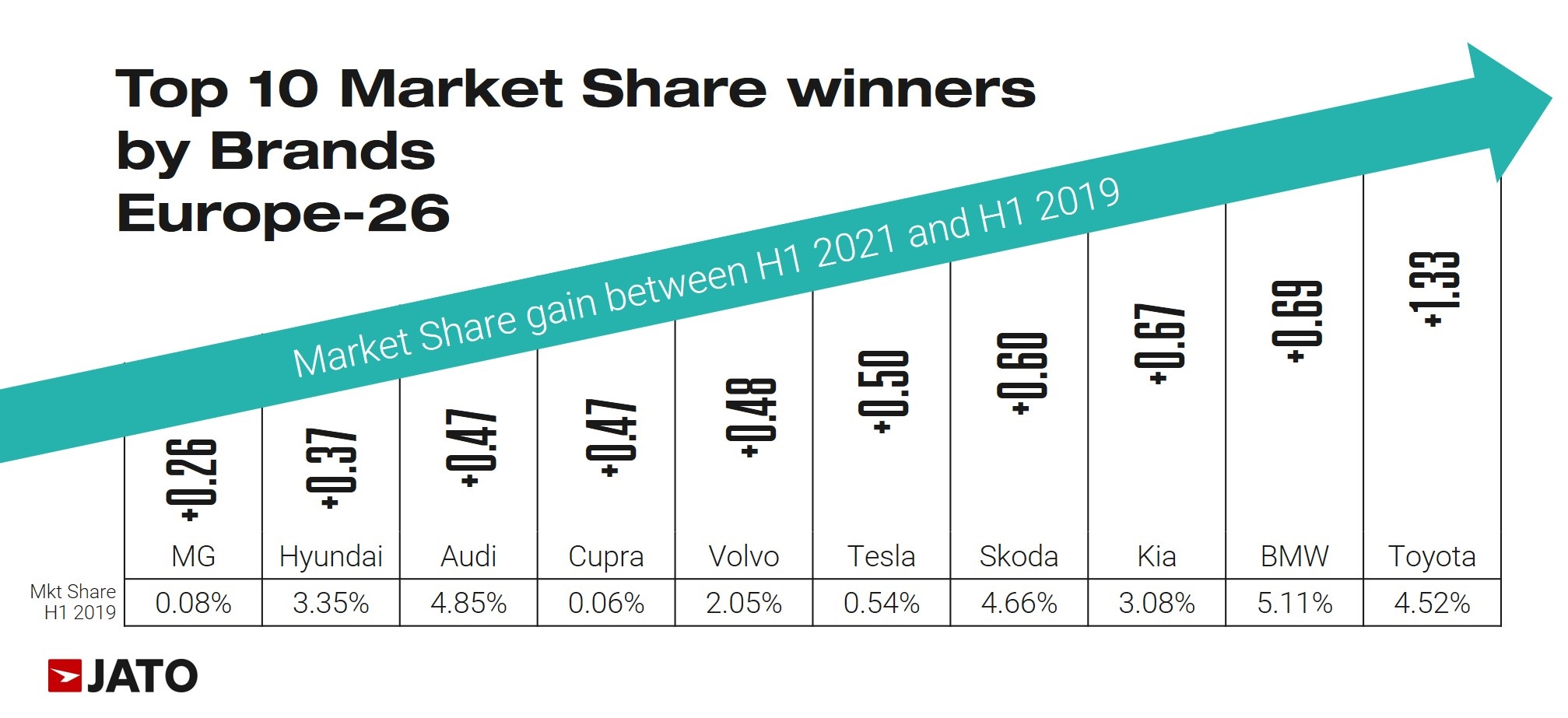

Toyota leads among the brands

Among the brands, Toyota gained the most market share, increasing by 1.4 points, from 4.5% share in H1 2019 to 5.9% this year. The brand benefitted from positive public response to its fourth generation Toyota Yaris, which was the top-selling new car in January 2021, and the third best-selling during H1.

BMW followed Toyota, gaining 0.7 points of share at 5.8% in H1 2021. The latest generation of the 3-Series, X5 and 2-Series boosted its volumes. Kia follows, with almost 0.7 points at 3.8% – positively impacted by the outstanding results of the Kia Niro (despite its age) and the Xceed. Other winners include Skoda (boosted by the Kamiq and Scala), Tesla (the Model 3 was Europe’s top-selling EV) and Volvo, whose XC40 was the top-selling premium car in Europe.

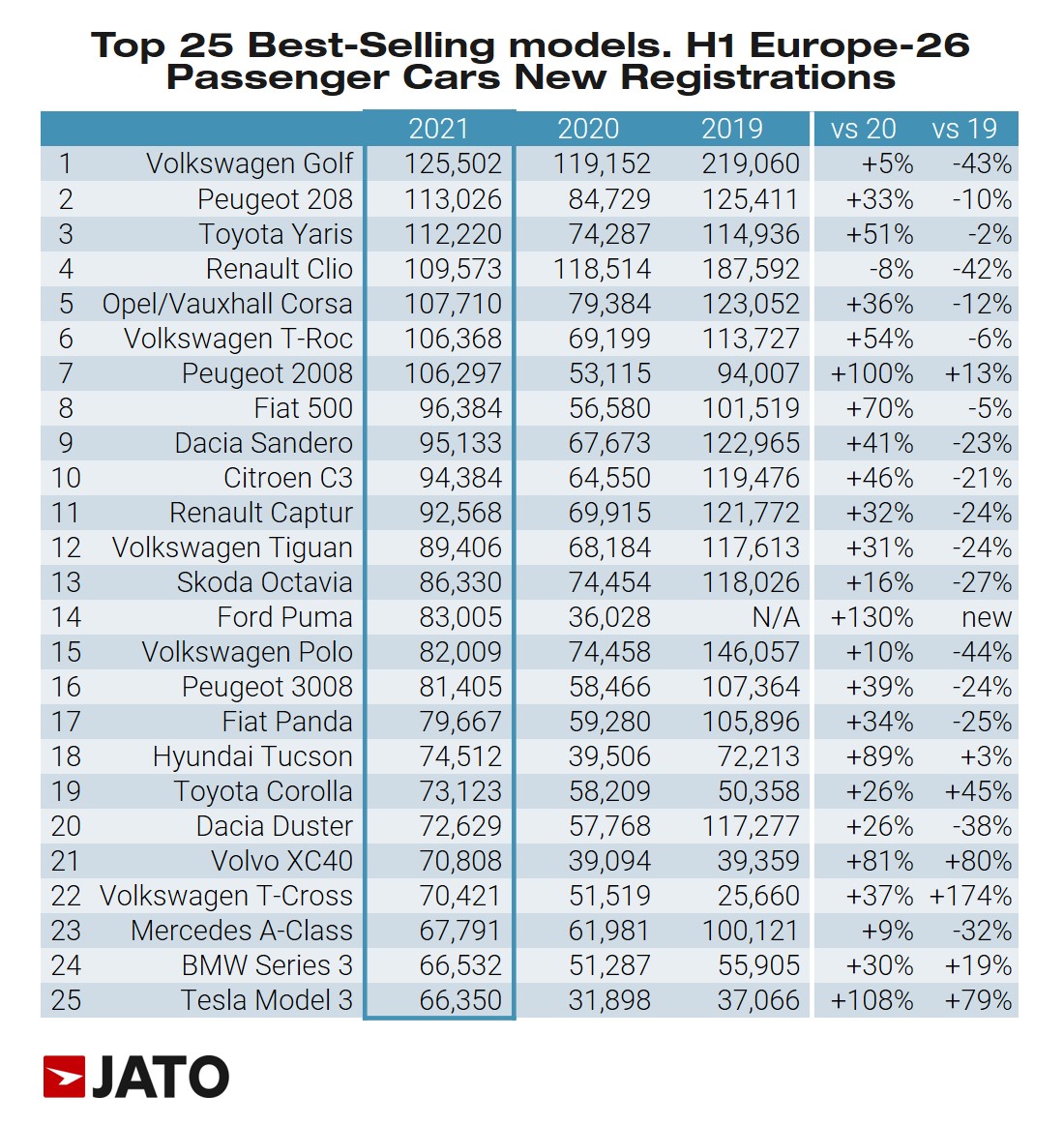

Outperformance for Volkswagen T-Cross, Volvo XC40 and Tesla Model 3

In comparison to H1 2019, the Volkswagen T-Cross, Volvo XC40 and Tesla Model 3 gained the most market share in H1 2021. Market share of the T-Cross soared from 0.31% in 2019 to 1.1% this year, with the registrations volume jumping from 25,700 to 70,400 units. In the case of the Volvo XC40 and Tesla Model 3, their volumes increased from 39,400 to 70,800 units, and 37,100 to 66,400 units respectively.

However, the Ford Puma, which was not available in H1 2019, managed to secure a 1.3% share through June. This increase was the largest among all models. The Puma was Ford’s top-selling model in H1, outselling the popular Fiesta by more than 20,000 units.