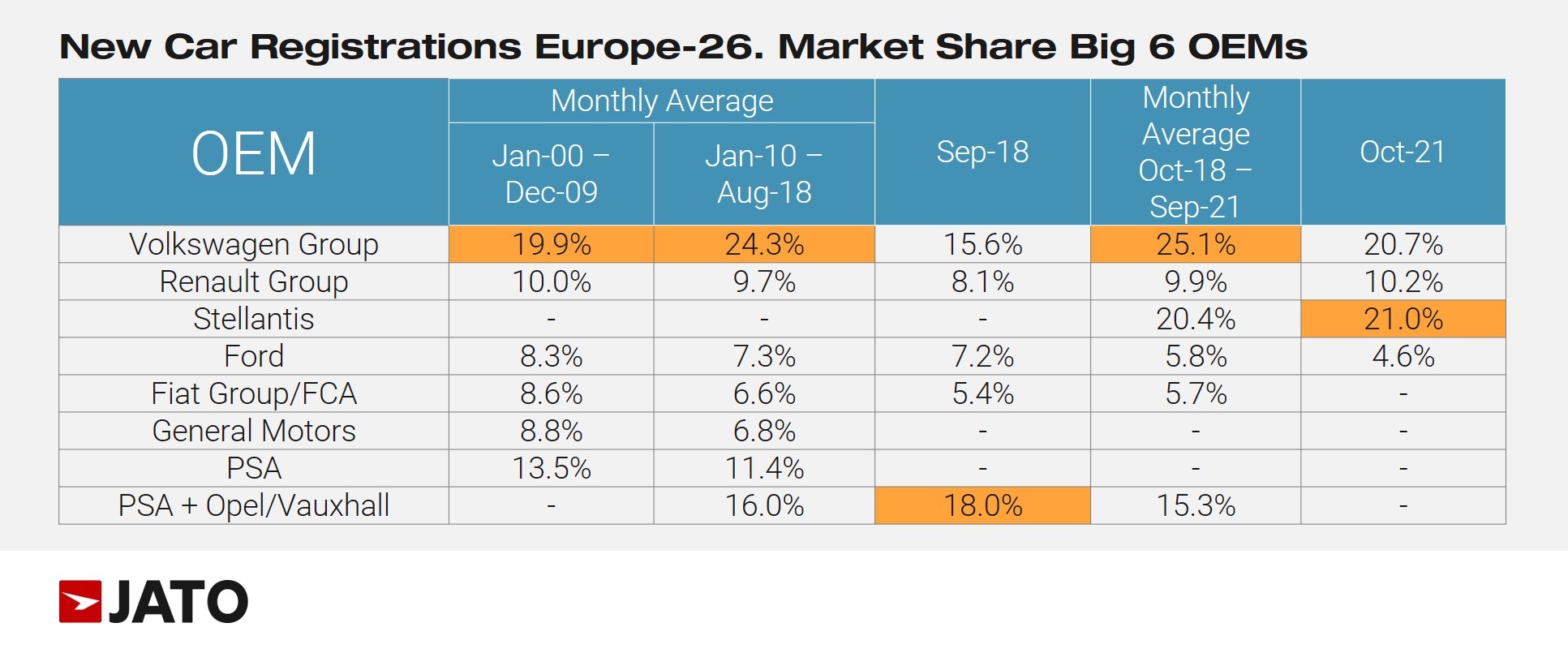

- Stellantis registered more units than Volkswagen Group in October

- The European car market decreased in size due to the ongoing semiconductor shortage

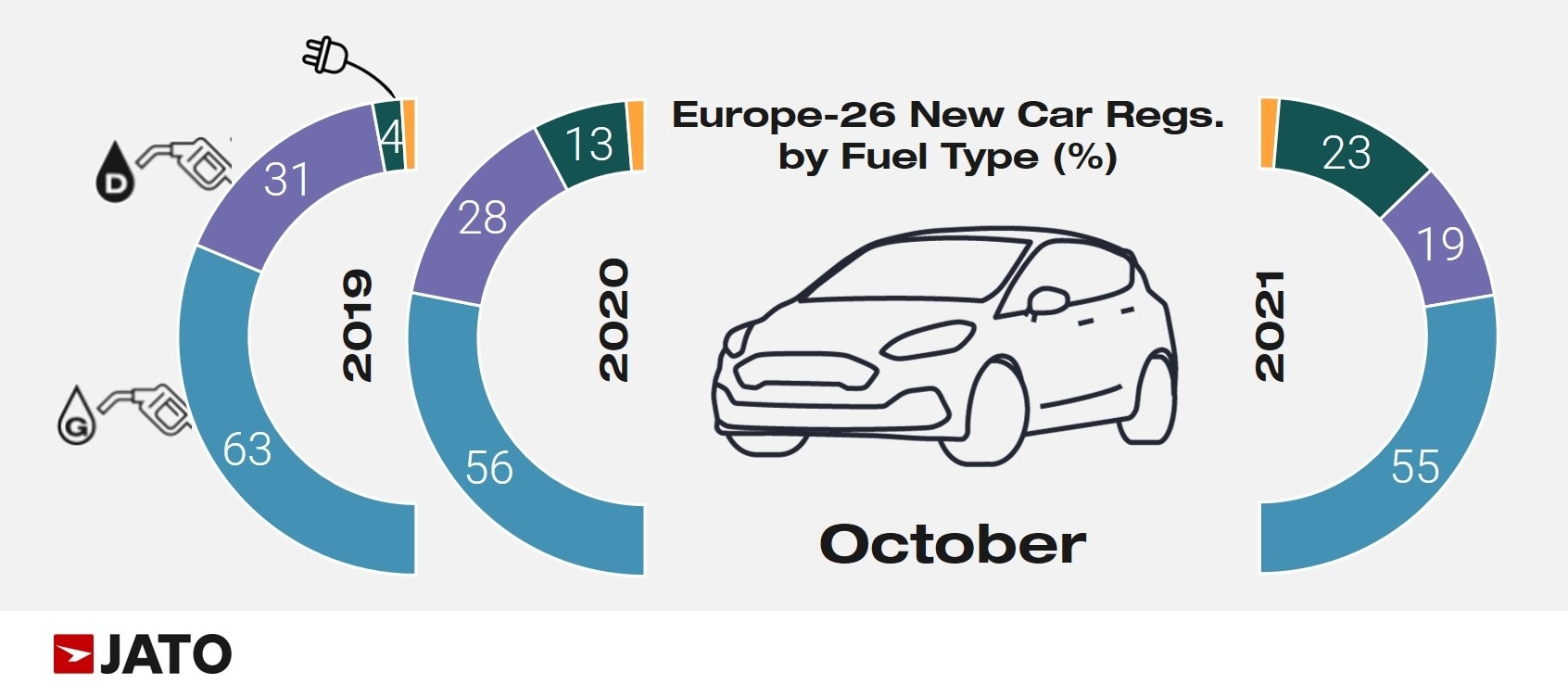

- EVs achieve a new record for monthly market share

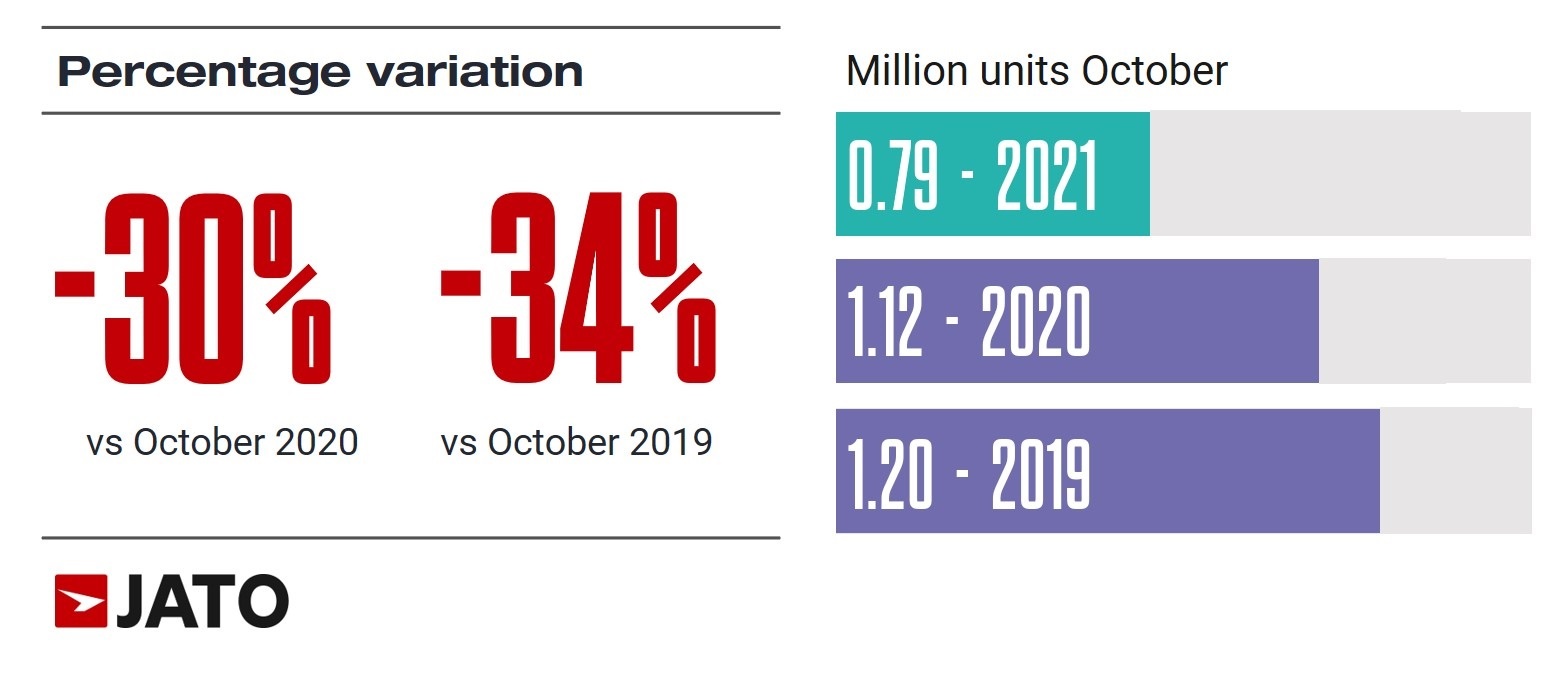

October was a challenging month for Europe’s automotive industry, as total registrations decreased by 30% to 790,652 units caused by the continued impact of shortages of new cars at dealerships. Felipe Munoz, Global Analyst at JATO Dynamics, commented: “The shortage of semiconductors is proving to be as severe as the COVID lockdowns of last year. We have seen factories shutdown across the continent, and at present the industry is struggling to find a solution to the supply chain crisis.”

Year-to-date, the total volume for Europe’s 26 markets continues to outperform in comparison to 2020, up by 2.6% to 9.85 million units – however the gap has once again narrowed when compared with the 7% rise that was seen in September.

The shortages are also having a direct impact on sales leadership across the European market. According to JATO Dynamics’ data, last month was the second time, this century, that Volkswagen Group fell out of the leadership position for monthly registrations ranking by OEM. This marks the first time since its formation earlier this year, that Stellantis has outsold the German manufacturer.

Last month, Volkswagen recorded a 42% decline in volume, with double-digit drops in all countries except Ireland. Its compact and midsize cars were the most severely affected segments. Munoz continued: “Carmakers are being forced to prioritise their best-selling segments, meaning that the few available semiconductors are being used solely to produce SUV and EVs.”

The market share for SUVs jumped from 40.7% in October 2020 to a new monthly record of 46.8% last month. Unlike the traditional segments, demand for SUVs has continued to gain momentum as manufacturers roll out their new EV alternatives. The segment was led by Volkswagen Group, Stellantis and Hyundai-Kia, but only the latter posted notably strong growth at +23%, due to its latest launches. Toyota, in 6th position, also saw its volume increase by 3%.

During the month, a total of 181,300 units of BEV and PHEV were registered, accounting for 22.9% of total market share – a new monthly record. While the EV segment continues its upward trajectory, diesel vehicles are struggling to gain traction in Europe, with market share dropping to just 19%. Munoz added: “As we saw during the pandemic, the current crisis has proved to be more of an opportunity than a threat to the developing EV market. COP 26 marked a significant turning point for the industry as 24 countries and 11 OEMs committed to no longer producing ICE vehicles by 2040, and so the shift towards EVs will only accelerate further in the coming years.”

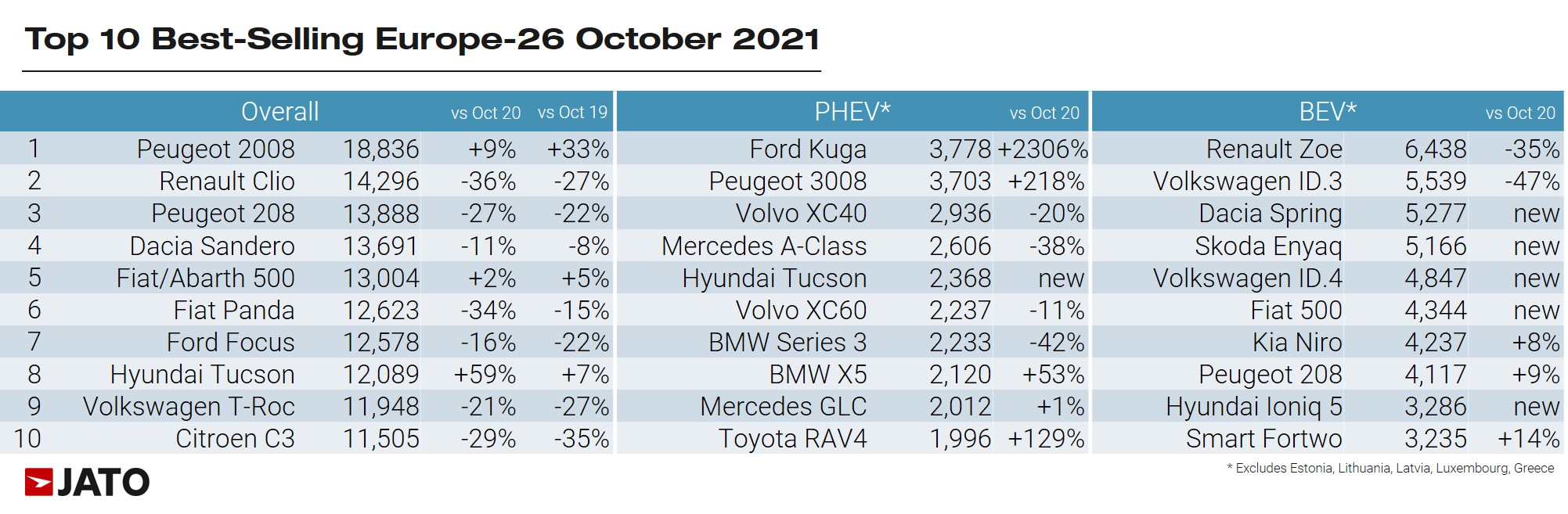

As a consequence of the crisis, there was considerable change in the rankings by model. The Peugeot 2008 secured the top spot for the first time since its introduction in 2013. Stellantis saw 5 of its models in the top 10, followed by Renault group with 2 models, and Volkswagen Group, Ford and Hyundai with one model each.

The Hyundai Tucson again performed well, up by 59% thanks to the new generation. Strong results were also posted by while the Volkswagen T-Cross +10%; BMW X3 +74%; Kia Sportage and Ceed, +23% and +26% respectively; Mitsubishi Space Star +45%; Ford Ecosport +36%; Tesla Model 3 +236%; Porsche Macan +38%; BMW 4-Series +31%; Volkswagen Arteon +103%; Porsche Taycan +41%; the Lexus UX + 28%.

Among the latest launches, the Opel/Vauxhall Mokka secured a place in the SUV top ten; the C4 became Citreon’s second best-selling vehicle; Renault’s Arkana outsold the Megane and Kadjar, and the Dacia Spring was the third best-selling BEV, behind the Renault Zoe and the Volkswagen ID.3.