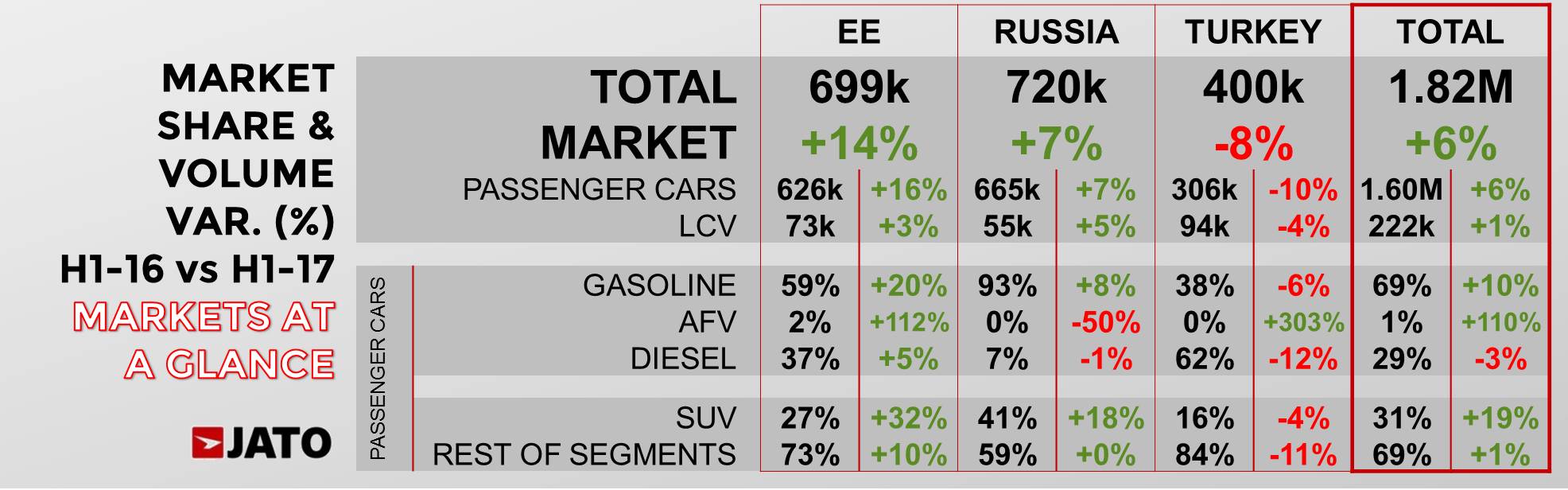

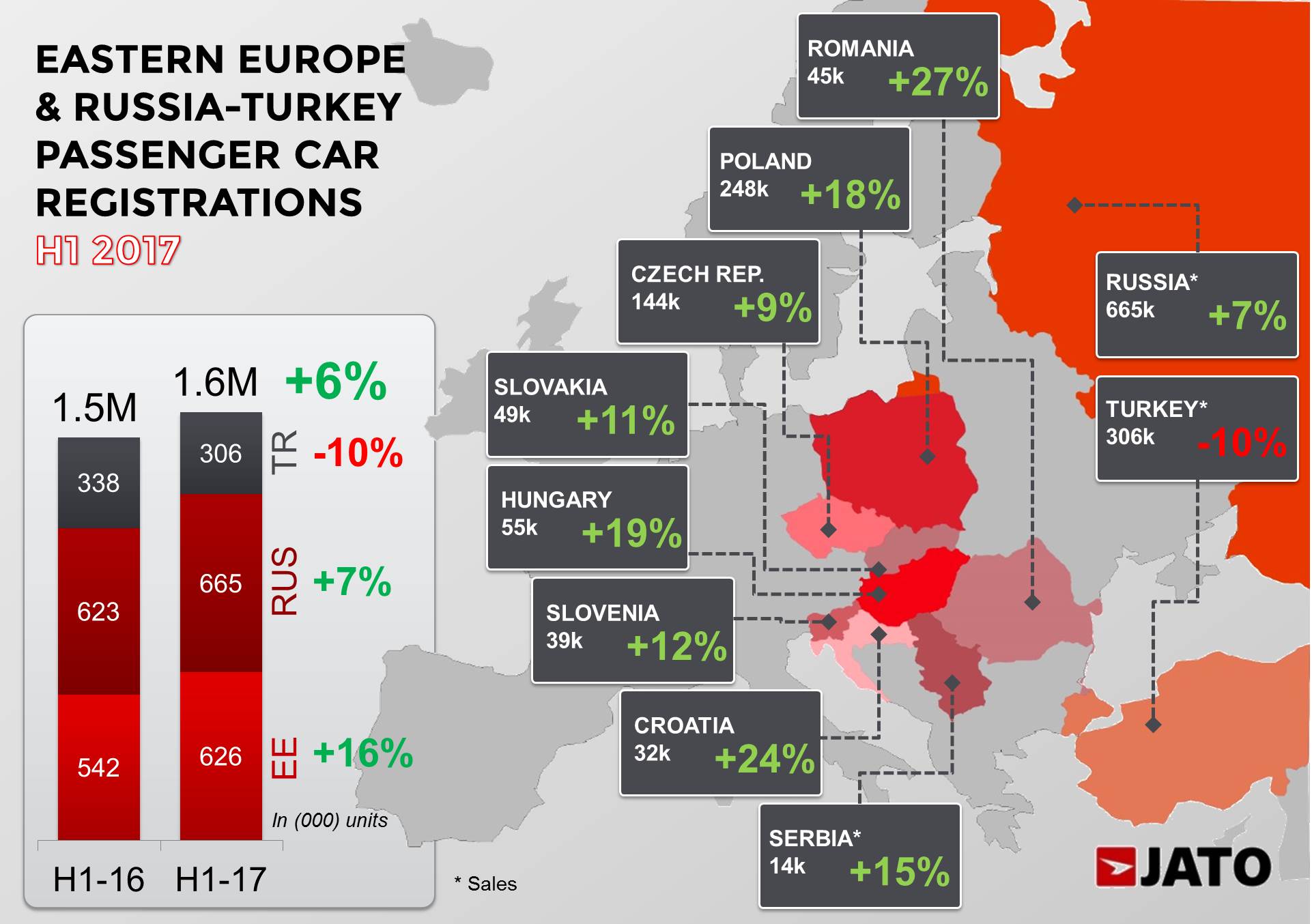

- Eastern European countries (Croatia, Czech Republic, Hungary, Poland, Romania, Serbia, Slovakia and Slovenia) have been analysed as a region; total registrations (passenger cars and LCVs) increased by 14.1% to 698,900 units in H1 2017

- Russia and Turkey have been analysed separately, with Russia signalling the steady recovery of its automotive market

- The Kia Rio was the best-selling model across the whole region, whilst the Skoda Octavia maintained its position as Eastern Europe’s most popular car model

The Eastern European car industry (excluding Russia and Turkey) grew in the first half of 2017 with new registrations for passenger and LCVs up 14.1% compared to 2016, with 698,900 units registered. This was driven by a strong performance across the region, with seven out of the eight Eastern European markets analysed recording double digit growth. Romania led the region, with an increase in registrations of 26.2%. Poland, the largest market in the region, recorded a significant 15.5% increase, registering 277,700 units, meaning the country is now the seventh largest market in Europe in terms of volume.

The positive performance of Eastern Europe can be attributed to increased demand for passenger cars, with registrations increasing by 15.5% to 626,100 units. Petrol vehicles also performed well, growing by 20% in H1 2017, to account for 59% of the total market. In comparison, diesel cars accounted for only 37% of the total market, and market share decreased by just 3 percentage points compared to 2016.

The passenger car market in Eastern Europe was dominated by VW Group, due to the strength of the Skoda brand in the region. Its double digit growth meant it accounted for more than double the volume of its nearest rival Renault-Nissan, yet VW Group has lost market share when compared to 2016. Renault-Nissan was bolstered by the strength of the Dacia brand, which benefits from both from being a local manufacturer and its low-cost product offering, which appeals to the region. PSA secured third place in the manufacturer ranking due to the strength of the recently acquired Opel brand in markets such as Croatia, Hungary and Poland. The manufacturing presence of car makers in the region has also played a significant role, with Hyundai-Kia capitalising on its presence in the Czech Republic and Slovakia to secure double-digit market share in these countries.

“The recent economic upturn in the Eastern European region is the key driver behind the positive performance in H1 2017. The political and economic instability in key global markets has pushed investment to Eastern Europe, which has benefitted from its proximity to Western Europe and positive signs such as declining unemployment, strong industrial production levels and reassuring retail sales volumes. As a result, economies in the region have grown significantly, with Romania recording a significant economic growth of 1.7% during Q1 2017. In terms of the region’s automotive industries, many of these economies produce vehicles locally. Local demand has been boosted as a result of increased product ranges across a number of manufacturers that now incorporate city-cars and luxury SUVs,” commented Felipe Munoz, Global Automotive Analyst at JATO Dynamics.

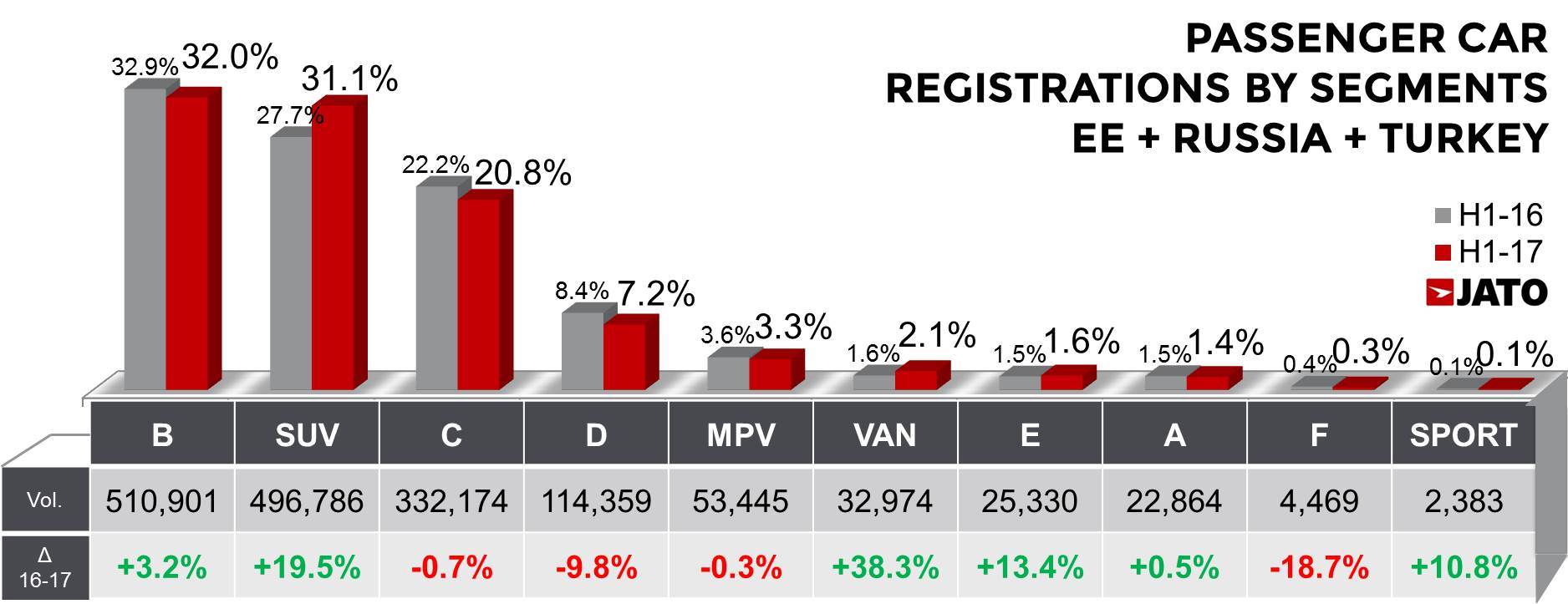

As with Western Europe, the growth in Eastern Europe has been driven by SUVs, which accounted for 27% of total registrations. The compact and subcompact segments have continued to be popular in the region with both recording double digit increases, but underperforming when compared to the total market’s average increase. In the model ranking, following a similar pattern to its Western European cousin the Golf, the Skoda Octavia leads in terms of total registrations. However, as with the Golf, the Octavia has lost market share. Other notable models include the Dacia Duster, which performed well, despite the impending launch of a new generation of the model. The Renault Clio, Suzuki Vitara, Dacia Sandero, Renault Megane, Volkswagen Tiguan and Fiat Tipo all also performed well.

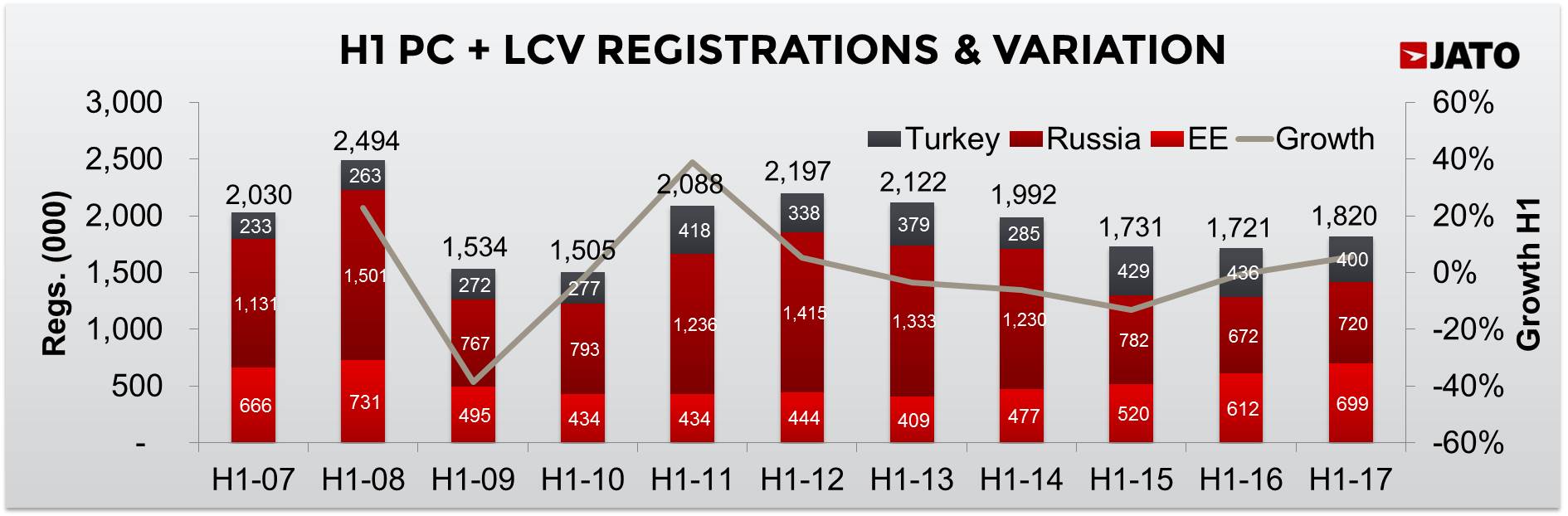

Outside of the core Eastern Europe market, Russia posted an increase of 6.7% when compared to last year. This growth signals that the country is beginning to recover following an economic downturn. However, in terms of volume it is still half of the size recorded in H1 2012, when it was the second largest European market and challenged Germany for dominance of the automotive industry in Europe.

Manufacturers with a strong established presence in the country are continuing to dominate the market. Renault-Nissan recorded 38.0% market share in H1 2017, and an increase in volume of 11% compared to last year; this can be attributed to the strength of the Lada and Renault brands in the country. Hyundai-Kia also dominates, with a market share of 23.8%, which was an increase of 2 percentage points, following a sales increase of 15.4%. This strong performance was driven by the Kia brand which posted a 22.1% increase which can be attributed to the Rio, the country’s best-selling model.

In Turkey, 400,000 units were recorded (cars and LCVs), meaning that the country’s registrations declined by 8.3% compared to last year, whilst the passenger car market totalled 305,700. Registrations of passenger cars in Turkey have been negatively impacted by the increase of consumption taxes that have been applied to cars that cost more than 40,000 Lira and the impact of this is clear in the segment figures for the Turkish market. Midsize, executive and luxury sedan sales declined by 23%, while compact, midsize and big SUV registrations declined by 9.5% in H1 2017. In stark contrast, small SUVs posted an 8.5% increase. Turkey remains one of the only global markets where SUVs do not dominate, this is largely due to the fact the country relies on imported SUVs which are vulnerable to high taxes.

“Russia and Turkey are performing very differently to Eastern Europe – whilst Turkey recorded a disappointing result, Russia showed signs of a tentative recovery. The first half of 2017 represented the best H1 result for the Czech Republic, Poland, Slovakia and Slovenia for the past decade in terms of car and LCV registrations, whilst for Eastern Europe in general (excluding Turkey and Russia), the period represented the highest H1 volume since H1 2008. As Western Europe and other global markets experience uncertainty, it will be interesting to see how the growth we’ve observed in Eastern Europe progresses and how countries such as Serbia and Romania fare, as they are far from the peaks we saw in 2008,” concluded Felipe Munoz, Global Automotive Analyst at JATO Dynamics.