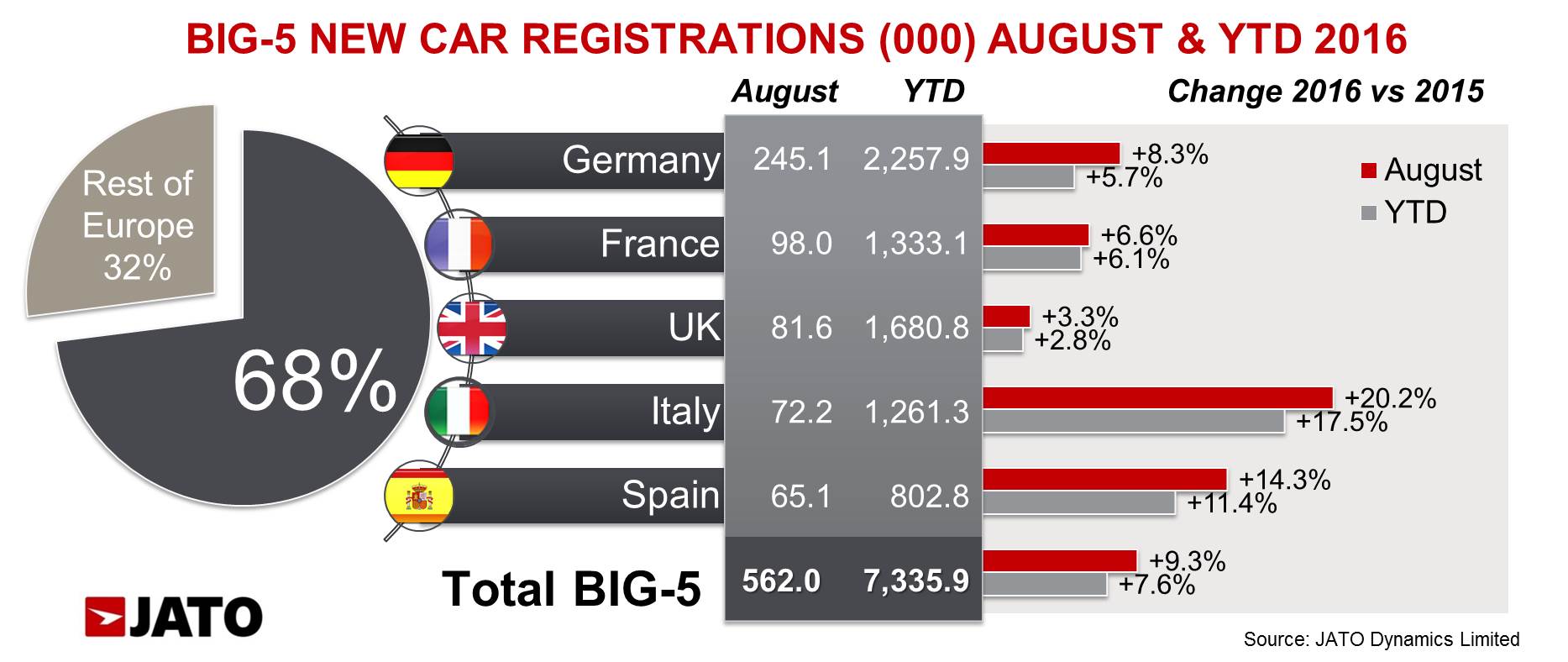

- Italy saw its best August results since 2009, increasing car registrations by 20.2%

- Spain’s market was boosted by an outstanding growth on rental car registrations, which were up 48%

- Year-to-date registrations were up 7.6%, with 7.33 million units registered overall so far this year

Registrations in Europe’s ‘Big 5’ markets saw a healthy increase of 9.3% in August, as market conditions improved following the 2% decline seen in July. Overall, registrations for August totalled 562,046 units, up from 514,428 in August 2015. Registrations YTD totalled 7.33 million units which is a 7.6% increase on the same period in 2015, SAAR figures came in at 10.92 million units.

While all five markets posted positive growth, Italy was the leader, posting its best August results since 2009 with a 20.2% increase on the same month last year, going from 60,065 units in August 2015 to 72,179 units in the same period this year, in part due to an additional working day. The Spanish market grew by 14.3% compared to the same period last year, largely due to record tourist numbers resulting in a 48% increase in rental car registrations. Europe’s largest market, Germany, posted an 8.3% increase, compared to the same period last year. This was driven by growth in private registrations which were up 19% on last year due to positive economic development, a healthy level of employment, and two additional working days in August. Both France and the UK posted a modest growth of 6.6% and 3.3% respectively.

While all five markets posted positive growth, Italy was the leader, posting its best August results since 2009 with a 20.2% increase on the same month last year, going from 60,065 units in August 2015 to 72,179 units in the same period this year, in part due to an additional working day. The Spanish market grew by 14.3% compared to the same period last year, largely due to record tourist numbers resulting in a 48% increase in rental car registrations. Europe’s largest market, Germany, posted an 8.3% increase, compared to the same period last year. This was driven by growth in private registrations which were up 19% on last year due to positive economic development, a healthy level of employment, and two additional working days in August. Both France and the UK posted a modest growth of 6.6% and 3.3% respectively.

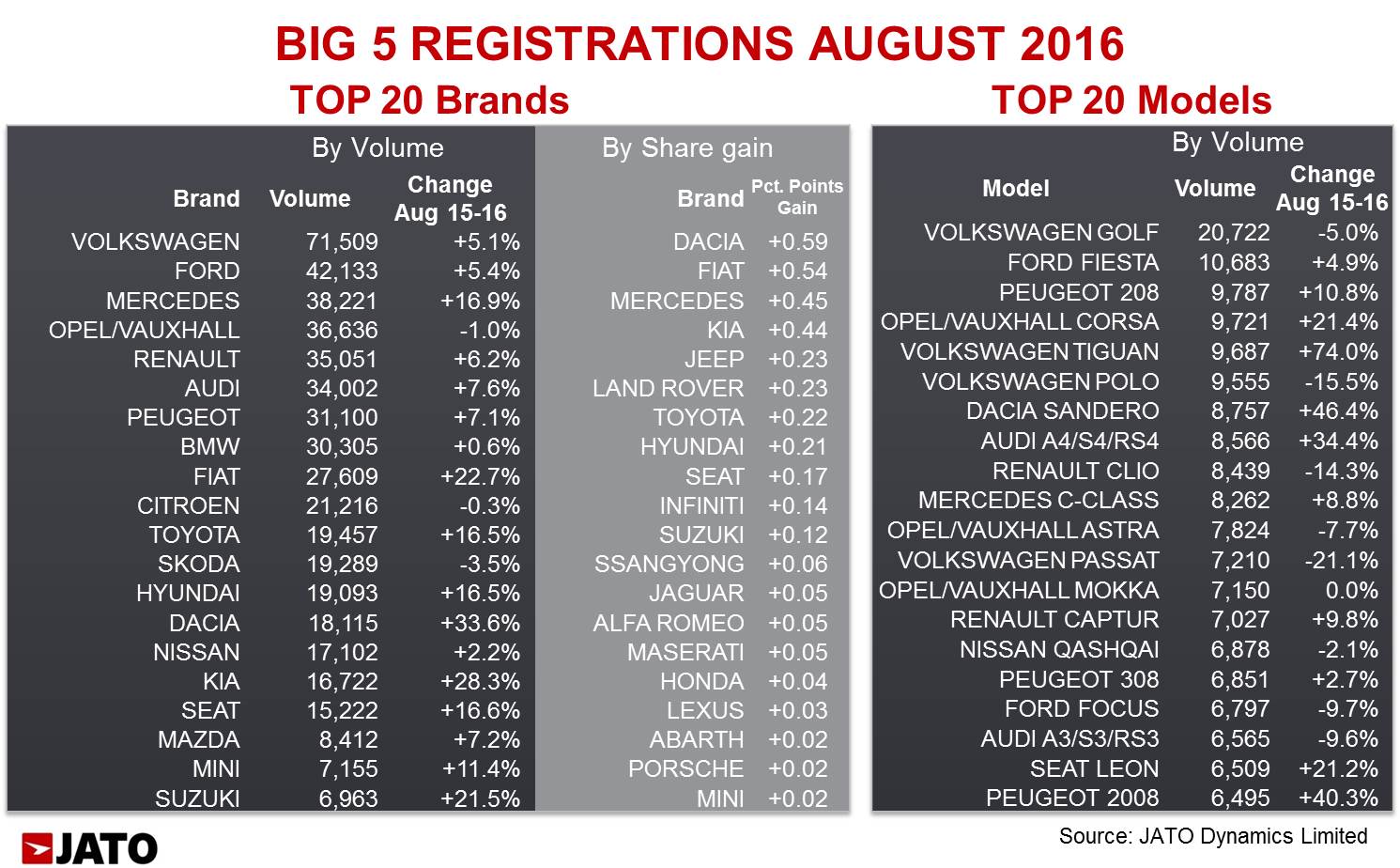

Volkswagen Group remained Europe’s largest car maker, posting a 5.8% increase on last year, having registered 143,324 units in August 2016 compared to 135,483 units in August 2015. However overall, the German group lost market share, recording the biggest market share drop of all the car makers analysed, going from 26.3% in August 2015 to 25.5% in 2016 as double digit growth in Germany was offset by falls in the UK and France. In contrast, Renault-Nissan alliance registrations grew by 12.2%, taking its overall market share to 12.7%, compared to 12.4% last year. The group saw strong growth of 27.3% and 32.7% in Italy and the UK respectively, which was particularly boosted by a 33.6% increase posted by Dacia, which outsold Nissan in the ranking. PSA and Ford both lost market share, whilst Opel/Vauxhall dropped by 1% and fell one position in the brand ranking.

Volkswagen Group remained Europe’s largest car maker, posting a 5.8% increase on last year, having registered 143,324 units in August 2016 compared to 135,483 units in August 2015. However overall, the German group lost market share, recording the biggest market share drop of all the car makers analysed, going from 26.3% in August 2015 to 25.5% in 2016 as double digit growth in Germany was offset by falls in the UK and France. In contrast, Renault-Nissan alliance registrations grew by 12.2%, taking its overall market share to 12.7%, compared to 12.4% last year. The group saw strong growth of 27.3% and 32.7% in Italy and the UK respectively, which was particularly boosted by a 33.6% increase posted by Dacia, which outsold Nissan in the ranking. PSA and Ford both lost market share, whilst Opel/Vauxhall dropped by 1% and fell one position in the brand ranking.

The big winner of the month was Daimler, with Mercedes posting double-digit gains in all of the five markets and becoming the third best-selling brand of the month. FCA increased its market share by 0.78 percentage points due to the double-digit growth of its Fiat, Jeep, Alfa Romeo and Abarth brands, a 173% increase in sales at Maserati. Hyundai-Kia grew by 21.7%.

“As the market continues to shift and Volkswagen brands continues to slowdown, other brands continue to improve in the mainstream market, such as Dacia, Fiat and Hyundai-Kia which have all seen strong growth, whilst in the premium market, Mercedes is continuing to perform well,” said Felipe Munoz, Global Automotive Analyst at JATO Dynamics.

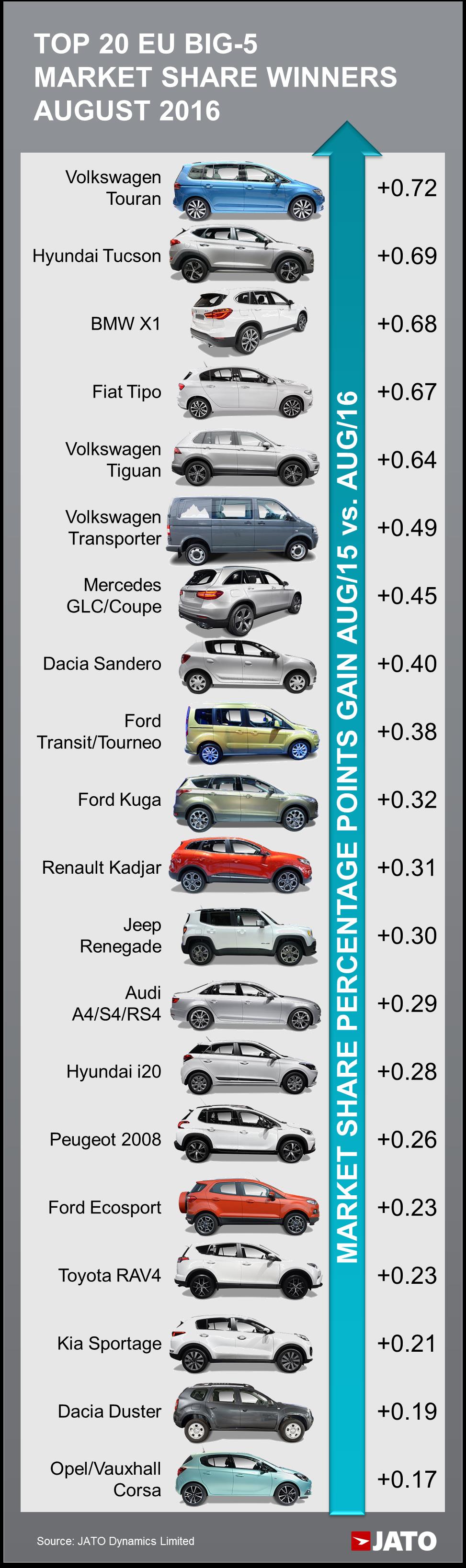

SUVs continued to boom, accounting for 25.9% of the total market, which is a dramatic increase considering the segment barely outsold subcompact (B-Segment) vehicles in August 2015. The SUV segment’s outstanding growth can largely be attributed to midsize and compact SUVs which posted increases of 55.1% and 36.1% respectively. Particularly noteworthy is the new Volkswagen Tiguan, which posted a 74% increase and was the best-selling SUV across the five markets and the fifth best-selling model overall. The Tiguan outsold the popular Nissan Qashqai which posted a 2.1% decline, and was significantly ahead of the fast-growing Kia Sportage (+41.3%), Hyundai Tucson (+326.4%) and Renault Kadjar (+79.9%). In the B-SUV segment the Opel/Vauxhall Mokka maintained its lead, despite recording a 0% growth, but was closely followed by the Renault Captur which recorded a 9.8% increase compared to the same period last year. Other big winners in the segment included the Peugeot 2008, Ford Kuga and Dacia Dusta which posted increases of 40.3%, 52.9% and 34.6% respectively.

The Subcompact segment (B-Segment) was boosted by the Dacia Sandero which increased registrations by 46.4% compared to the same period last year, and was the seventh best-selling model across the five markets in August 2016. The Peugeot 208 outsold its popular rivals Renault Clio (down 14.3%) and Volkswagen Polo (down 15.5%) to become the second best-selling subcompact.

The model ranking was again led by the the Volkswagen Golf which remained the best-selling car across the five markets, selling 20,722 units, posting a 5% decline when compared to the same period last year. Despite posting a 7.5% increase in Germany, double digit drops across the other markets hindered the model’s performance. Despite this, the Golf’s volume was more than double that of the Opel/Vauxhall Astra, which was second in the C-Segment ranking posting a decline of 7.7%. The segment’s big market share winners were the Fiat Tipo, Mini Clubman and Seat Leon.

“While the latest Volkswagen models have helped the brand offset drops posted by their traditional products, other brands gained market share by taking advantage of the booming SUV segment,” concluded Munoz.