Last week at the presentation of the all-new Volkswagen Polo, one thing came to my attention – the new subcompact won’t be offered in a 3-door option. This is the consequence of the shocking sales drop posted by this body-type during the last few years. There is an evident trend in the European passenger cars market. Overall, the market is continuing to grow, beating pre-crisis levels and remaining stable. However, European consumers are displaying a change in preferences when it comes to body-type. Much has been said and written about the SUV boom and its importance to the automotive sector’s growth, but there is another overriding trend of recent years – the financial crisis and its impact is forcing drivers to think more rationally about body-type when purchasing a car.

Consumers now think carefully about the balance between comfort, usability and design, especially European consumers looking for small cars. We are seeing a shift, design is no longer the primary concern of consumers – convenience is increasingly important. This explains why 3-door hatchbacks are disappearing from European roads.

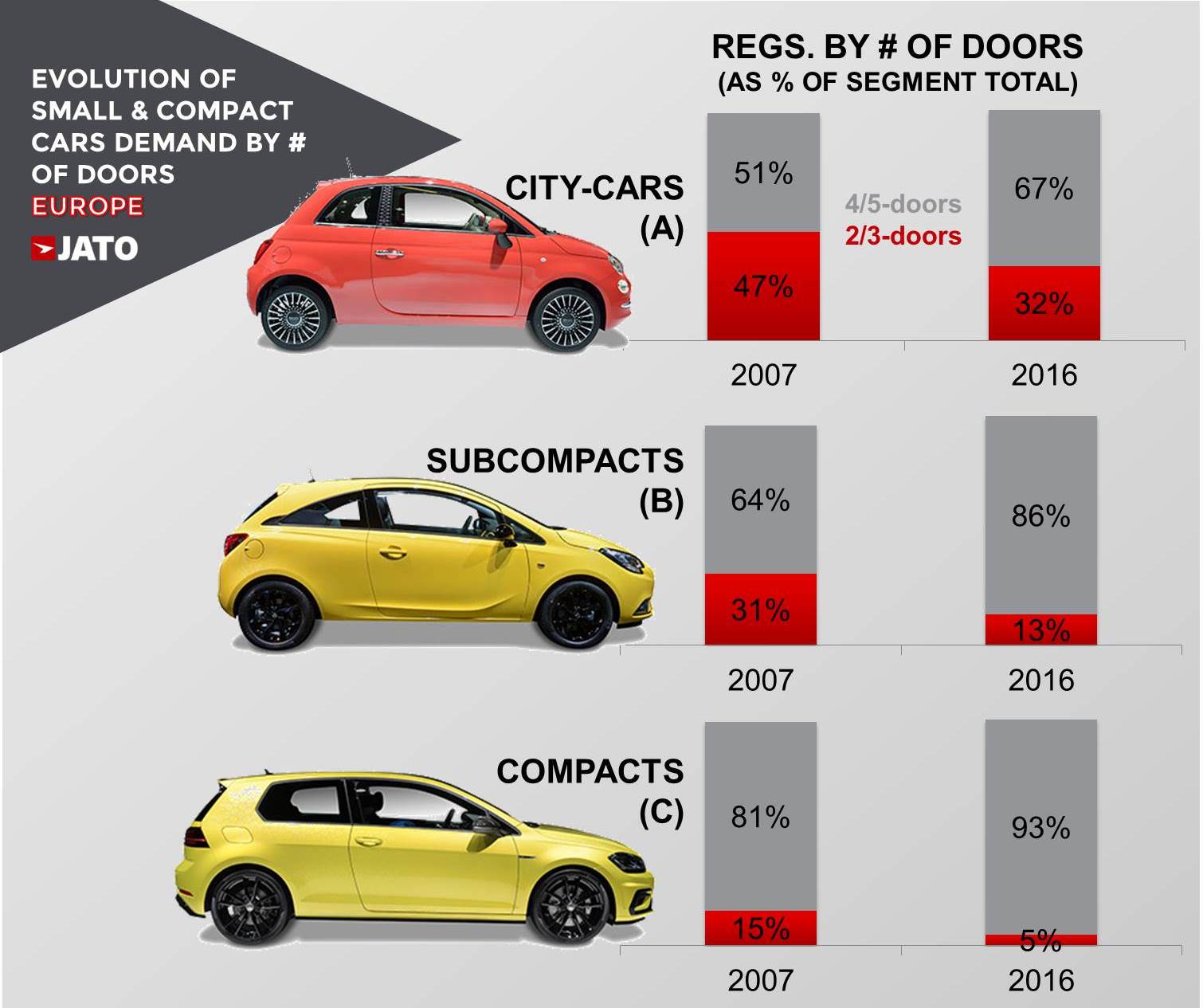

3-door hatchbacks are cars that sit in the A, B and C segments that usually feature the same characteristics and look of their 5-door counterparts. However, some make use of more aggressive designs and are positioned as the “sporty little hatches” in the market. In the current climate, this positioning is no longer valid, with consumers becoming more rational in their decision making since the European financial crisis of 2009-2013. What’s the evidence for this?

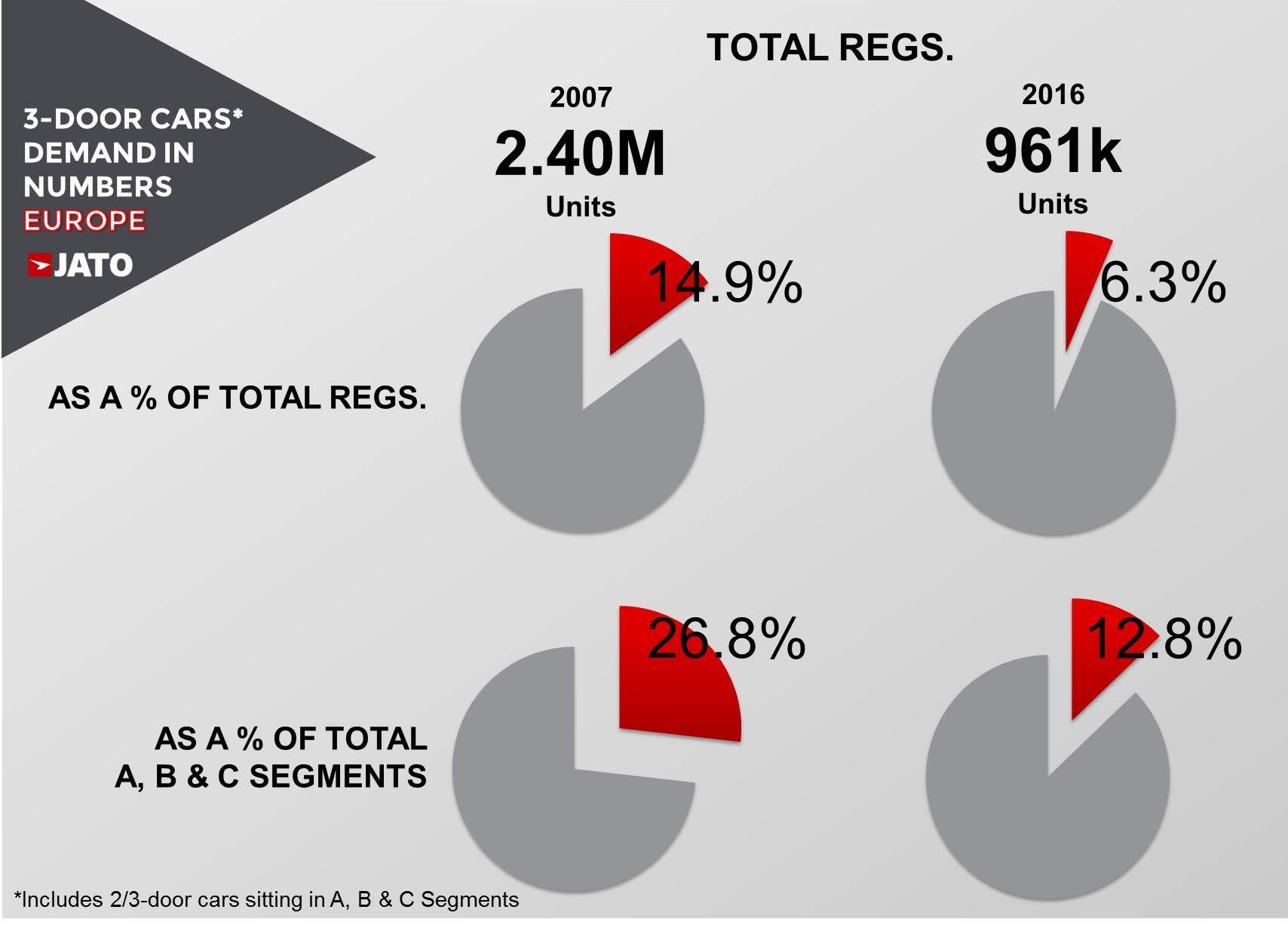

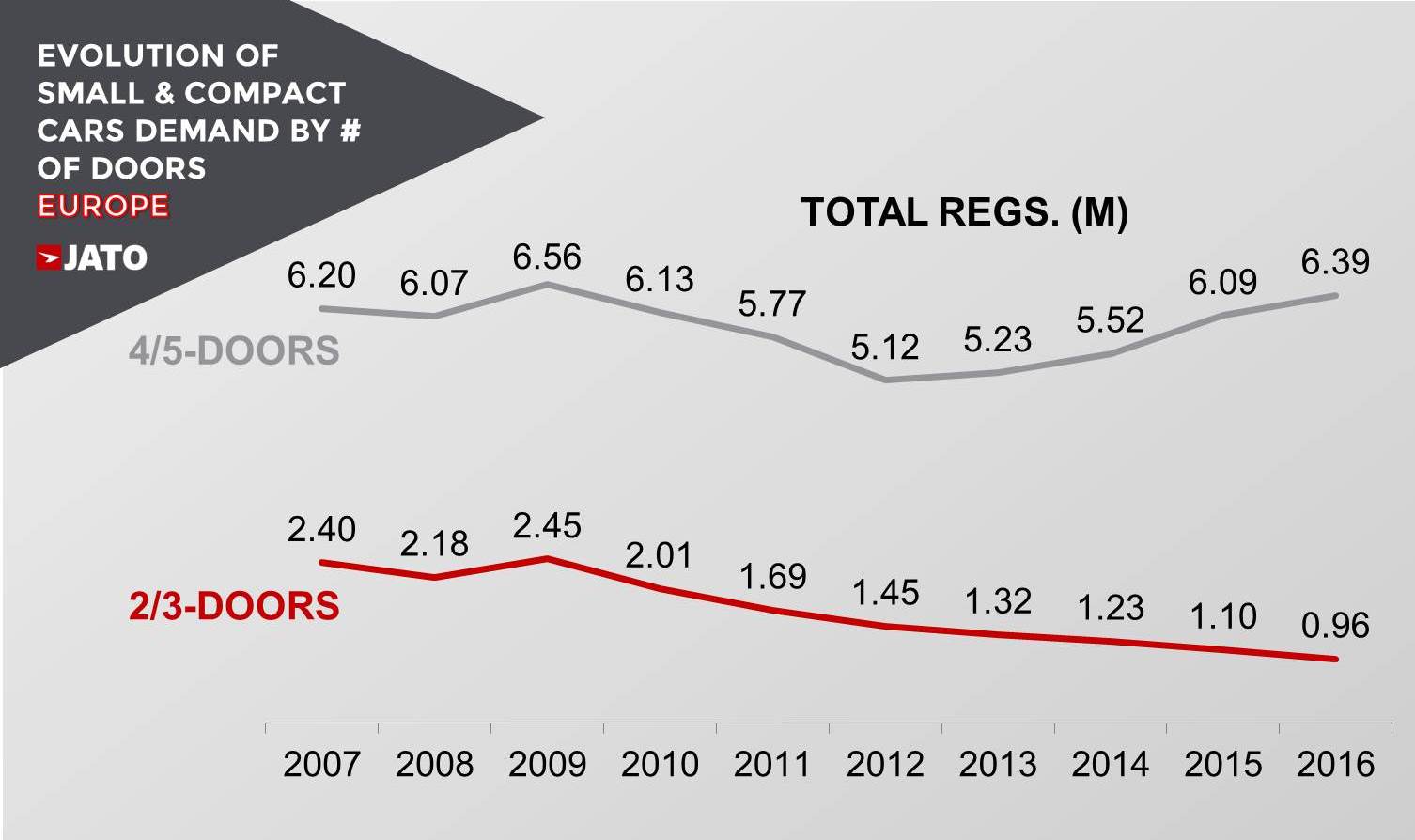

In 2007 the 2/3-door mini (A-Segment), subcompact (B) and compact (C) cars accounted for almost 15% of total European registrations. They were a valid option for people looking for an emotive or ‘exciting’ driving experience within a small car. These cars were positioned to give a sense of ‘sportiness’ to single people, couples or even youngsters looking for their first car. Demand rose to 2.4 million units in 2009, accounting for almost 17% of total market.

But, as the financial crisis hit, consumer priorities changed. Since then, the market share of small and compact 3-door cars posted a shocking decline from 2.45 million units in 2009 to 961,000 units in 2016. It was the first time in many years that less than 1 million customers opted for a 3-door car. Their market share shrank by more than 10 percentage points, from 16.6% in 2009 to 6.3% last year in a time when overall car registrations have shown positive growth.

SUVs are continuing to gain ground, with most featuring 5-door body-types, this is having a negative impact on traditional segments, with the market abandoning less practical body-types. Roughly half of the 3-door small cars currently available in the market correspond to unique body-types without a 5-door option available – for example the Fiat 500, Smart Fortwo, Opel Adam, DS 3, VW Beetle, Ford Ka, Alfa Romeo Mito or VW Scirocco.

The declining sales of the category is resulting in fewer choices for consumers, with many 3-door versions of the popular B-Segment cars no longer available, such as the Clio, Punto, Micra and Ypsilon which are all only available in 5-door versions, meanwhile the new generation Ibiza, Polo and Swift will eliminate the 3-door versions from their catalogues.

In the C-Segment, the situation is even more dramatic as car makers have eliminated the 3-door versions of the Astra, Focus, 308, Megane, Auris, C4, i30 and the Civic (in Europe).

The unavailability of the Polo 3-door is one more step towards the end of a body-type that was a synonym for ‘cool’ style, that is no longer valid in a market full of more practical, rational consumers. A strong trend like this can even impact a strong player like Volkswagen so is one to watch.