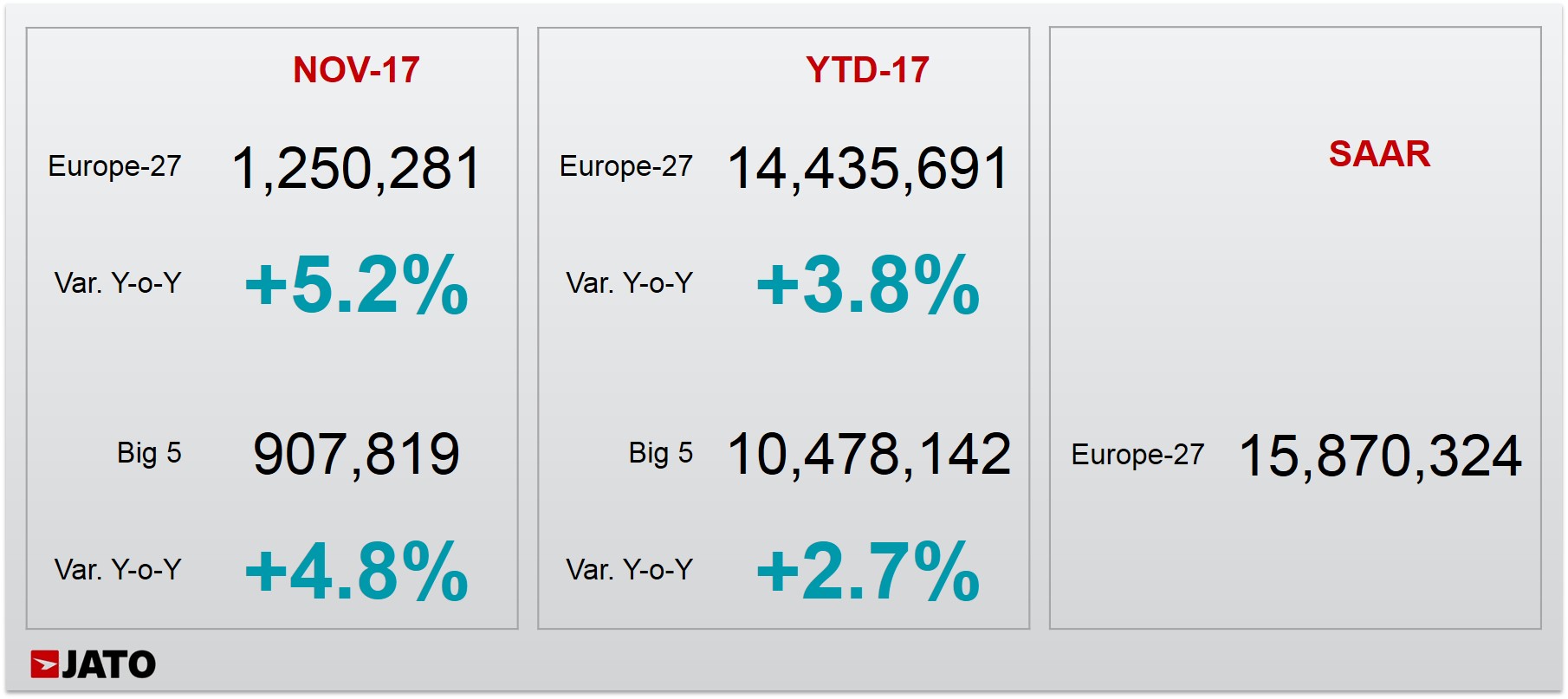

- European car registrations increased by 5.2%, with a total of 1,250,281 registrations in November 2017

- SUVs recorded a 31.9% share of the market, an increase of 4.3 percentage points in just 12 months

- The VW Golf maintained its top spot, but the Peugeot 3008 SUV gained the most market share

The European car industry held firm in November 2017, with new registrations totalling 1,250,281, an increase of 5.2% when compared to November 2016. France, Spain and Germany, along with mid-sized markets including the Netherlands and Austria, experienced the biggest increases in volume for the month, off-setting a decline in the UK market where registrations were down 11.2%. Despite a turbulent 2017 for the industry as a whole, which has faced threats from the diesel crisis, new emissions targets and Brexit, results for the first eleven months of the year show an overall increase in registrations of 3.8%, with 14.43 million units registered over the period.

Growth was driven by the ever-increasing demand for SUVs and registrations in the segment grew by 21.6% to almost 400,000 units. SUVs now make up 31.9% of the market, an increase of 4.3 percentage points from a market share of 27.6% during the same period last year.

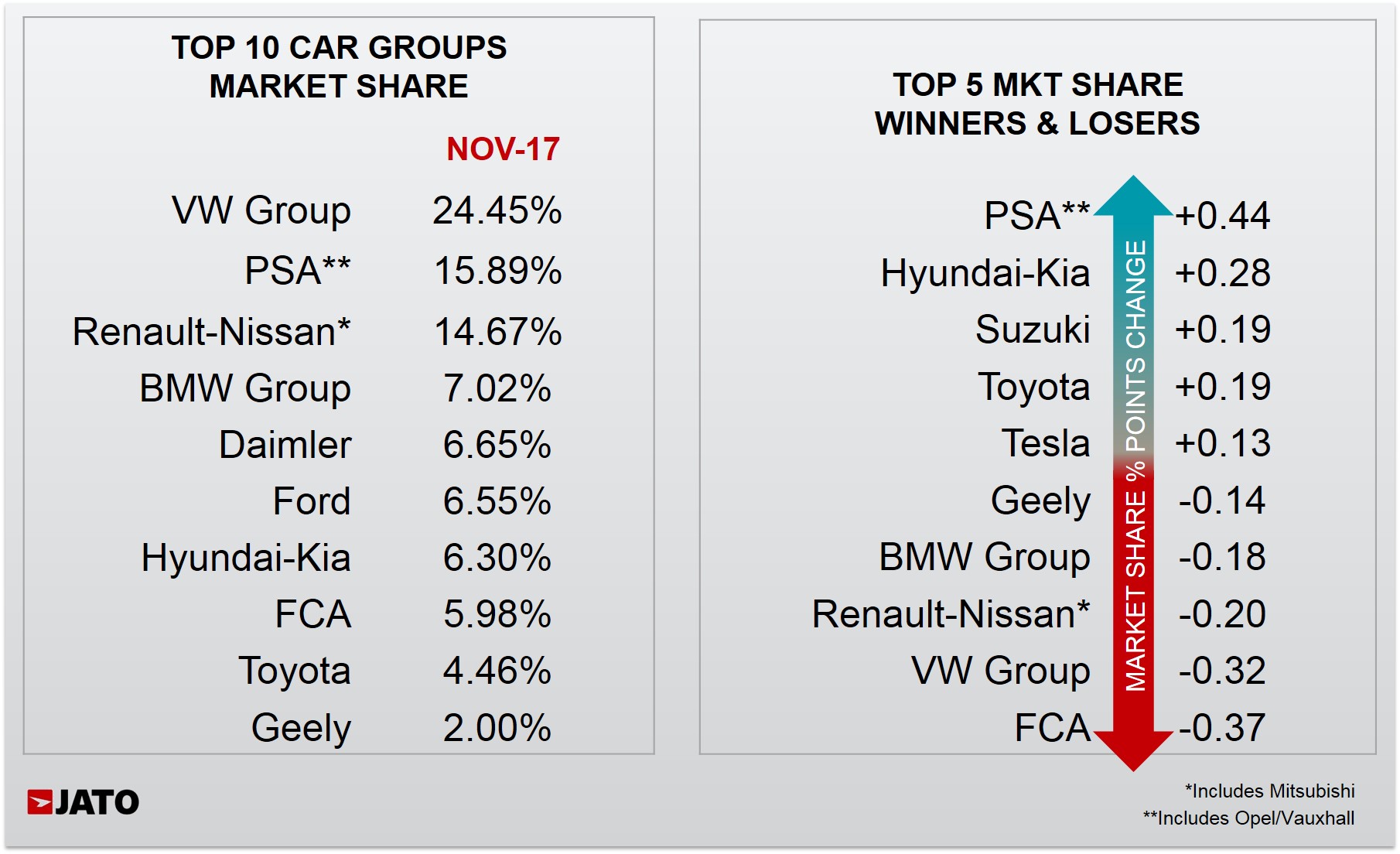

The SUV segment was bolstered by increased demand for small (B-SUV), compact (C-SUV) and midsize (D-SUV) SUVs, which increased volumes by 25.5%, 16.6% and 41% respectively. Latvia and Estonia held their positions as the European markets where SUVs are most popular, with market shares of 44.1% and 39.5% respectively. Significant market share increases for SUVs in Denmark, Poland and Norway contributed to the segment’s increased volume for November. Despite its dominant position in the segment, with a share of 19.8% of the SUV market, Renault-Nissan was unable to take advantage of this increased demand, with registrations of its SUV vehicles only increasing by 2.4% for November. In contrast, PSA, due to the strong performance of its new Peugeot, Opel/Vauxhall and Citroen SUVs, saw its SUV registrations grow by 70.2% in November – meaning it outsold VW Group in the segment.

“Despite the upheaval it faces with new emissions targets, Brexit, and the diesel crisis, increasing demand for SUVs has allowed the automotive industry to continue to grow in Europe. Looking ahead to the future, it is clear that manufacturers will increasingly see the SUV segment as a means of growth in a tough market, and as a consequence, SUVs will take market share away from more traditional segments. Already we have seen the effects of this on MPVs, which recorded a market share of just 7% in November 2017, thanks to a fall in volume of 11.3% to 87,400 units. This has been caused by the discontinuation of vehicles such as the Citroen C3 Picasso, Opel/Vauxhall Meriva and Nissan Note, which couldn’t compete with their B-SUV counterparts,” commented Felipe Munoz, Global Automotive Analyst at JATO Dynamics.

VW group kept its lead with 24.5% market share, a decrease of 0.3 percentage points on last year. PSA came second after experiencing the third highest increase in volume for the month. FCA fell due to a decrease in registrations in its home market of Italy.

The VW Golf comfortably held on to its number one position. The Peugeot 3008 SUV gained the most market share for the month, followed by three other SUVs: the Opel/Vauxhall Crossland X, Peugeot 5008 and Skoda Kodiaq.

Click below to see full tables