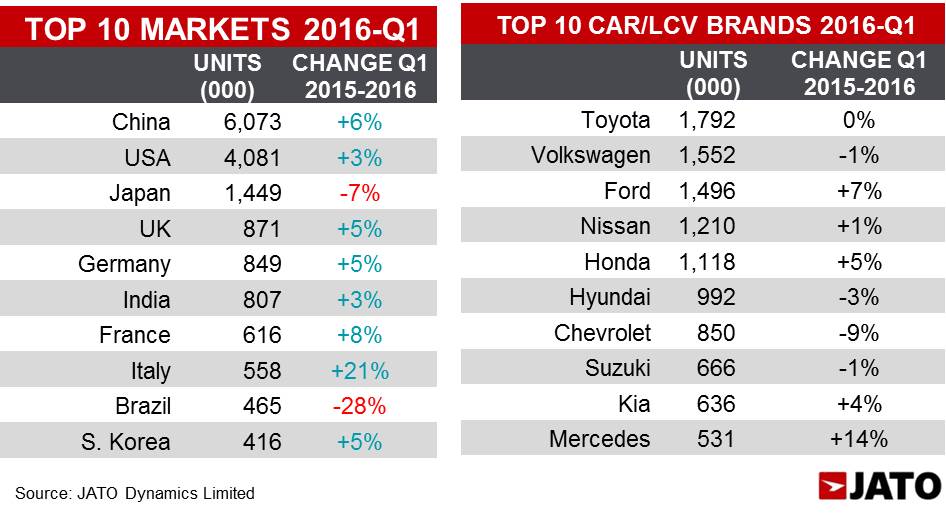

- Overall, 20.44 million units were sold across all segments in Q1 2016, largely driven by growth in the Chinese and European markets

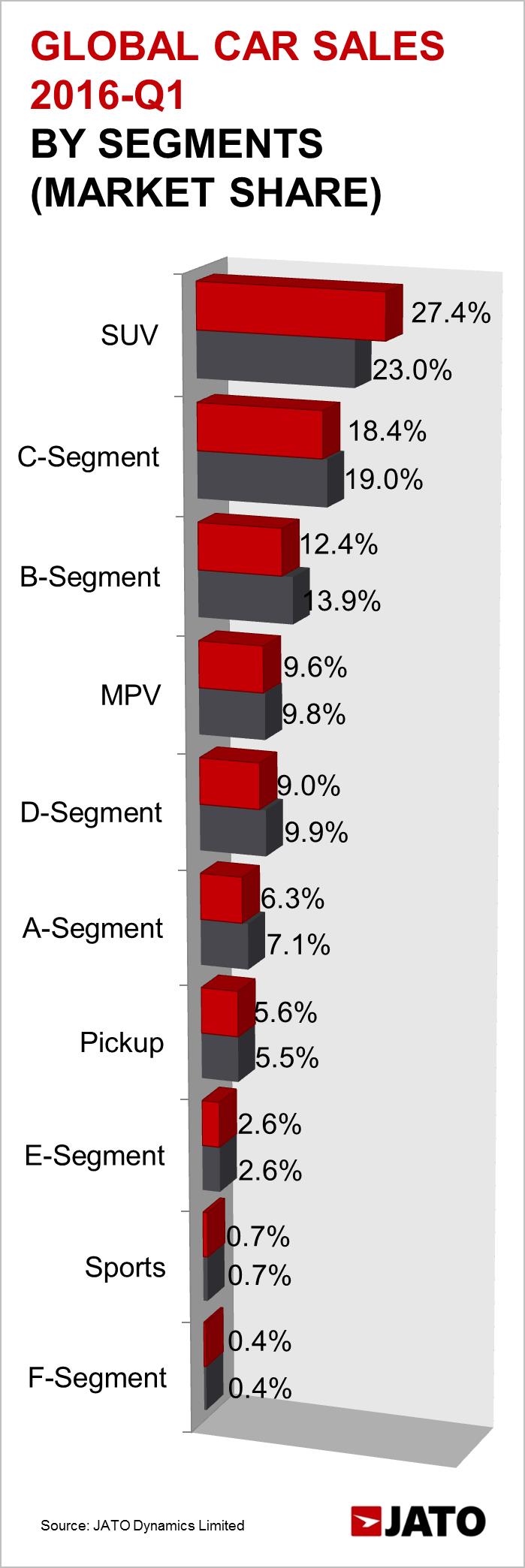

- The SUV boom continued, with seven of the eight regions analysed posting double digit growth

- Ford, Honda and Mercedes posted the strongest growth, largely driven by their SUVs

- Volkswagen posted a 1% decline on the same period in 2015

In Q1 2016, 558,700 more units (LCVs and passenger cars) were sold compared with the same period in 2015 according to a report released today by JATO Dynamics. Global car sales totalled 20.44 million units, a 2.8% increase on the same period in 2015. Significantly, the market’s biggest brands posted declines, with Volkswagen declining by 1%, Hyundai by 3% and Chevrolet by 9%. Ford, Honda and Mercedes posted the biggest increases amongst the top 10 at 7%, 5% and 14% respectively.

In terms of models, the Toyota Corolla reported a 4.8% gain in Q1 2016 which saw it move up the ranking to become the best-selling vehicle for this period, knocking the Wuling Hongguang from the top spot.

The popularity of SUVs in China has been an ongoing source of growth, and the trend continued last quarter, with the country accounting for 36% of total sales in Q1 2016. Sales of SUVs in Europe (including Russia and Turkey) gave the overall market a boost with 20% growth and 1.11 million units sold.

SUVs continued to dominate across much of the rest of the world in Q1 2016, with the category increasing sales by 23% compared with the same period last year and five vehicles from the category entering the top 10 best-selling car ranking – these were the Nissan X-Trail, Honda HR-V, Toyota RAV4, Honda CR-V and Ford Escape. All regions included in the report posted positive growth for SUVs, with all except for Japan-Korea posting double digit growth. As a result of the growth, the market share of the SUV segment jumped to 27.4% compared to 23.0% in the same period of 2015. The growth in the SUV segment was offset by slower rises amongst the traditional segment leaders; Renault-Nissan kept the lead in the SUV category but its growth was half the average for the segment. The SUV category has room for improvement in India and South America as the segment only accounted for 15% and 14% of the country’s respective total volumes.

SUV growth also drove premium car volumes, with 2.15 million units sold, 833,300 of which were SUVs. Overall the premium category saw a dramatic 9% gain on the same period last year. The growth saw the category go from a 10.8% market share in Q1 2015 to 11.4% in Q1 2016. Europe was the strongest market for premiums, accounting for 43% of the global total. North America was second, losing ground at a 24% share, and closely followed by China-Taiwan with a 23% share of global sales.

Felipe Munoz, Global Automotive Analyst at JATO, concluded: “Q1 2016 saw dramatic changes as the SUV category increased its market dominance. The whole world wants a SUV, and this shift is evident in the brand ranking, as those that focused on this segment, were the brands that posted the largest gains.”