European OEMs have experienced several challenges this year. Alongside the hugely disruptive effects of Covid-19, manufacturers are now facing the impending CO2 target deadline presented by the European Commission.

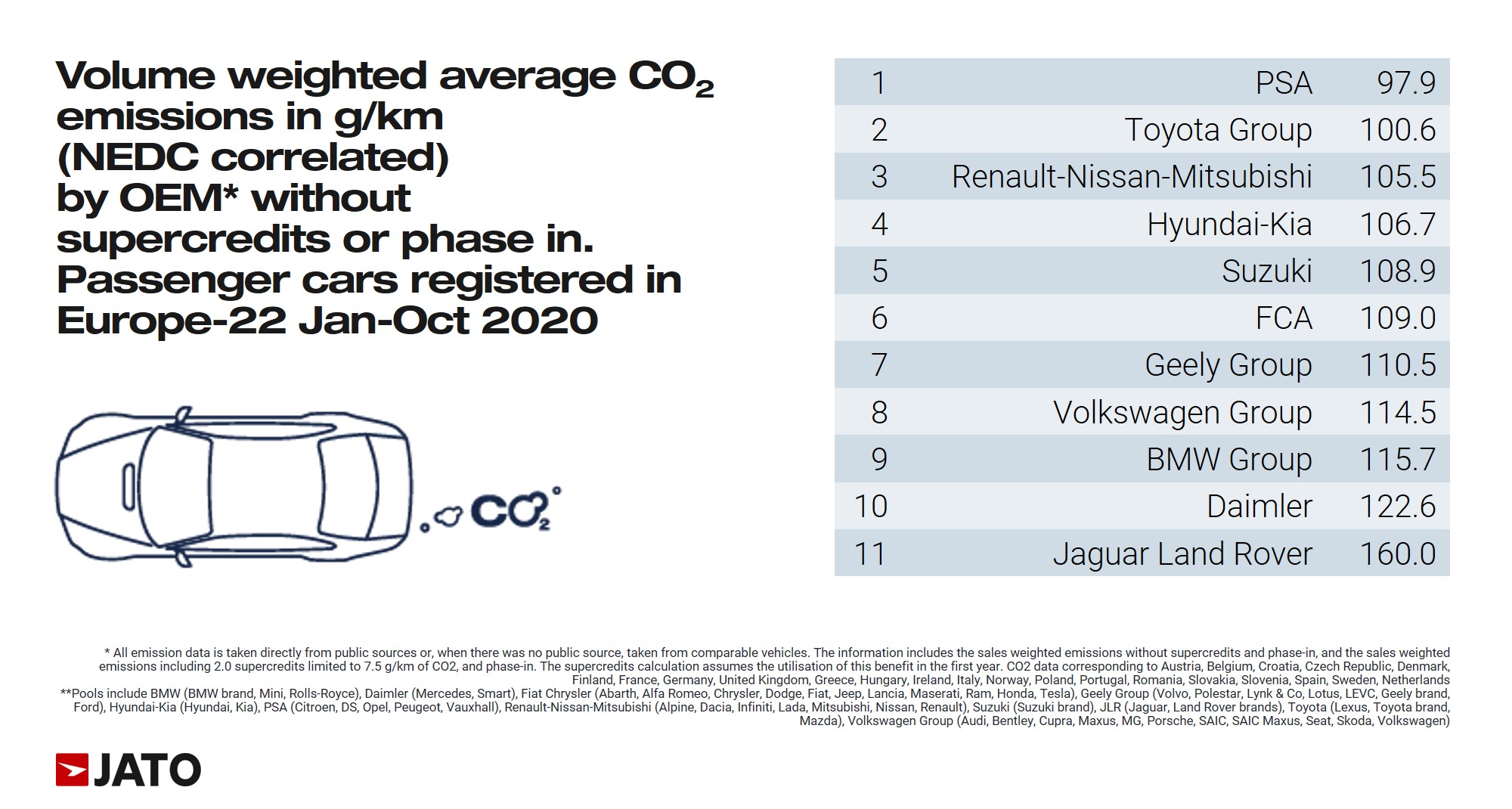

According to our data*, the results for January-October 2020 revealed that PSA recorded the lowest sales weighted CO2 emissions across all benchmarks.

According to our data*, the results for January-October 2020 revealed that PSA recorded the lowest sales weighted CO2 emissions across all benchmarks.

The European Commission’s legislation states that for each gram that’s over the CO2 target, manufacturers will face a fine of €95 per car registered. As a result of this policy, many brands have taken to discontinuing some of their slow-selling models that also heavily contribute to their CO2 averages.

The CO2 target deadline has also led to the acceleration of OEMs’ electrification plans. The “super-credit” system presents manufacturers with additional incentives for marketing zero and low-emission vehicles – specifically those that emit less than 50 g/km. And, through the “super credit system” when calculating a manufacturer’s average emissions levels, these cars also count as two vehicles.

The CO2 target deadline has also led to the acceleration of OEMs’ electrification plans. The “super-credit” system presents manufacturers with additional incentives for marketing zero and low-emission vehicles – specifically those that emit less than 50 g/km. And, through the “super credit system” when calculating a manufacturer’s average emissions levels, these cars also count as two vehicles.

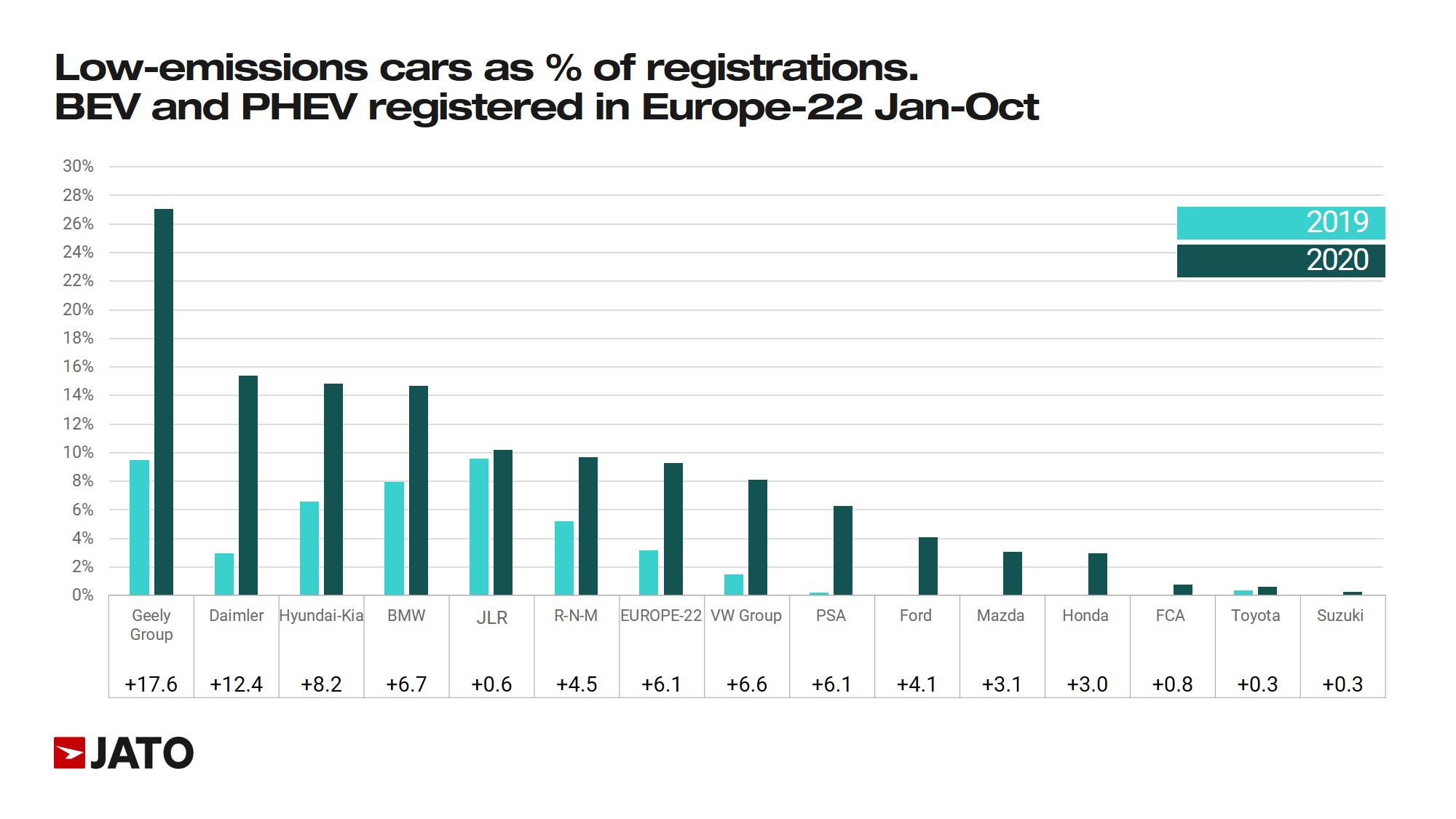

According to our data, the super-credit policy has been a driver behind the outstanding growth seen in EV registrations this year. Registrations of low-emissions cars** increased by 113% through October to 875,000 units from 411,700 units in 2019, for 22 markets across Europe. The market share of low emissions cars jumped from 3.2% (January – October 2019), to 9.3% year-on-year. This increase coincides with the double-digit decline in demand seen for gasoline and diesel cars.

Low-emissions vehicles market surge continues

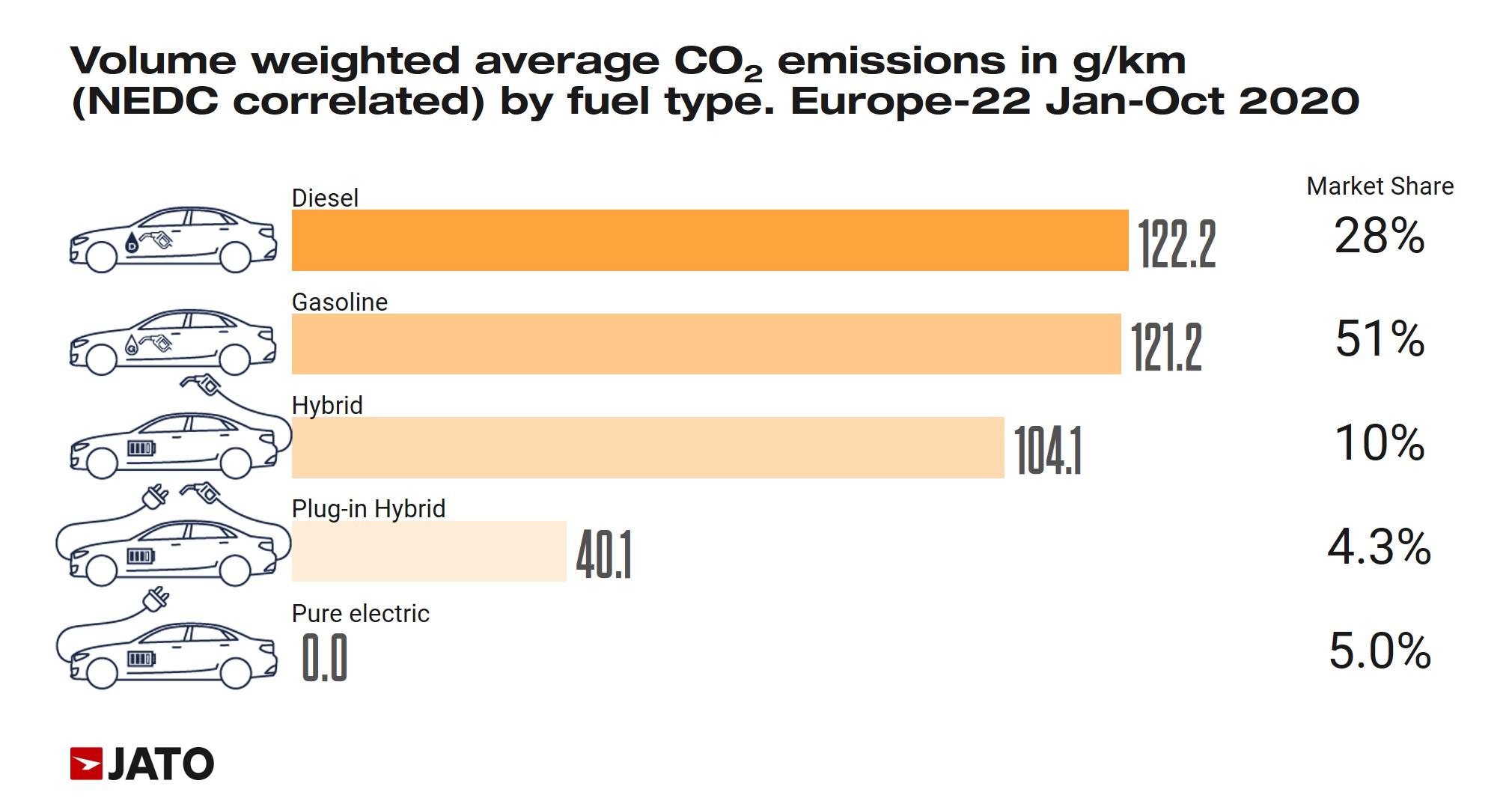

As the low carbon agenda is driven forward by European legislation, low emissions vehicles registrations continue to soar. In fact, when measured against the current super-credits legislation, pure electric cars, fuel-cells powered cars, and plug-in hybrid electric cars were the only vehicles to post averages that sit within the 50 g/km limit.

The same cannot be said for pure ICE (diesel and petrol) and hybrid vehicles. In January-October 2020, these cars posted averages above 100 g/km.

PSA achieved lowest emissions

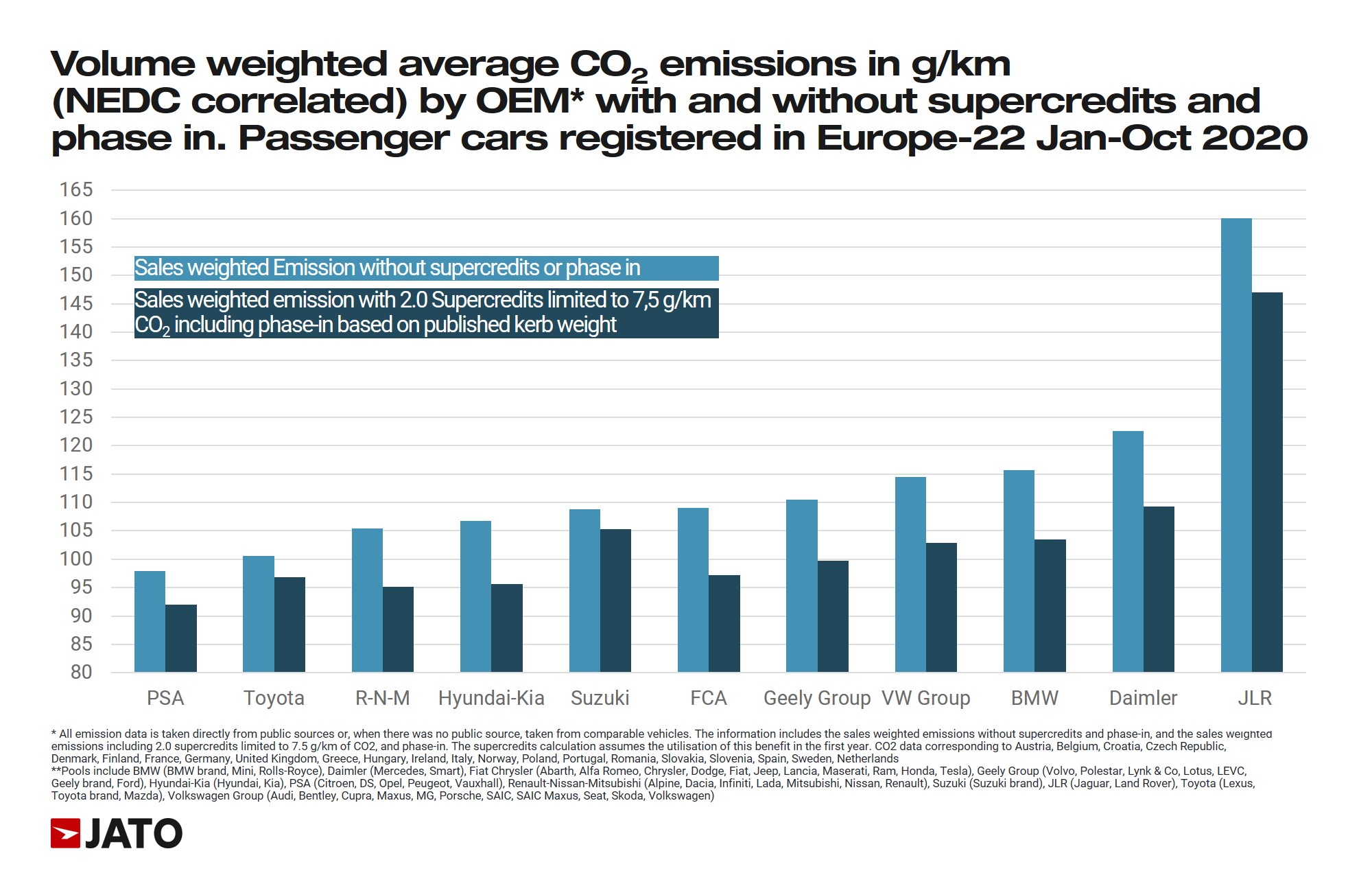

Between January and October 2020, PSA registered sales-weighted emissions of 97.9 g/km. This was the best result among 11 different pools** – achieved without supercredits or phase-in benefits.

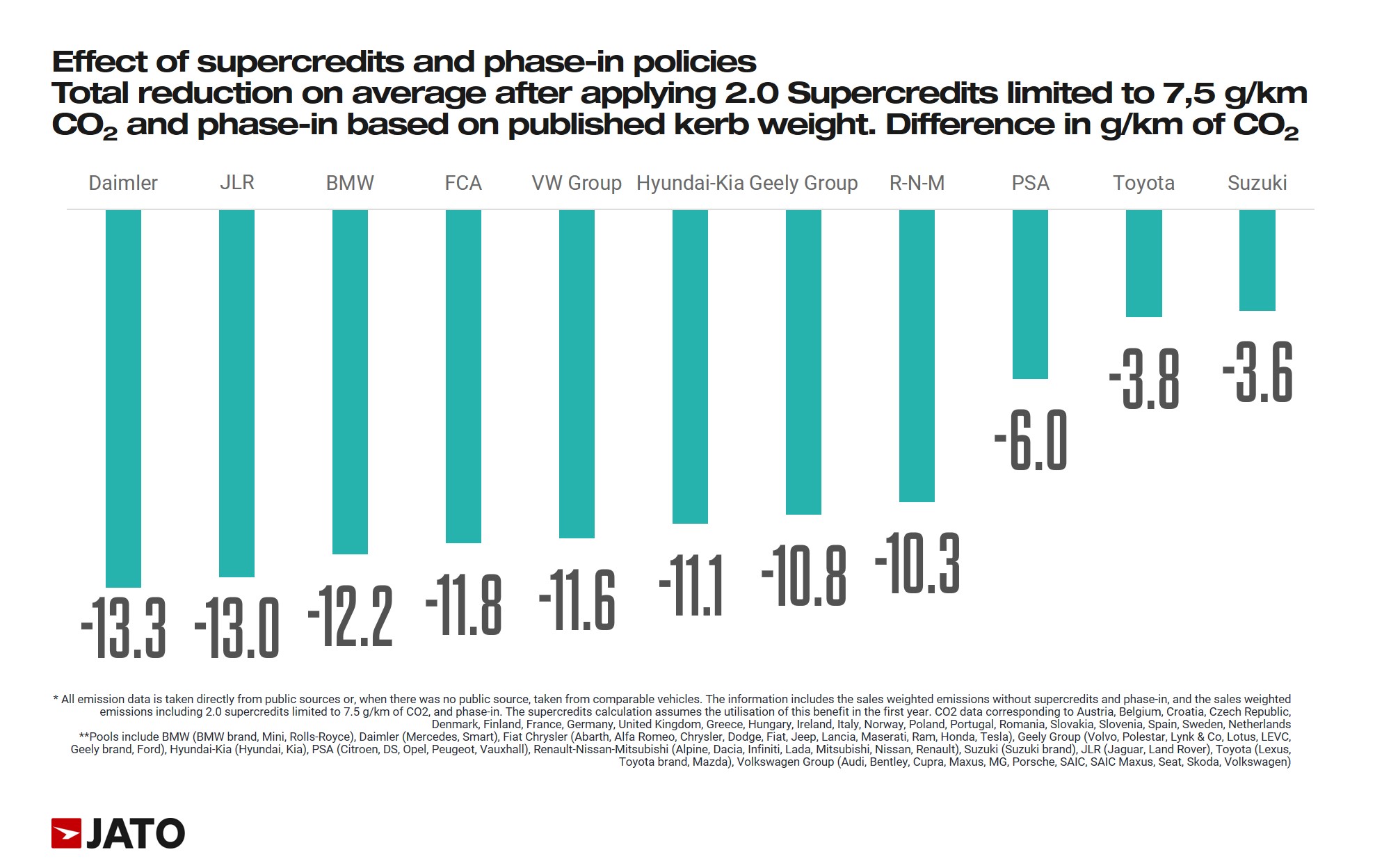

In January-October, the use of supercredits and phase-in benefits reduced PSA’s average CO2 emissions levels to 91.9 g/km. This reduction of 6 grams comes as a result of the increased demand seen for small cars, and their recent focus on low emissions vehicles. The city-cars, subcompacts and small SUVs accounted for 57% of PSA’s volume through October, while registrations of its plug-in hybrid and pure electric cars totalled 88,800 in the first ten months of this year.

DS was the second brand with the lowest average CO2 emissions in Jan-Oct 2020, only behind MG and the four zero-emissions brands, Tesla, Maxus, Polestar and Smart.

About JATO’s C02 emissions data

*All emission data is taken directly from public sources or, when there was no public source, taken from comparable vehicles. The information includes the sales weighted emissions without supercredits and phase-in, and the sales weighted emissions including 2.0 supercredits limited to 7.5 g/km of CO2, and phase-in. The supercredits calculation assumes the utilisation of this benefit in the first year. CO2 data corresponding to Austria, Belgium, Croatia, Czech Republic, Denmark, Finland, France, Germany, United Kingdom, Greece, Hungary, Ireland, Italy, Norway, Poland, Portugal, Romania, Slovakia, Slovenia, Spain, Sweden, Netherlands.

** BEV + PHEV + FCEV

*** Pools include BMW (BMW brand, Mini, Rolls-Royce), Daimler (Mercedes, Smart), Fiat Chrysler (Abarth, Alfa Romeo, Chrysler, Dodge, Fiat, Jeep, Lancia, Maserati, Ram, Honda, Tesla), Geely Group (Volvo, Polestar, Lynk & Co, Lotus, LEVC, Geely brand, Ford), Hyundai-Kia (Hyundai, Kia), PSA (Citroen, DS, Opel, Peugeot, Vauxhall), Renault-Nissan-Mitsubishi (Alpine, Dacia, Infiniti, Lada, Mitsubishi, Nissan, Renault), Suzuki (Suzuki brand), JLR (Jaguar, Land Rover), Toyota (Lexus, Toyota brand, Mazda), Volkswagen Group (Audi, Bentley, Cupra, Maxus, MG, Porsche, SAIC, SAIC Maxus, Seat, Skoda, Volkswagen).