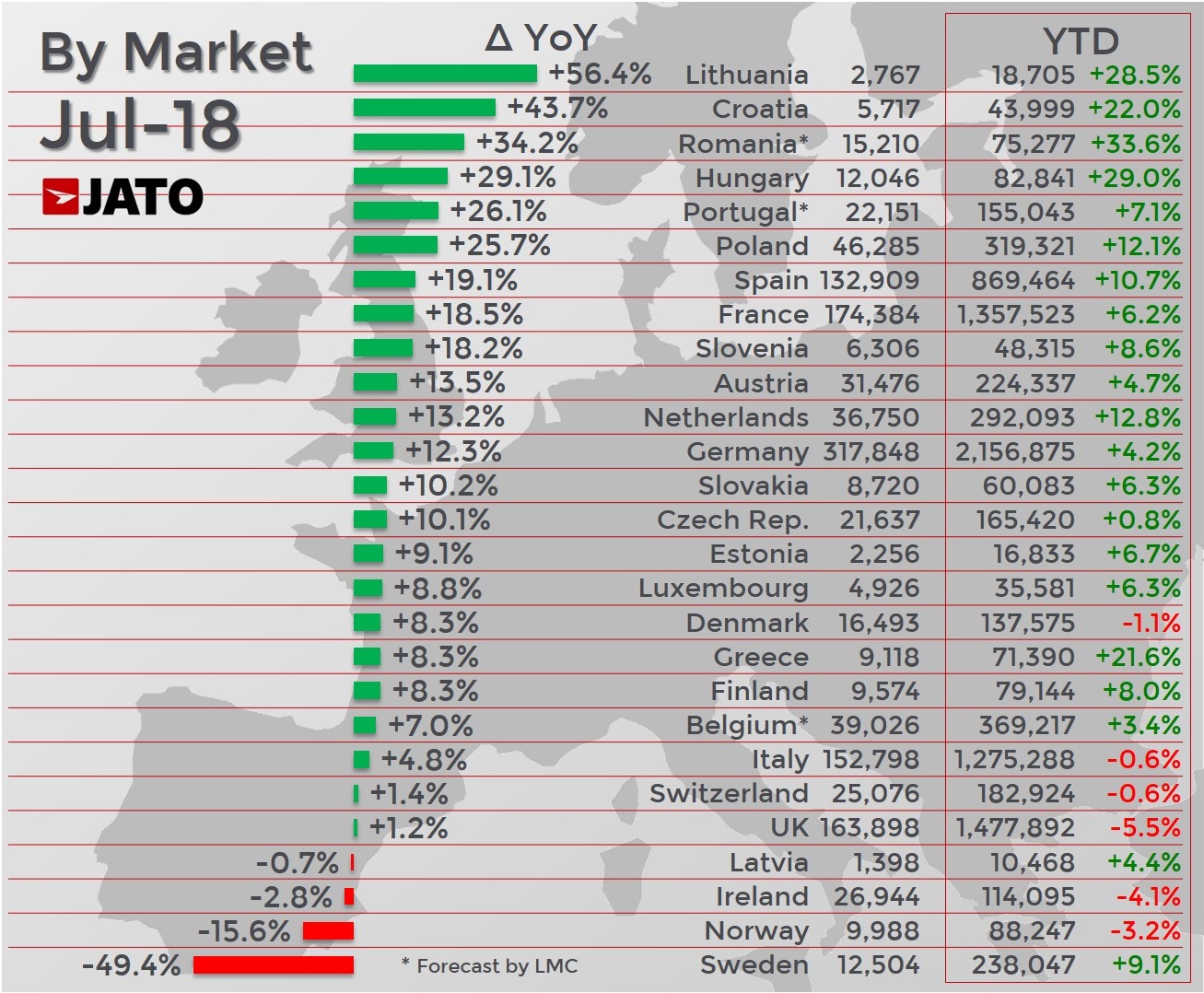

- A total of 1.31 million cars were registered in July, a year on year increase of 10.0%

- The overall market was boosted by strong results in Spain and France

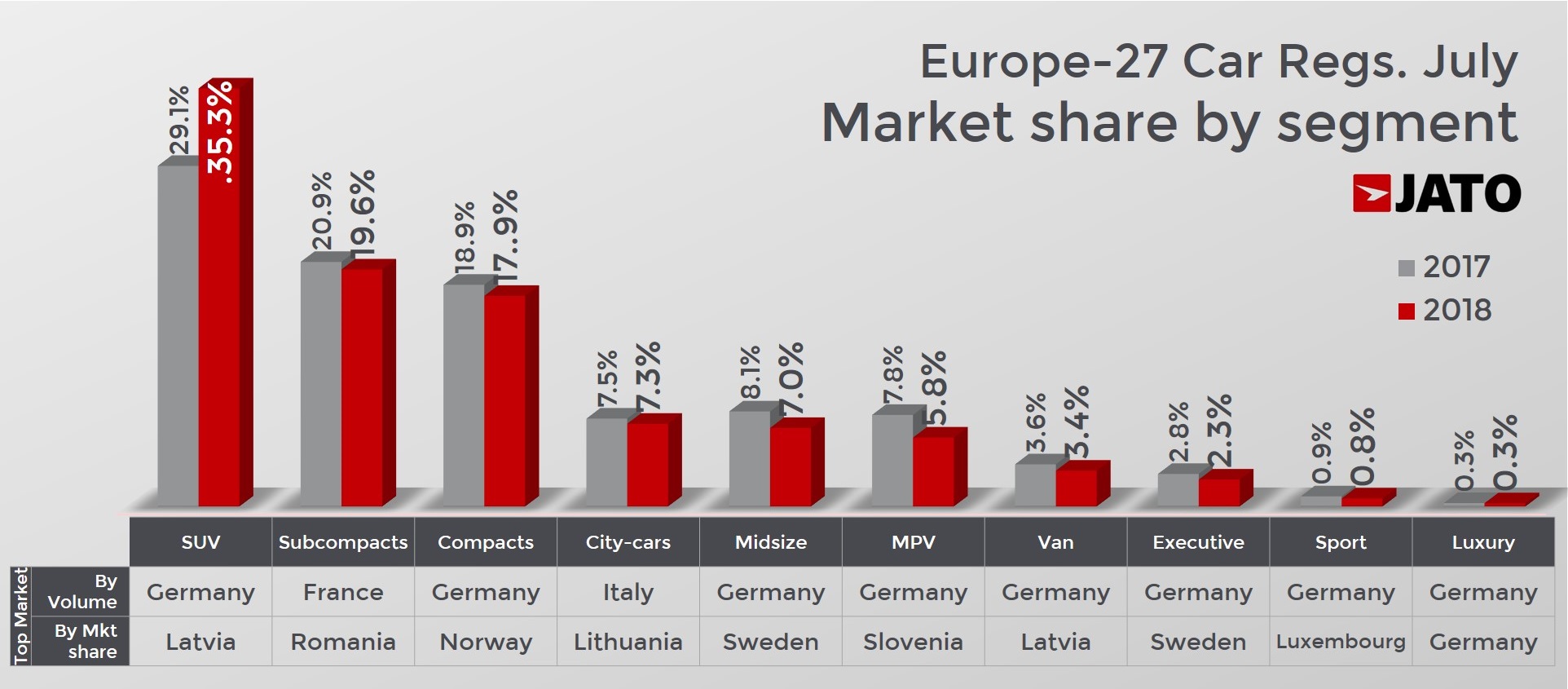

- SUV demand continued to grow, as the segment accounted for 35.3% of total registrations – a new record

The European car market continued its strong performance in July, as a total of 1.31 million cars were registered, the highest monthly volume since July 2009 when 1.29m million cars were registered. The market was boosted by increased demand in Spain and France, as well as double-digit growth in midsize markets like the Netherlands, Austria and Poland. The results were also boosted by an extra selling day in the month compared to July 2017, and the upcoming deadline to register cars under the existing NEDC emissions regulations may also have had an impact by accelerating the purchase process.

“The results from July are certainly positive and a clear sign that the market is recovering well, despite the current challenges it faces over diesel and CO2 regulations. Although these results are encouraging, part of the growth could potentially be explained by more consumers and dealers buying cars before the WLTP test process is extended to cover all new car registrations on 1st September. It will be interesting to see how the market performs in August, and whether this confirms the theory,” comments Felipe Munoz, JATO’s Global Analyst.

The SUV segment once again benefited from the increase in consumer demand. As has been the case for many months, demand for SUVs continued to grow throughout July, as their volume increased by 34% to 461,900 units. This means they accounted for 35.3% of total registrations across Europe for the month – a new record.

A large part of the growth can be explained by the increasing popularity of small SUVs, which accounted for 37% of total SUV registrations. Volume for small SUVs increased by 50%, rising from 113,400 units in July 2017 to 169,800 units last month. With the exceptions of Suzuki, Mazda and Mahindra, all car groups posted an increase in the small SUV sub-segment. Renault-Nissan secured a 25% share of the market, followed by PSA and VW Group which accounted for 23% and 19% of the market respectively.

A large part of the growth can be explained by the increasing popularity of small SUVs, which accounted for 37% of total SUV registrations. Volume for small SUVs increased by 50%, rising from 113,400 units in July 2017 to 169,800 units last month. With the exceptions of Suzuki, Mazda and Mahindra, all car groups posted an increase in the small SUV sub-segment. Renault-Nissan secured a 25% share of the market, followed by PSA and VW Group which accounted for 23% and 19% of the market respectively.

The SUV market continued to be dominated by compact SUVs, which recorded 198,300 registrations, a volume increase of 34%. VW Group led the sub-segment with a 22% market share, followed by Renault-Nissan with 17% and Hyundai-Kia with 13%. VW Group also led in the midsize SUV sub-segment, whose registrations totalled 73,000 units, up by 15%.

Only large SUVs didn’t grow, with volume stable at 20,900 units. Meanwhile, demand for subcompacts, compacts and city-cars also grew but at a slower pace than the overall market. As a result, all segments lost market share with the exception of SUVs.

Only large SUVs didn’t grow, with volume stable at 20,900 units. Meanwhile, demand for subcompacts, compacts and city-cars also grew but at a slower pace than the overall market. As a result, all segments lost market share with the exception of SUVs.

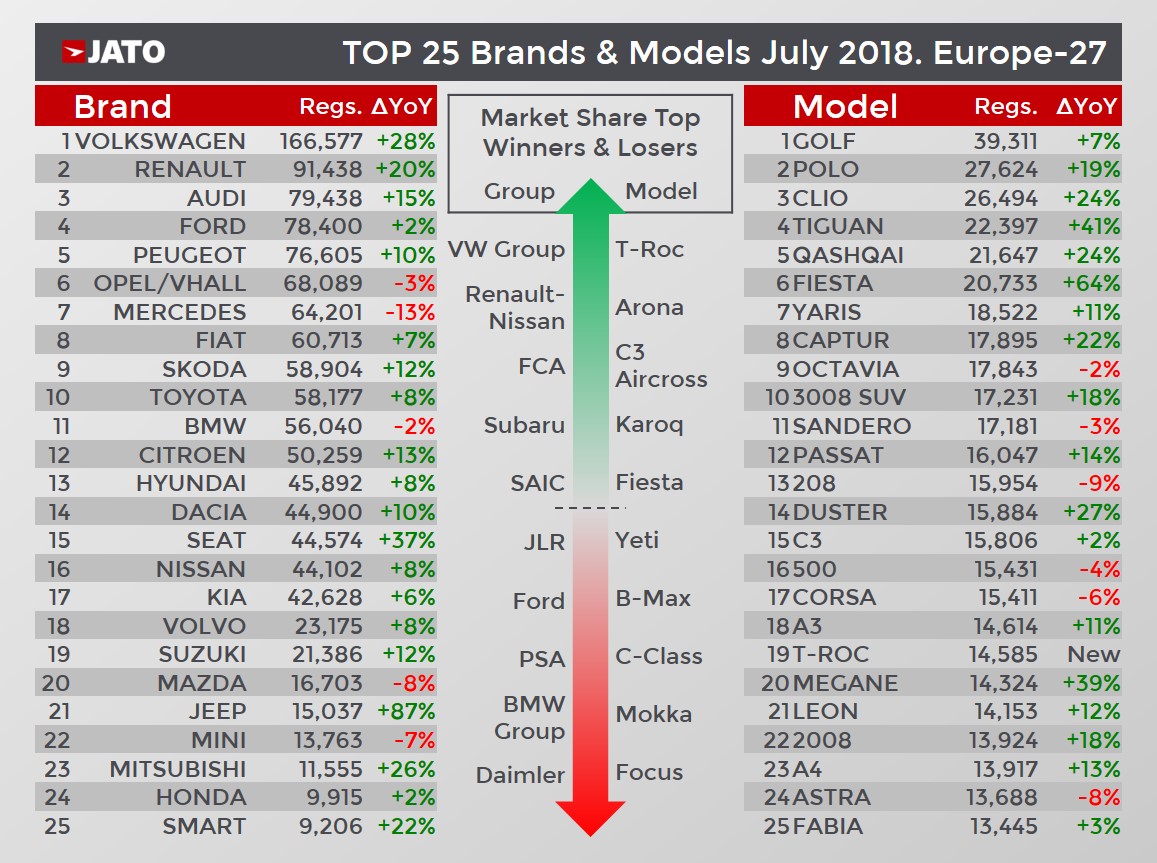

VW Group was once again the top-selling car maker in Europe in July and it also posted the highest market share gain. This was largely due to its latest SUV launches being a success with consumers, as the T-Roc hit the top 25 model ranking, and the Karoq and Arona also gained significant market share. The results can also be attributed to double-digit growth across the VW, Skoda and Seat brands.

Renault-Nissan also performed well in July, with registrations up by 14% to 193,100 units. With the exception of Infiniti, all of its brands recorded increases. PSA was slightly ahead with 6,100 more registrations, but its volume was only up 6% as increases at Peugeot, Citroën and DS were offset by a 3% decline at Opel/Vauxhall.

Other brands which recorded significant increases during the month included Suzuki, Jeep, Mitsubishi, Smart, Alfa Romeo, Porsche, Jaguar and Subaru. Conversely, Mazda, Mini, Land Rover, and Mercedes all posted declines.

Other brands which recorded significant increases during the month included Suzuki, Jeep, Mitsubishi, Smart, Alfa Romeo, Porsche, Jaguar and Subaru. Conversely, Mazda, Mini, Land Rover, and Mercedes all posted declines.

The Volkswagen Golf maintained its place as the best-selling car in Europe, as did the Volkswagen Tiguan as the best-selling SUV. There were no significant changes in the top 25, except for the entrance of the Volkswagen T-Roc, which became the 19th best-selling car in Europe in July. It was only outsold by the Renault Captur and the Dacia Duster in the small SUV segment.

Among the latest launches there were some significant performers; the Citroën C3 Aircross recorded 9,766 units (40th place), Skoda Karoq recorded 7,703 units (53rd place), Seat Arona recorded 10,106 units (37th), and Opel/Vauxhall Grandland recorded 6,734 units (69th). The Jeep Compass registered 7,290 units, the Volvo XC40 registered 5,795 units, and Hyundai registered 5,694 units of the Kona.

More details and rankings are available on the JATO Blog