In the race for automotive electrification, China has set the bar high. Recognising that electric vehicles would offer a clear route to becoming a major player in the global automotive market, Chinese OEMs moved quickly to secure a stronghold in the EV market.

The Covid-19 crisis has raised concerns that the economic hardship could lead governments to relax fuel efficiency standards to lower the pressure on struggling automakers or reduce support measures for electric cars to free up funds for use elsewhere. That has not happened so far. China announced it would extend the purchase subsidies that it had originally planned to discontinue this year until 2022 – albeit at a slightly reduced rate.

There is little doubt that the future of the growing EV market is on the minds of the world’s largest OEMs. China has already begun owning it, but with a cooling of the market in China as the government pulls back on subsidies, the race is far from over.

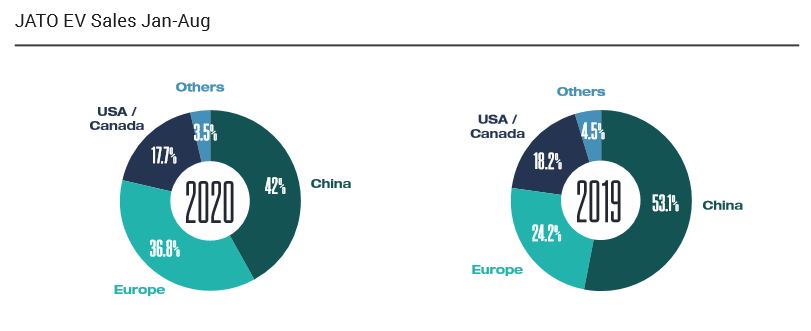

Rapidly shifting regional dynamics means other markets led by Europe now have an opening to lead global growth in electric-car sales for the first time, as governments across the region offer consumers sweeteners toward the purchase of new vehicles. Momentum is building in a market that’s already the world’s second biggest – well behind China but significantly ahead of North America. In fact, the European market is growing at such a pace that it is looking increasingly likely that Europe will outsell China on EVs in the near future.

China’s regulation, incentivisation and consumer demand

Incentivisation and heavy government intervention have played a crucial role in helping the Chinese EV market to flourish. From investments into start-up businesses and consumer subsidies, right through to building a robust charging infrastructure network, this heavy interventionist approach has helped to supercharge consumer and business confidence and has fuelled EV uptake at pace.

However, with government subsidies due to end in 2022, consumer demand for EVs has begun to slow down for the first time and is likely to drop further once subsidies are phased out. But despite this, for now the EV market in China continues to grow and with many Chinese OEMs looking to target other regions to continue expansion, it remains to be seen whether their success is dependent on government intervention alone.

Since 2016, China has been the fastest and largest growing market for electric vehicles in the world. A number of factors have driven its rise to precedence, but arguably, none more than an incentivisation policy mix which has effectively produced the world’s largest EV market in just a decade.

With the Chinese government quickly recognising EVs as a golden opportunity to become a global leader on the automotive stage, manufacturers eagerly joined the race for electrification – taking centre stage in the EV market, long before their competitors in the West.

At a national level, the Government recognised the potential of EVs to become a pillar of economic growth and as such, Chinese businesses and consumers alike were gifted huge investments and subsidies. Whilst China isn’t alone when it comes to subsidy provision for automakers, the fundamental difference here was that imported vehicles were never made eligible for subsidies and were subject to import tariffs.

This unwavering commitment to cultivating high quality domestic manufacturers and establishing a domestic supply chain ecosystem saw the Government backing everything from homegrown EV start-ups and parts manufacturing, right through to building a robust charging infrastructure network – all in the name of supercharging confidence and demand.

In many ways, this approach has been hugely successful.

This is epitomised by the fact that Chinese OEMs are now turning their attention to overseas expansion, and western manufacturers looking to Asia for transferable trends in automotive technology and connectivity.

Despite this impressive growth, over the last year there has been a stabilisation in the Chinese EV market, and China remains some distance from meeting its ambitious target for 25% of total new vehicles to be New Energy Vehicles (NEVs) by 2025.

This slowdown comes as a result of a subsidy reduction enforced by the government over the last few years. As Europe’s EV market has continued to grow from strength to strength, this stagnation prompts the question – is China’s success solely down to heavy government intervention?

Only time will tell just how much of an influence China’s regulation and incentivisation has had on their longer-term success, but for now the Chinese government seems committed to their continued success in the EV market in China. Having announced the extension of tax exemptions and subsidies and issuing new credit schemes for NEVs until 2023, it is more than likely that the EV market in China will only continue to grow.

What can the world learn from China?

There are two defining factors which catalysed China’s rapid rise to EV global dominance in such a short space of time, the first is vast capital investment with an estimated $50bn pumped into the industry – combined with a highly interventionist, centralised strategy to not only support manufacturing, but also the rollout of a nationwide infrastructure programme to complement uptake.

At the very heart of this plan, however, was a deep-seated commitment – that today’s dominance of the electric vehicle market will lead to China’s global automobile supremacy tomorrow.

Results orientated intervention

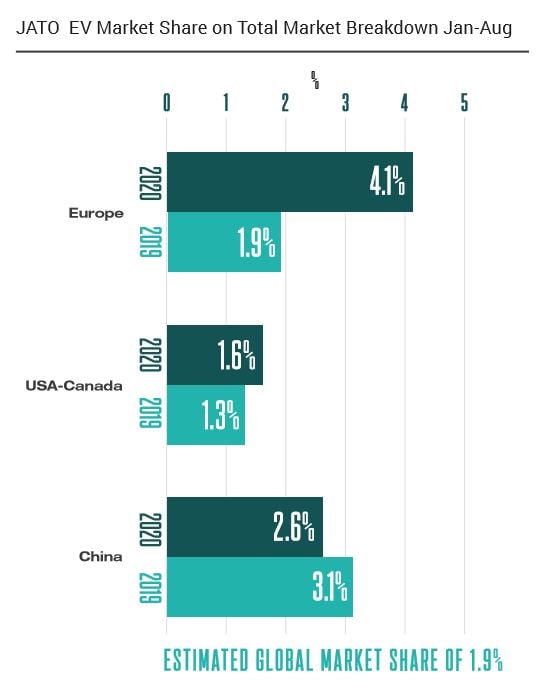

It is ultimately heavy Government intervention that set the tone for China’s EV market dominance. Fast forward a decade and China’s new electric vehicle market has become the largest in the world. And the results speak for themselves – in 2018, according to JATO data more than 700,000 vehicles were sold in China – the highest annual result.

A relentless approach was applied to not only encourage the uptake of EVs but to deter consumers from petrol and diesel cars. One example of this is in Shanghai and how license plates are granted; it costs $13,000 for a vehicle with a combustion engine, whereas it is free of charge for an EV – thereby creating a huge economic incentive and making the use of electric vehicles a no brainer.

It is clear that when examining China’s approach to incentivisation and regulation, that China set out to win, and would stop at nothing to achieve its ambitions. When compared with government interventions in other global markets, it is apparent that a lighter touch approach is simply not as successful – as can be seen in the EU or US. For example, China has offered consumers large discounts to drive uptake at scale and pace, whereas the US has instead granted OEMs limited subsidies on their vehicles sold which will inevitably result in slow progress.

The simple fact remains that as long as EVs remain at a premium price point, consumers will have little incentive to make the switch, meaning that Western OEMs must consider new and innovative ways of making price points more affordable.

Harnessing the power of centralised planning

A centrally planned economy was also integral to China’s success in driving EV adoption, to enable an effective infrastructure implementation strategy which is crucial to supporting adoption. To put things into perspective, according to the IEA the number of public slow and fast charging spots reached 862,118 globally, with China, the world’s largest car market, taking a 60% share (Global EV Outlook 2020).

Whilst a number of governments, including the UK, have announced that new petrol and diesel cars could stop being sold as early as 2030, there is still no clear plan to back up these bold ambitions – which ultimately has a knock-on effect when it comes to consumer confidence. What governments in underdeveloped EV markets now need is a more centralised plan to catalyse growth and create an optimal environment to build consumer confidence by making adoption as simple as possible.

Putting EV Affordability at the heart of production

China has also been able to grow very quickly due to an emphasis on cheap production. Where the EU decided to push luxury EVs, China has instead focused on affordable models and as a result, found success in higher sales and strong consumer uptake – catalysing the industry to grow at pace. China has also pioneered the production and sales of electric SUVs, whilst Europe and the US have focused efforts on mid-sized vehicles.

With some exceptions, most of the EV market in Europe and the US tends to be focused on the upper segments.

JATO’s figures show that there is a significant price point gap between China, Europe and the US. The average retail price (excluding any kind of incentive) of EVs sold in Europe and the US in 2019 was 58% and 52% higher than in China, respectively. This is a huge difference that goes some way to explaining the EV penetration in each market.

Data as a game changer

Chinese OEMs have quickly understood how data is going to change the market because many view vehicles essentially as a mobile data platform. In line with China’s smartphone generation ethos, Chinese OEMs care less about our traditional automotive capabilities and more geared towards data and technology expertise. This is ultimately where OEMs will find value in automotive in the coming years.

The use of data by Chinese OEMs enables them to understand consumers at a granular level, and by extension optimise segmenting target customers. Applying robust data and analytics enables them to gain deeper insights into consumer preferences, which they can then utilise to develop a more robust model for predicting purchasing behaviour and by extension, driving sales.

Different consumers, different levels of success

Attitudes vary considerably, market by market – and this can be seen when comparing consumer behaviour across different markets. Case in point are the differences in behaviour between consumers in Europe and China. Attitudes vary significantly when it comes to electric vehicles, and this section considers how the ‘consumer factor’ has influenced the shape of each of these markets.

China’s Early Adopters

China continues to dominate the EV market – accounting for half of all vehicle sales – and although this is predominantly down to government regulation and intervention in China, the attitudes of Chinese consumers has also played a significant role.

The rise of technology in Chinese society has been staggering in the past decade – for example more than 25% of worldwide smartphone sales are now generated in the country.1

And this technological obsession extends beyond phones – Chinese consumers are tech savvy, early adopters and keen to be at the forefront of digital development.

It is therefore unsurprising that Chinese consumers are demanding more digital features when it comes to electric vehicles – and this has only increased up to the present day.2 Connectivity is key for Chinese consumers, for example a recent study found that a third of Chinese consumers believe it is

critical to have in-car connectivity (compared to 18% of consumers in Germany). The vast majority of Chinese consumers reported the need for in-car services, and half wanted seamless synchronisation between their phone applications and car services.

The connected nature of smartphones – which constantly require the sharing of data with and across apps – are so ingrained in daily life in China, that consumers are less concerned about sharing data than their European counterparts. As the Chinese are more relaxed with their data, businesses are afforded better insights into their customers’ perceptions, buying and search habits, and ultimately, their preferences. This is reflected in China’s production of EVs – for example, one of China’s latest best-selling EVs is the BYD Qin Pro,3 according to the China Passenger Car Association. The model features an intelligent connected platform with cutting-edge AI technologies and a self-driving platform – with this slick, tech-driven vehicle tailor made for the preferences of the younger generation.

Europe’s Creatures of Habit

In comparison to the attitudes of Chinese consumers outlined above, European consumers have typically been more hesitant when it comes to the adoption of electric vehicles, uncertain of EV capabilities and preferring to stick to what they know. For example, a recent report found that the mainstream adoption of EVs in Europe has been hindered by insufficient charging infrastructure in some regions.4 An estimated $1.8 billion of investment is required in the EU in the year 2025 in order for the public charging supply metric to be deemed merely adequate by this time.5

However, the fact that lack of charging infrastructure is now the top concern for European consumers suggests that they are starting to see EVs as a realistic option for their next car purchase, and are now considering the practicalities of ownership. Concerns about the range of EVs, also known as ‘range anxiety’, has historically been a key reason behind European consumers’ unwillingness to purchase an EV, but as technology advances this is beginning to shift.

Linked to this, Europe has seen more EV sales growth than any other regions in 2019, and one of the key catalysts behind this in recent times is due to a growing concern about

climate change among consumers. European consumers are looking to live more sustainably – reflected in greener buying habits – and car purchases are no exception.

The vast majority of European countries have set climate change goals – for example the UK has proposed a ban on all polluting vehicles by 2035 and a target of net zero emissions by 2050, and Germany plans to cut gas emissions by 40% by the end of 2020 – so governments have put a number of policies in place which further incentivise European consumers to make the shift to EVs. In Germany the government has also doubled existing subsidies to almost $7000 on EVs costing less than $45000, and in France private consumers who buy EVs that cost up to $50,000 now receive an almost $8,000 incentive. Unlike the Chinese market, the uptake of EVs in Europe has been driven through the necessity to respond to stringent climate change targets and therefore, consumers’ view of EVs as a green vehicle – rather than being a gadget or an opportunity to own a high-tech product.

Motivated by a desire to be more sustainable, combined with Government incentives, it is highly likely that we will see a significant increase in the uptake of EVs among European consumers.

Market predictions: what’s next for China in a post-subsidy era?

In the world’s largest market for EVs, the growth trajectory remains unclear. The recent slowdown suggests that in the absence of government subsidies, the rate of growth will likely not continue at the same pace as it has previously.

Originally, the Chinese plan had been to remove EV subsidies by the end of 2020. However, in March of this year, in part due to the downturn caused by Covid-19, the decision was taken to extend them. The revision now includes consumers who buy new electric vehicles through 2022 and tax exemptions on purchases for 2 years.

The full plan will play out to cut subsidies by 20% in 2021 and 30% in 2022.

What remains unchanged however, is China’s ambition to be a leading player in automotive on the global stage. Other than resulting in a sales slowdown, the decision to cut the subsidy has also led to another important development – a major sector shake-out. Pre-pandemic a whopping 400-plus Chinese companies were operating within the internal EV sector, however, some companies reliant on subsidies went bust. The remaining players that weathered the storm are now in a stronger position.

This all largely speaks to the Chinese government’s broader ambition of wanting to consolidate and build the strength of its homegrown automotive makers and create EVs that can compete with western OEMs.

For example, the decision to let foreign players like Tesla into the Chinese market, was a strategic one. The Tesla Model 3 is currently China’s most popular electric car.

By setting up a facility in Shanghai, the company has benefitted handsomely from preferential loans from Chinese banks and approvals from the Shanghai government. Tesla’s unwavering popularity in China seems to be going from strength to strength, in a relatively short space of time.

But to have a Tesla supply chain is invaluable as it will give the Chinese a chance to learn and over time, to shift that support to their own homegrown OEMs. And the Chinese dream is to have a Tesla of their own.

Beyond its internal market, China aims to become a global automotive superpower, and considers wider penetration of China’s own EVs as essential to that objective in the longer-term.

A green powered bounceback in Europe?

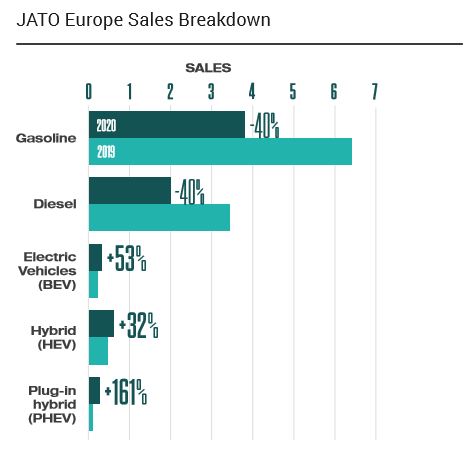

Sales of EVs in Europe are skyrocketing with sales up by over 50% year-on-year through August.

And rather surprisingly, Covid-19 hasn’t deterred the growth of EVs in Europe. In fact, European countries are using the pandemic as a premise to make a green recovery out of the crisis, with some governments creating additional purchase incentives as part of their Covid-19 economic-stimulus programmes.

There is little doubt that the market in Europe is starting to gain real momentum, and it increasingly seems that the continent is taking a leaf out of China’s book by ramping up state intervention to accelerate uptake and growth, as it races to meet carbon emission targets.

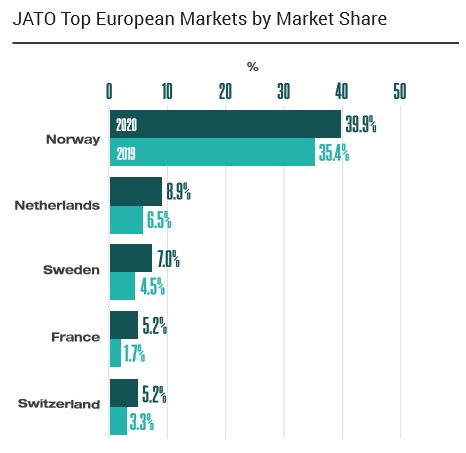

Norway is currently leading the charge in Europe, in part due to its enduring commitment to electrification since the 1990s. With an original plan to have 100,000 electrified vehicles on the road by 2020, Norway exceeded this number in 2018.

Norway posted the highest pure electric car registrations last year with 60,400 units which equates to 42% of total market. This year through August, volume totalled 38,600 units.

However, many European nations are looking to catch-up by setting bold ambitions and further incentivisation. For example, Germany’s ambition is to have a staggering 10 million EVs on the road and 1 million charging stations implemented by 2030. This summer’s €130 billion postCOVID-19 stimulus package included significant funding to boost EV incentives even more.

In France, President Macron has pledged €8 billion to the automotive sector as part of the Covid-19 recovery support package and is set to increase the state-provided grant towards an electrified vehicle purchase to €7,000 (from €6,000).

Notwithstanding these incentives, in Europe, adoption will be economic rather than regulatory, and only when parity in total cost of ownership is achieved will EVs begin to gain a significant share of new vehicle sales.

What’s next for China’s OEMs?

In a post-subsidy era, will Europe’s EV market be able to accelerate and rival China? Or will China be crowned successful in its pursuit of expanding into the European automotive market?

JATO’s Six Chinese Automotive Players to Watch in 2021…

MG

The renowned British brand WAS acquired by Chinese firm SAIC Motor in 2005 and has since found considerable success venturing into the EV market. In particular, the ZS EV model (a small SUV) released 1 September 2019 has already been ranked in the Top 10 EV models in a number of European markets. Initially on sale in the Netherlands and the UK, and will be available for purchase across Norway, France, Belgium, Italy, Austria in the near future. In fact, the ZS has risen to particular prominence in the UK, garnering 6% of the EV market and making it the UK’s fourth best-selling EV, only behind the Tesla Model 3, Nissan LEAF and Jaguar I-Pace.

Since switching to Chinese ownership, MG had spent the last 14 years attempting to capture markets across continental Europe. Last year’s launch of the ZS EV, showcasing its competitive range and pricing, created a long overdue opportunity for European success, that ICE models were previously unable to present.

And, SAIC Motor is not the only Chinese OEM hoping to gain traction in Europe….

BYD

BYD is China’s largest electric car maker and second largest in the world after Tesla.

It is the leading producer for rechargeable batteries in the world and has a strong presence In Europe through its electric bus (first released in 2010). More recently, it has begun to venture into the EU passenger electric vehicle market.

GEELY

The ambitions of Chinese OEMs go far beyond producing models for European markets. In the last decade, Zhejiang Geely Holding Group, discovered a quick route to Europe, acquiring established brands including Volvo and Lotus, however their ambitions haven’t stopped there. In fact, Geely has gone a step further, launching an open-source EV architecture. Sustainable Experience Architecture (SEA) aims to help elevate the availability of zero-emission vehicles across the world.

Geely Holding will make its breakthrough zero-emission architecture accessible to other original equipment manufacturers and third parties – a huge step for the industry, reflecting the common interest of tackling the challenge presented by climate change.

NIO

It’s not only large incumbent OEMs that Europe should be keeping a close eye on, competition arises in all forms, most concerningly from disrupters with the spirit of innovation in their blood.

Considered the “Tesla of China”, NIO – with its Internet giant background is the exemplary model for Chinese NEV start-ups. Its revolutionary concept of “Battery as a Service” (BaaS) has attracted important attention and although NIO operates exclusively in China – it is planned that vehicles from the manufacturer will be available in Europe in 2021.

Currently, NIO offers the ES8, ES6 and EC6 in China, and due to their BaaS concept, models can be purchased without a battery, making them considerably more affordable. It is more than likely therefore, that the company could offer its vehicles to European consumers at extremely favourable prices, challenging any European incumbent.

AIWAYS

And, the competition doesn’t end with the price tag. In 2019, Aiways challenged its U5 model to drive from China to Germany – travelling approximately 15,022km in 53 days. This first showing in Europe 2019, clearly demonstrated the high quality of the product, showcasing China’s unique capabilities in the EV market. Since then, Aiways have distributed their model in France, and placed new focus on online partnerships such as their work with German trade partner ‘Euronics’.

Unsurprisingly, Chinese OEMs are finding multiple routes into the European automotive markets, including entrance by supporting challenger brands.

CAMEL GROUP

Croatian OEM, Rimac Automobili – currently acquiring Bugatti from VW Group – is dubbed “Europe’s Tesla” and known for its innovative work in the EV market including its latest model – the 1914bhp C-Two coupe, which is yet to enter production.

With so much “buzz” surrounding the company – this challenger brand has secured a huge amount of funding, the largest secondary shareholders being Chinese battery producer, the Camel Group.

Conclusions

China’s journey in becoming the largest EV market in the world in just under a decade remains living proof that the growth of EVs at pace, requires the backing of Government intervention.

State policy and support are integral to helping the EV industry to achieve the cut through it need to truly succeed. In particular, as consumer confidence is heavily reliant on infrastructure creation and keen price points, state intervention becomes integral to the EV market success formula.

This is evident when you look to markets outside of China, such as Norway where a concerted effort has been made to drive EV uptake since the 1990s and yielded strong results. In contrast, this can also be seen in the US, where a light touch regulatory approach has characterised a flattening out of the market.

China however remains fully committed to the evolution and revolution of the automotive industry and goal of the Boao Declaration, which aims for EVs to account for 50% of the global market by 2035.

With Europe tipped for the next EV boom, things are certainly set to get more interesting in the race for global EV domination.

And against all odds, the pandemic seems to have led to an acceleration of the EV rollout across Europe, with Governments upping subsidies and incentivisation.

A combination of these generous incentives and the reluctance of established brands to sell more EVs than needed to fulfil emissions regulations, present Chinese OEMs with a clear opportunity to move things up a gear.

It is apparent that Chinese OEMs are committed to this challenge. For example, understanding that heritage brands hold a considerable amount of sway with European consumers, they have sought to infiltrate the European market – through buying up shares or outright purchasing Western OEMs – rather than trying to sell Chinese brands to European consumers.

Whilst there is perhaps still some way to go until Chinese OEMs establish a strong foothold in Europe, it seems the Chinese government isn’t going to deviate from its long-term ambition to build the strength of its homegrown talent and create EVs that can compete with western OEMs. And when considering the formula applied by Chinese OEMs to their home market –

- an emphasis on affordable EVs

- ample consumer choice in terms of vehicle models (including SUVs)

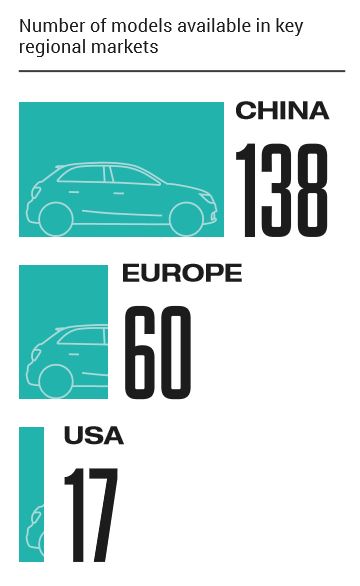

- vast EV ranges which dwarf European model ranges

- tech savvy vehicles

- designs led by consumer data and insight

- strong appeal to young consumers

It is difficult to envisage how the above elements, when applied strategically to the European market, would not appeal to mass consumers. So perhaps when it comes to global EV domination, it is more a question of how long it will take Chinese EVs to successfully enter the European market, rather than a case of whether they will succeed.