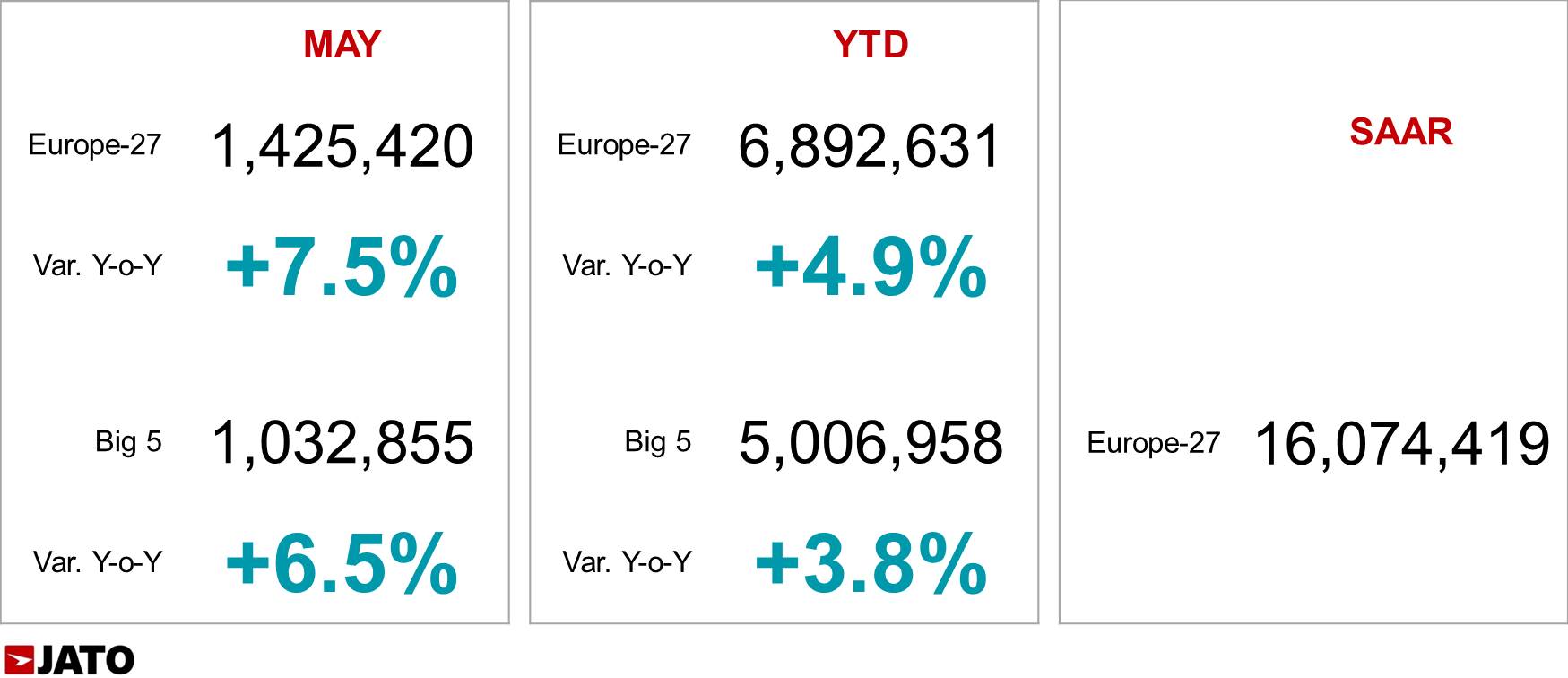

- European car registrations totalled 1.4 million units in May 2017, an increase of 7.5% when compared to the same month last year, and the highest May total for a decade

- Registrations of 3-door hatchbacks declined by 8.4% in May as European consumer preferences continued to change

- The Volkswagen Golf retained its position as Europe’s most popular car model – with the Polo taking second place

The European car industry returned to growth in May 2017, with new registrations for the month totalling 1.4 million – an increase of 7.5% when compared to the same month last year. In terms of volume this represents the highest total for May in the last decade, and is only 19,000 units behind the record total which occurred in May 2007. The positive performance was driven by a relatively stable economic and political situation in the majority of markets, as well as evolution in the automotive sector, with manufacturers bringing more models, new technology and purchasing routes to market.

Germany was a significant driver of the growth, the country posted an increase of 12.9%, Italy also performed well, recording an increase of 7.6% to become Europe’s second largest market. Other significant markets such as Spain, Poland, the Netherlands and Austria all posted double-digit increases.

Despite the overall growth of the market, a shift became evident as sales of 2/3 door versions of city-cars, subcompacts and compacts totalled 76,800 units, which is a decline of 8.4% on the same period last year. In comparison, their 4/5 door counterparts posted a 5.1% increase, registering 594,300 units. The poor performance of 2/3 door hatchbacks is the culmination of a longer-term decline which has seen sales of hatchbacks fall from 2.45 million in 2009 to less than 1 million in 2016 as manufacturers eliminate 3-door models. This was evidenced by the launch of the new Volkswagen Polo, which despite being a subcompact, will not be offered in a 3-door version. The decline of 3-door hatchbacks can be attributed to the changing preferences of European consumers who are increasingly rational when choosing small and compact cars.

“Overall, the market has returned to growth, driven by double-digit increases in many of Europe’s major markets. Amidst this, a shift is taking place with hatchbacks in decline. The presentation of the new VW Polo in June with the omission of a 3-door model is a symptom of a fundamental decline that could see 3-door hatchbacks vanishing from roads. There are many reasons for this, but the increasing practicality of cautious consumers is a major factor. As manufacturers shun 3-door vehicles meaning less choice for customers, the 3-door hatch – once a synonym for sportiness – could soon be consigned to history,” commented Felipe Munoz, Global Automotive Analyst at JATO Dynamics.

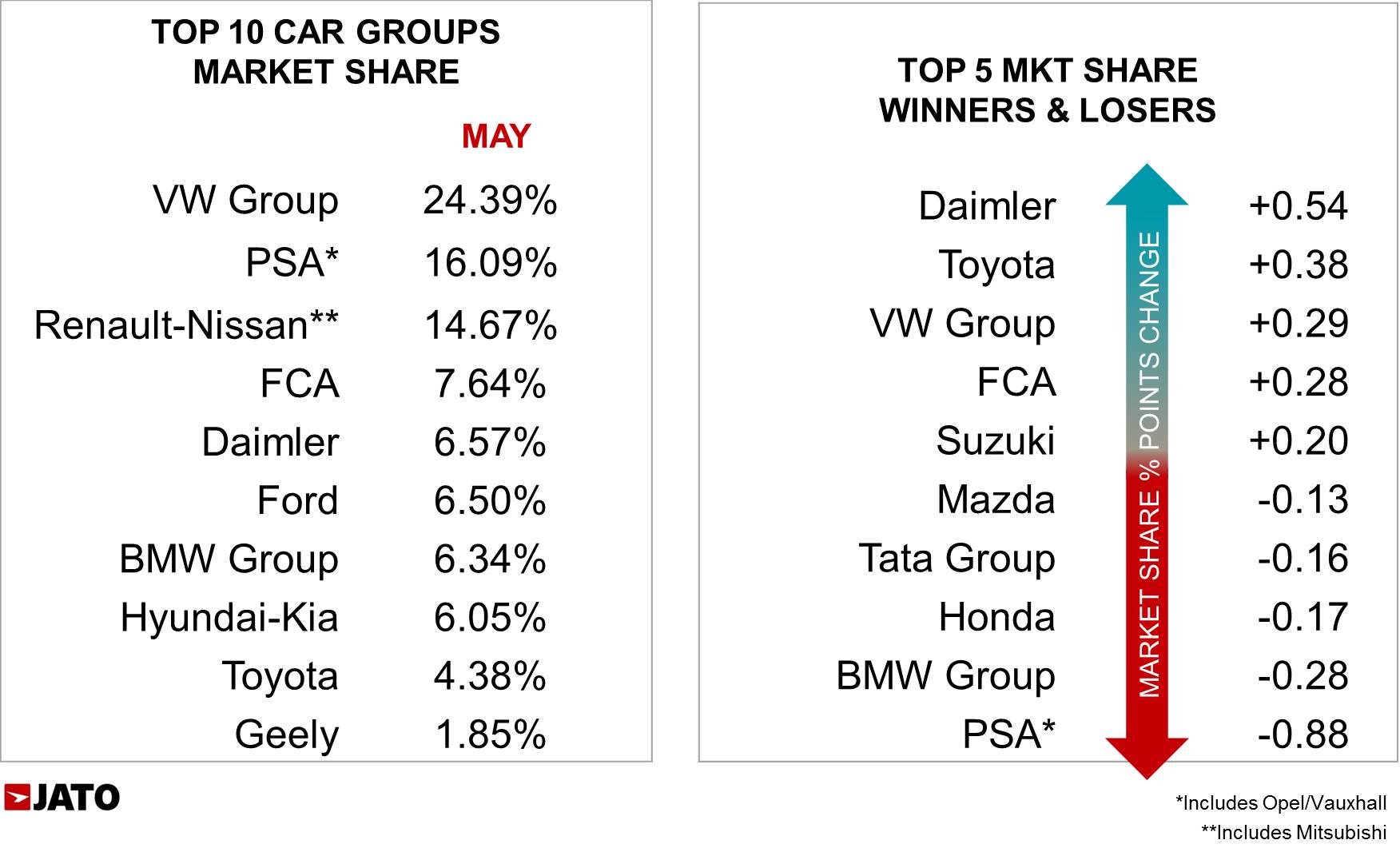

VW Group increased its market share following months of decline, as a result of the strong performance of the Skoda and Seat brands, both posted double-digit growth, whilst the Volkswagen brand registered an 8.7% increase.

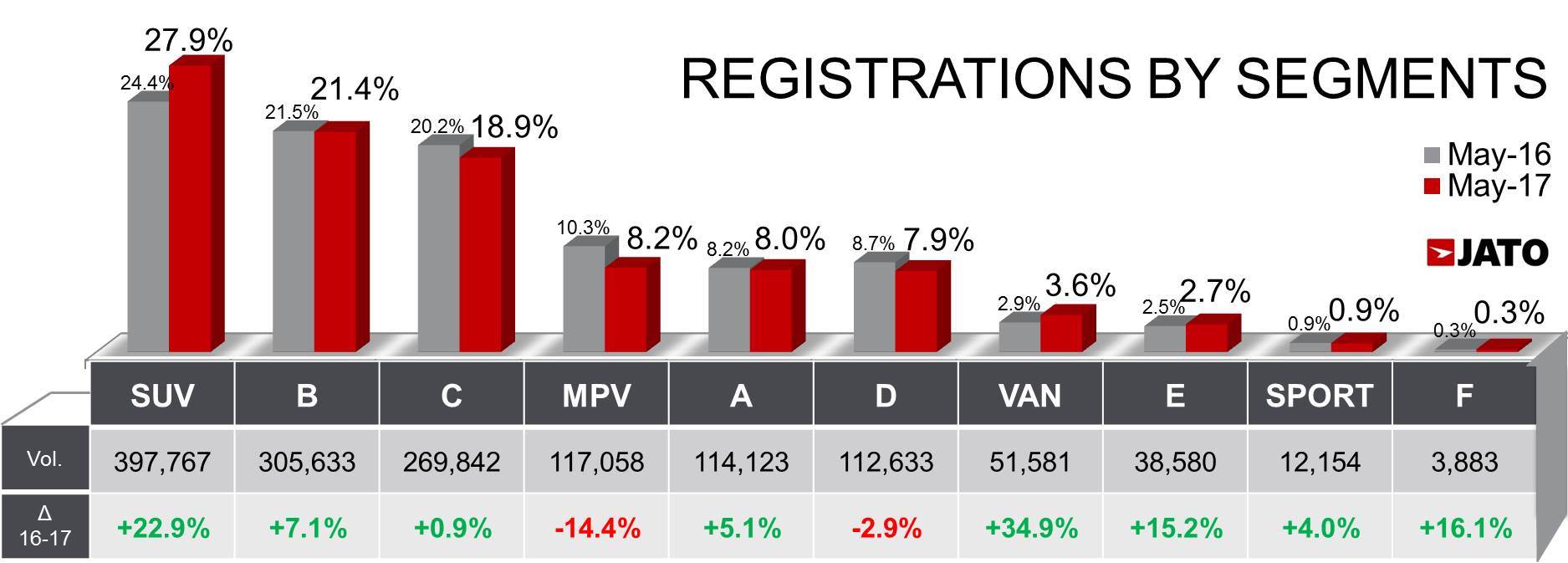

SUVs were a major driver of growth, accounting for 28% of the total market as a result of a 22.9% increase in registrations. The VW Golf maintained its lead but lost ground, whilst the Polo was the second best performing car.