Europe is a relatively open market for new cars. The different trade agreements and the relatively low taxes on imports allow the arrival of different brands and models from all over the world. Safety and emissions regulation is one of the main barriers. In any case, the European car market today welcomes more than 80 different brands that are coming not only from Europe, but from USA, Japan, South Korea, China, and India.

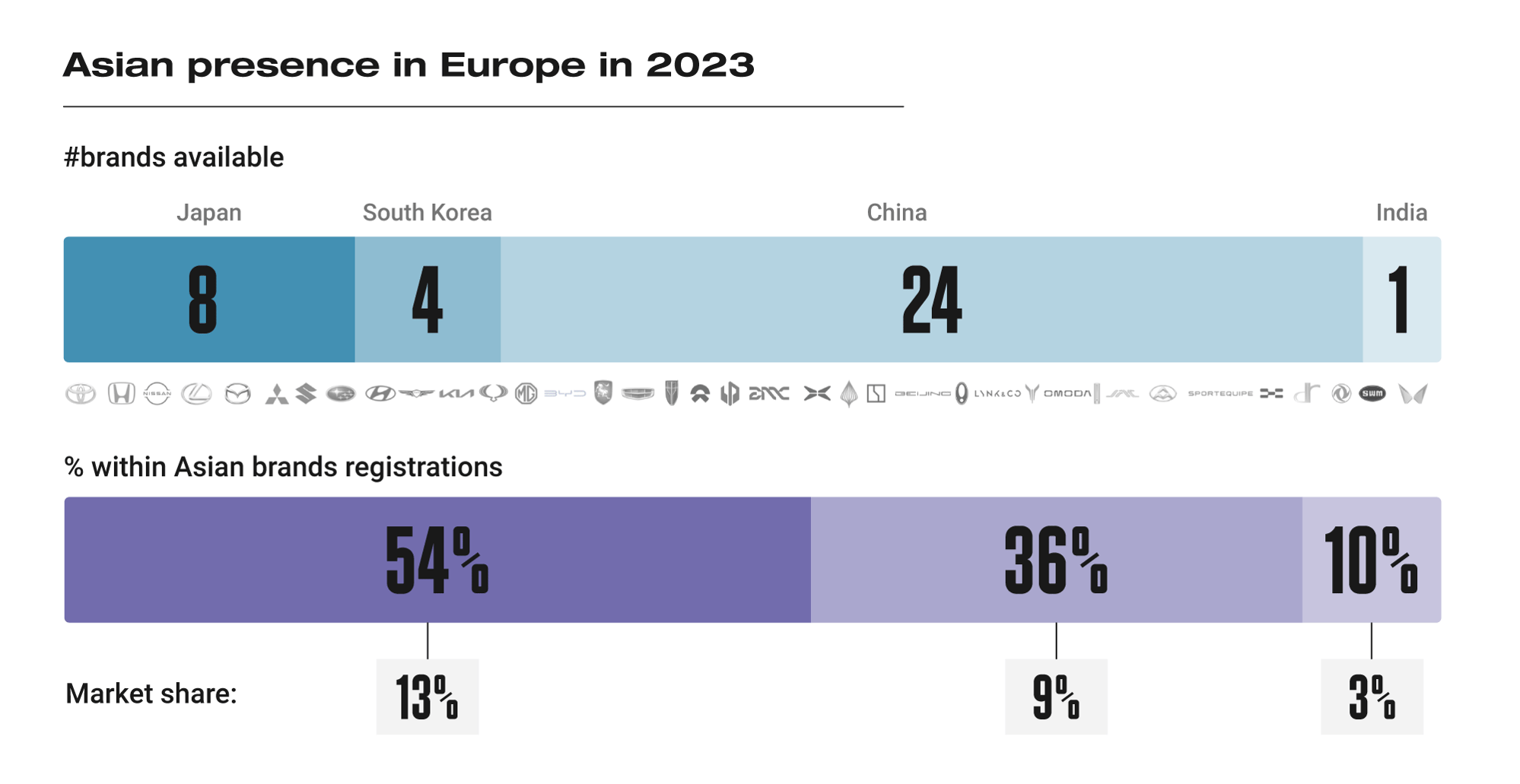

Among them there is the increasing key role of the Asian car brands. By December 2023, there were 37 different passenger car brands from this continent available in Europe. Although they were the latest to arrive, most of them are Chinese brands, followed by Japan, Korea, and only one in India. But the significant Chinese presence in terms of offer, is not reflected in terms of demand.

Last year, the Japanese car brands counted for 54% of the Asian brands selling cars in Europe. They were followed by the Koreans, which made up 36% of the Asian group; and finally, China with 10%. In terms of overall market share on passenger car registrations, the Japanese OEMs counted for 13% of the total market, followed by the Koreans with 9% share, and China with 3%.

From the 24 Chinese car makes available in Europe by December 2023, only 9 registered more than 1,000 units. There’s a long way ahead for them.

China, the next wave.

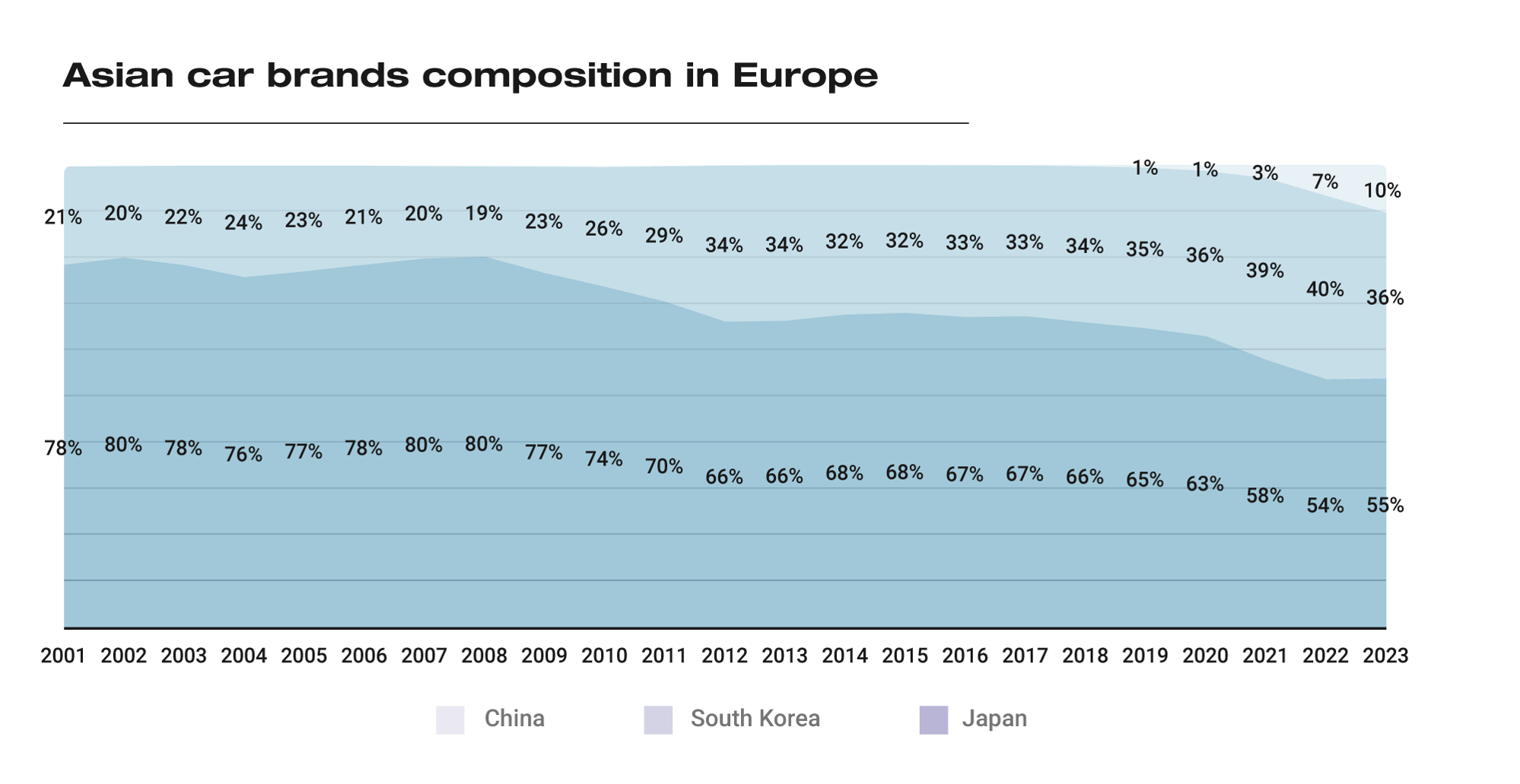

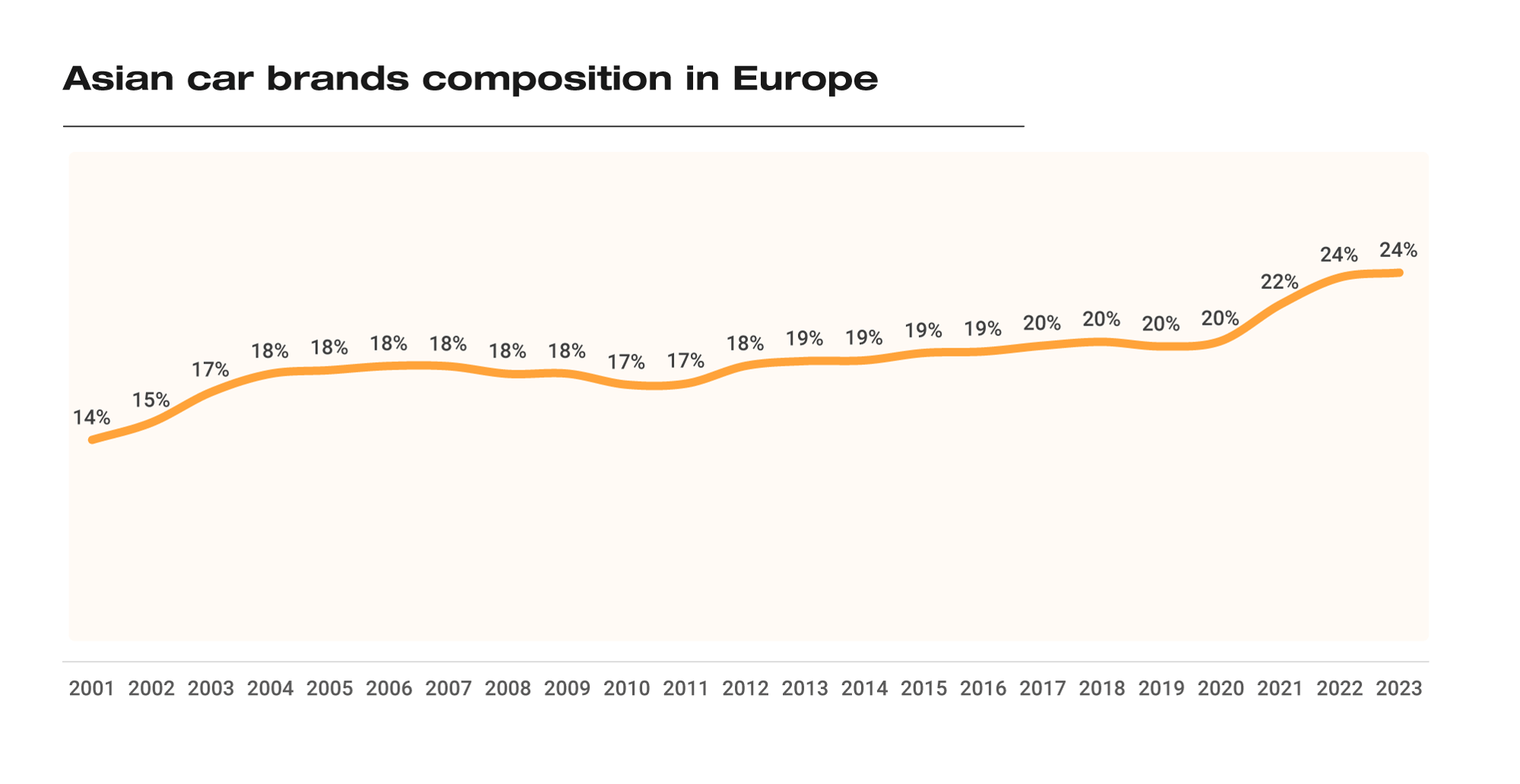

The evolution of the Asian OEMs’ presence in Europe is quite interesting. First it was the Japanese makers which arrived and gained traction in the 90’s – 00’s. After years of learning from the European consumer, they finally produced competitive products designed for the consumer there. They localised the production and became a strong alternative to the European mainstream brands.

Then it was the turn for the Korean players. They followed the same formula used by their Japanese peers and finally took off during the late 00’s, early 10’s. Quality, wide range of products, and localisation helped them to gain traction up to the point that today two of their brands sell more cars in Europe than all the Japanese ones, except for Toyota.

Now it is China’s turn. They want to replicate the success stories of their Asian competitors, but faster. They have the resources and products to do it, but it won’t be without its challenges. Although they have increased their presence quite fast since 2021, they face different challenges. There are still issues with perception in the West when it comes to Chinese products, and positively influencing that consumer perception will be key.

These three groups have been able to increase their market share in Europe from 14% in 2001 to 24% last year. The remaining question is whether the arrival of the Chinese manufacturers will steal market share from Asian competitors, or from European ones.

Made in Asia

Made in Asia

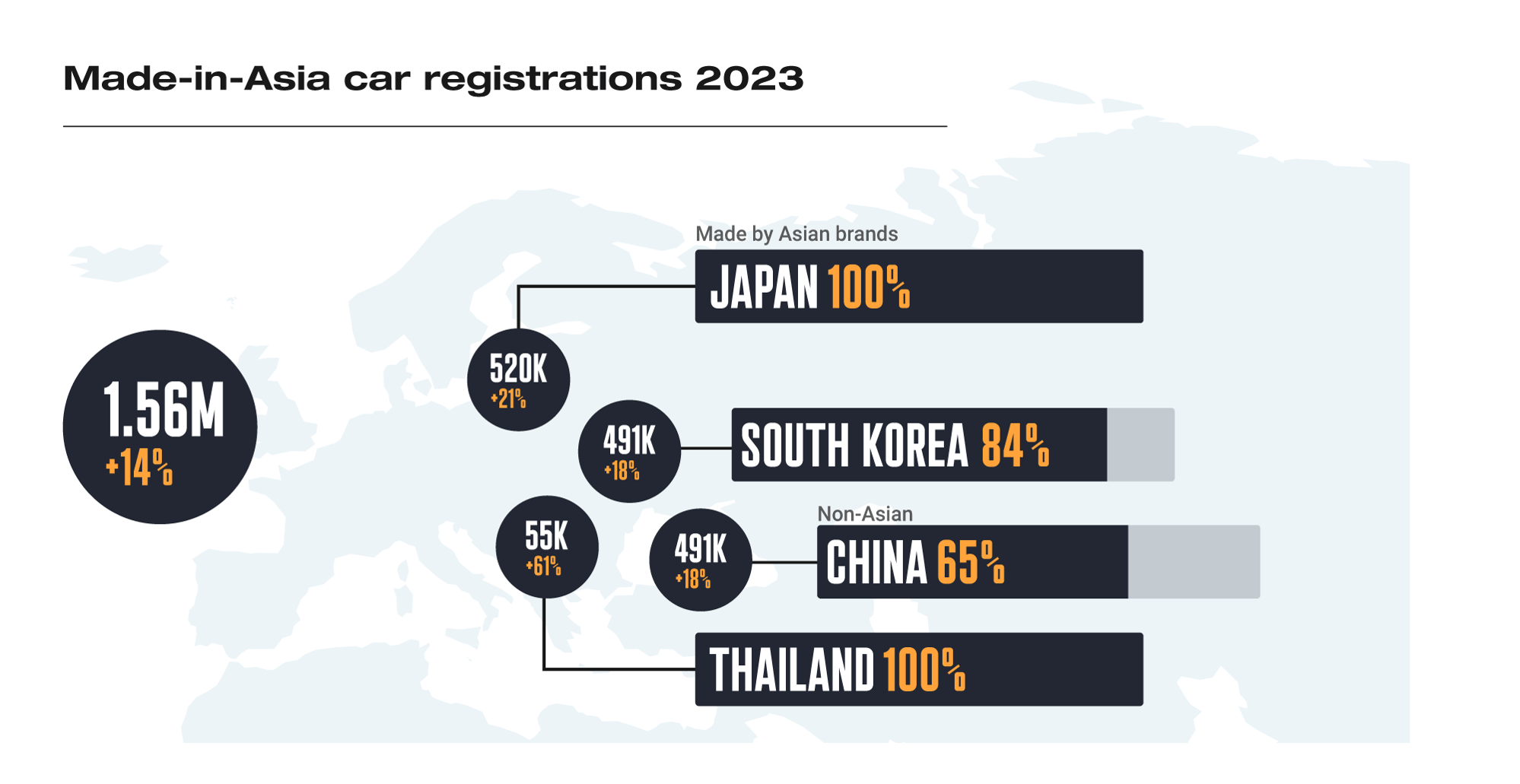

The story changes when looking not at the nationality of the car brands but at where the cars are manufactured. Toyota is a Japanese brand but a large proportion of the cars it sells in Europe, are made locally. Last year, a total of 520,000 cars made in Japan were registered in Europe. They were all produced by Japanese companies.

Korea imported 495,000 cars that were registered in Europe, up by 2% vs 2022, with 84% of them made by Korean makes (the remaining 16% corresponded to Renault vehicles). In the case of China, there were 491,000 Chinese made cars registered in Europe, of which 65% were made by Chinese brands. This country is a popular destination of foreign investment and a big export hub: Tesla, Dacia, Volvo, Mini, BMW, Polestar import Chinese made models.

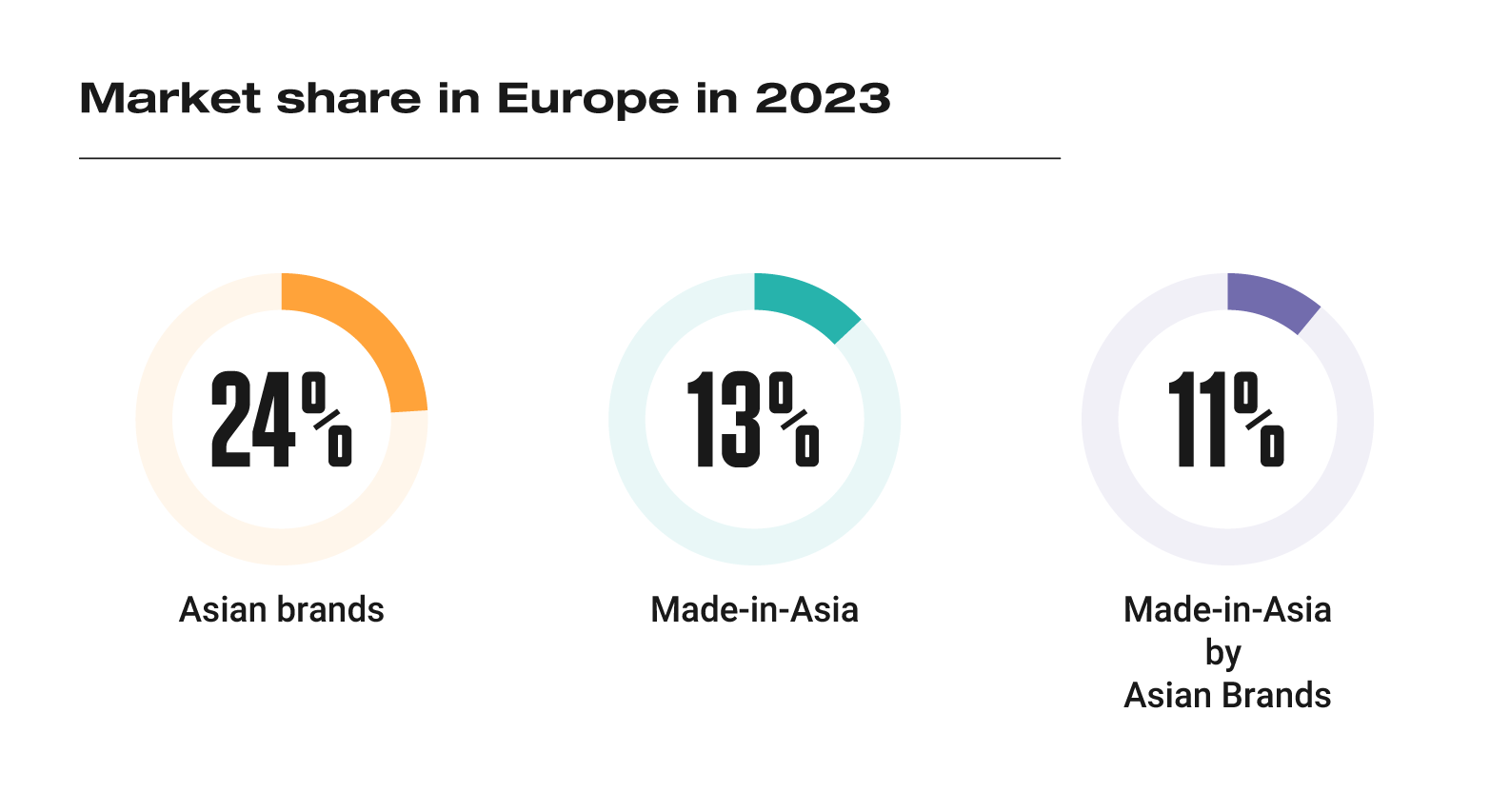

Therefore, you have different market shares for the Asian origin cars. The Asian brands represented 24% of the new passenger cars registered in Europe last year. In contrast, the made-in-Asia cars counted for 13% of the total; and the ones made in Asia by Asian brands made up just 11% of the total.

What’s their strength?

Reliability is associated with the Japanese brands. Competitiveness with the Korean ones. For now, low prices are what is mostly associated with Chinese brands. They all shine in different ways. Their strength varies according to the segment or powertrain.

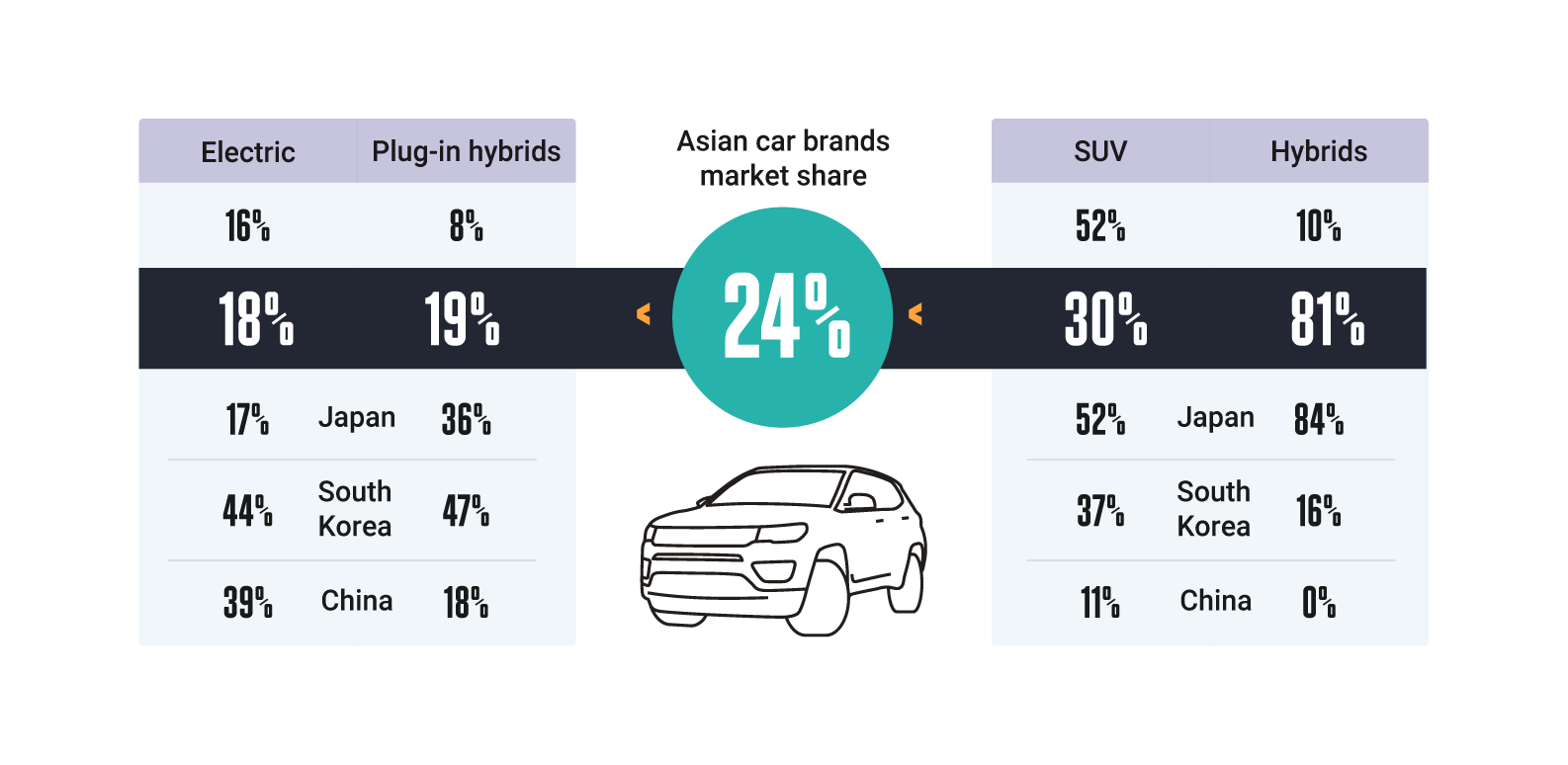

For instance, the Japanese brands are strong with hybrid technology. Market share for these vehicles totaled 10% last year, and Japanese brands counted for 84% of the registrations of Asian brands. Korea shines within the plug-in hybrids with 47% of the Asian mix. Meanwhile the Chinese makes had good results within the electric segment with 39% of the Asian mix.

In total, the Asian car brands posted their highest market share in the hybrid segment at 81%, followed by the SUV segment with 30% share, the plug-in hybrids with 19% share, and the fully electric cars with 18% – not bad results.

Are Chinese brands dominating?

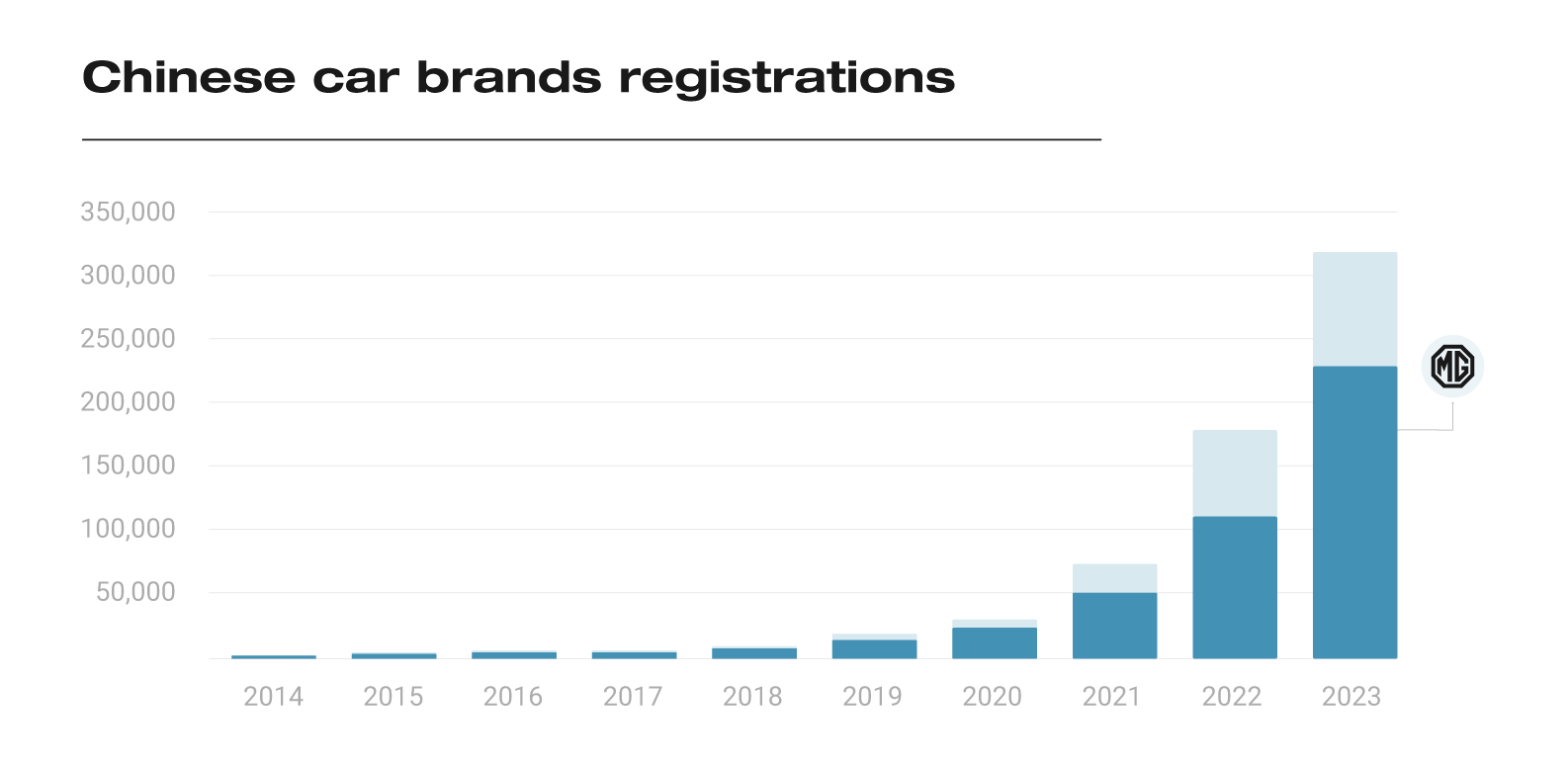

Despite somewhat sensational headlines designed to create the impression that Chinese brands are starting to dominate the European market at pace, the numbers tell a more tempered story. Last year, the registrations from Chinese car brands totaled 321,300 units out of 12.81 million units throughout Europe (or just 2.5% of the total). Moreover, 72% of this total was registered by MG, a fully Chinese brand from production to design, but positioned as British in the West. To the European public, the Chinese cars are still a rare thing to see on the streets.

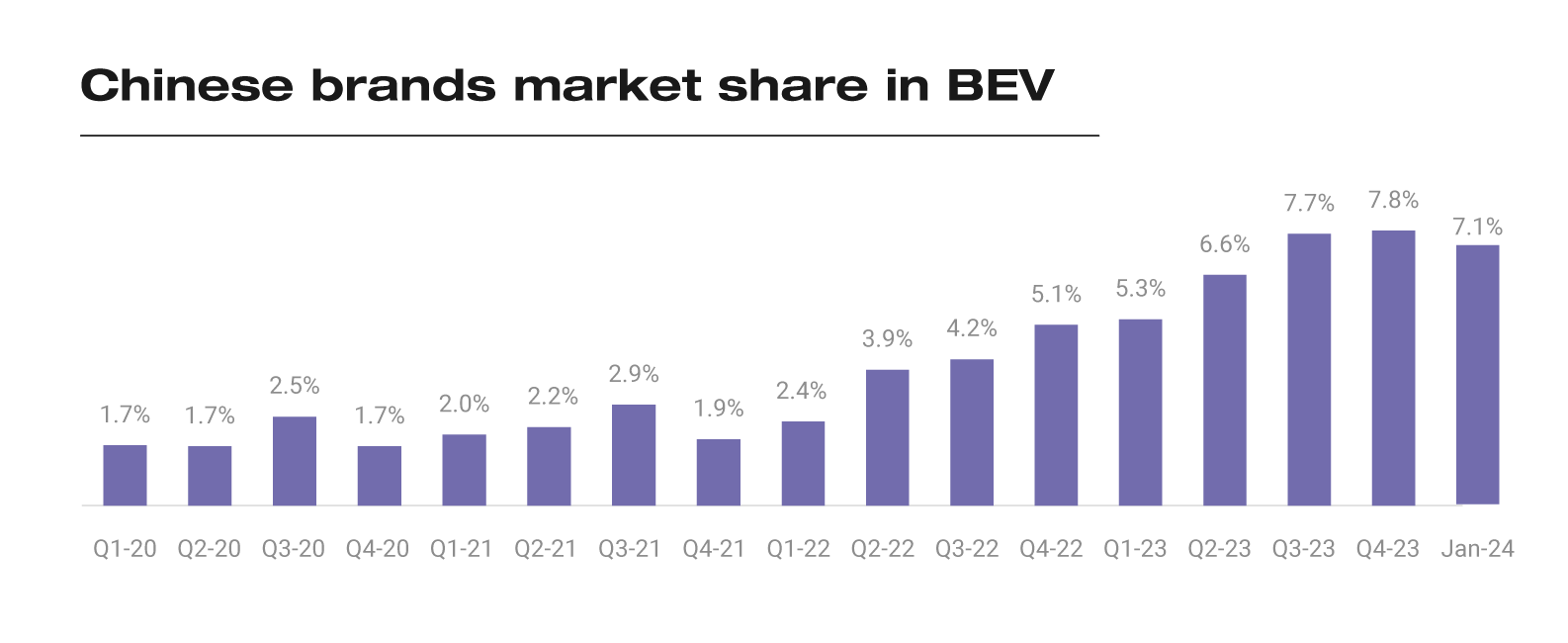

Nevertheless, they are more visible within the BEV (Battery Electric Vehicle) segment. China is ahead of Europe and USA when it comes to electric cars. They don’t only have more resources and a bigger local market with economies of scale, but they own a big part of the supply chain around the batteries production. This advantage is evident when looking at their latest electric cars and their prices.

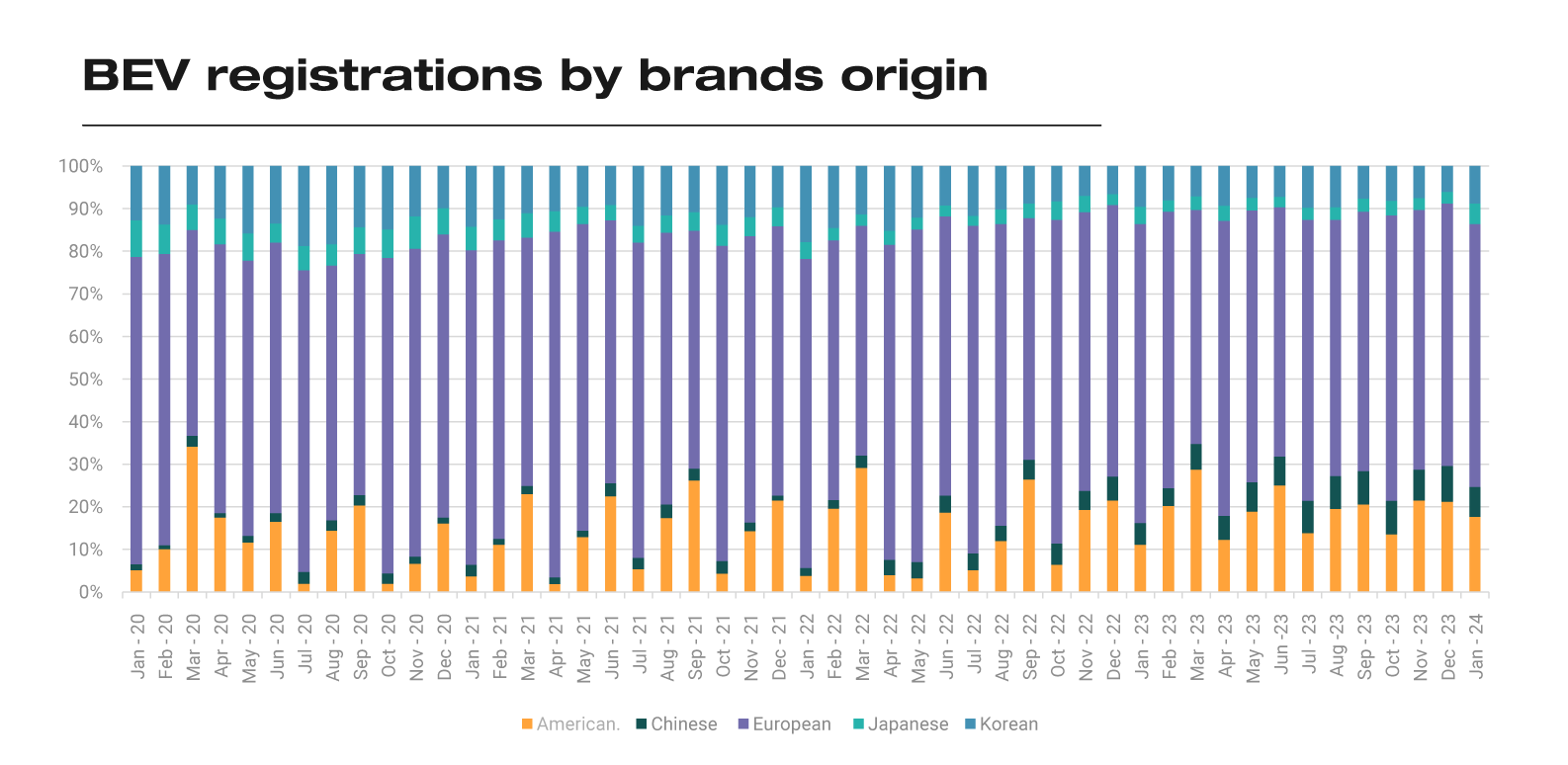

This is why MG was able to place its compact MG4 as Europe’s 4th most registered electric car in 2023. The Chinese electric cars from Chinese brands made up 7.8% of the BEV registrations in Q4 2023, up from 5.1% in Q4 2022, and 1.9% in Q4 2021.

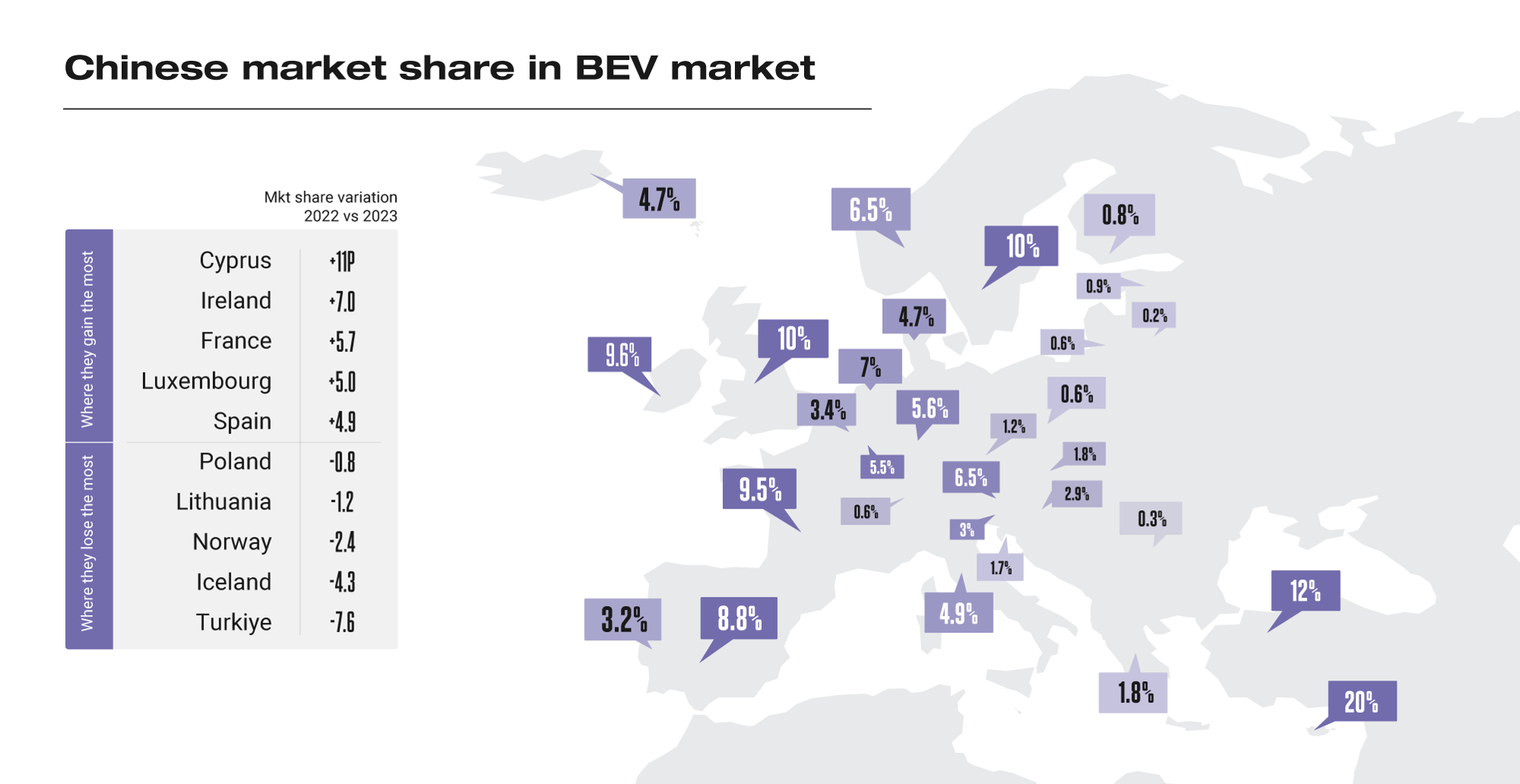

Their growth is being driven by markets like Cyprus, the UK, Sweden, France, Turkey, and Ireland, where their market share is quite high. MG of course is responsible for a big part of these strong results.

A matter of price

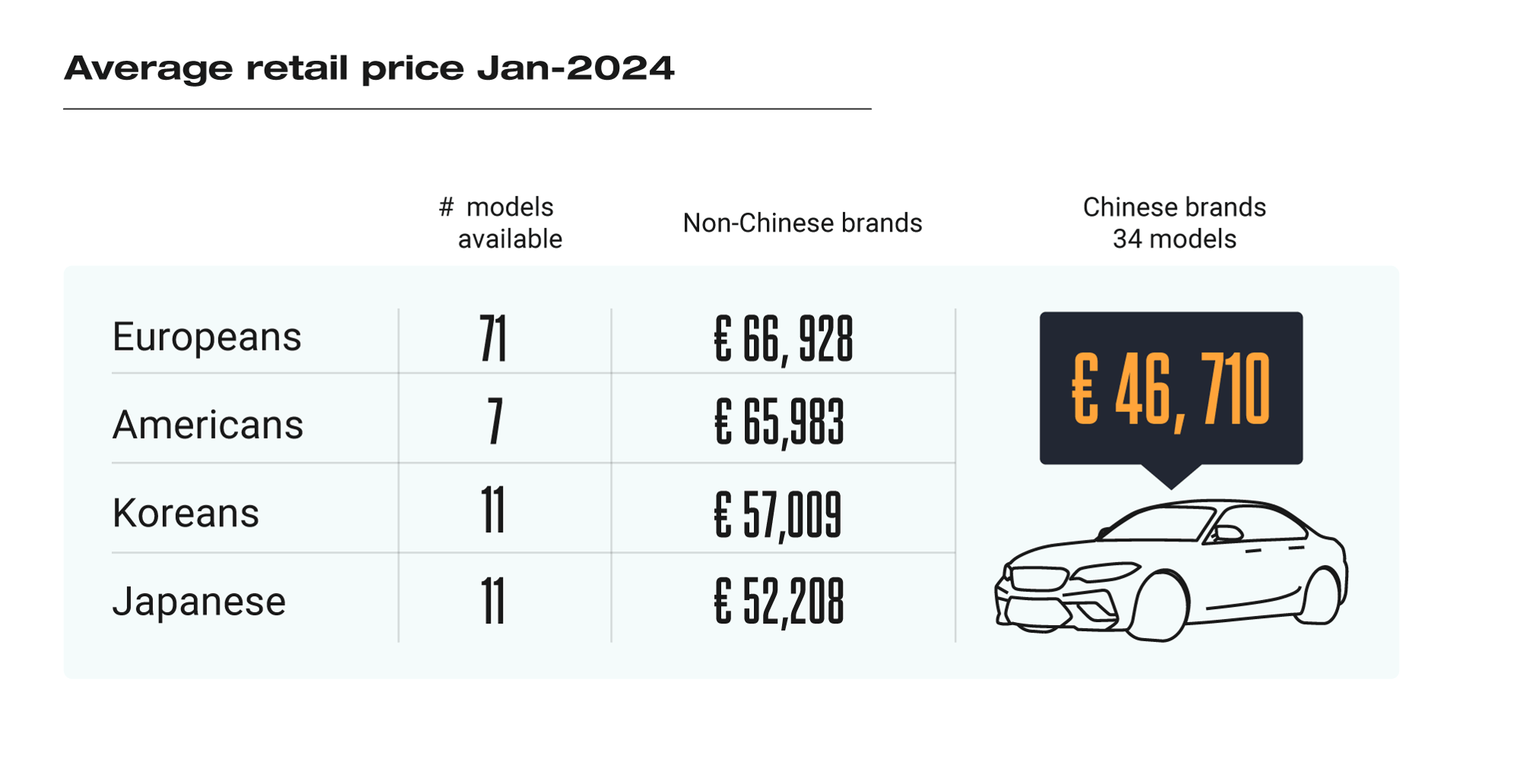

The competitiveness of the Chinese electric cars over the Europeans, Americans, Koreans, and Japanese is partly explained by their low prices. According to our data, the average retail price of a Chinese electric car in Europe during January was 30% lower than the average posted by the European competitors. In total the former was an average of 20,200 euros more expensive.

Why? Lower labour costs at home, more economies of scale, and more control over the supply chain of battery parts allow the Chinese cars to be cheaper than the rest of the offer. In addition, Chinese automakers may benefit from government support in ways not available to their European and American counterparts.

The price card will definitely help China to expand its presence abroad, at least until various imminent measures in the West take effect. Following the IRA (Inflation Reduction Act) implemented by the Biden administration in USA, Europe too is getting ready to respond to this threat. An investigation about potential subsidies on electric cars coming from China is underway. The European Commission needs to find the way to protect its industry without hurting the trade rules.

Europe’s response

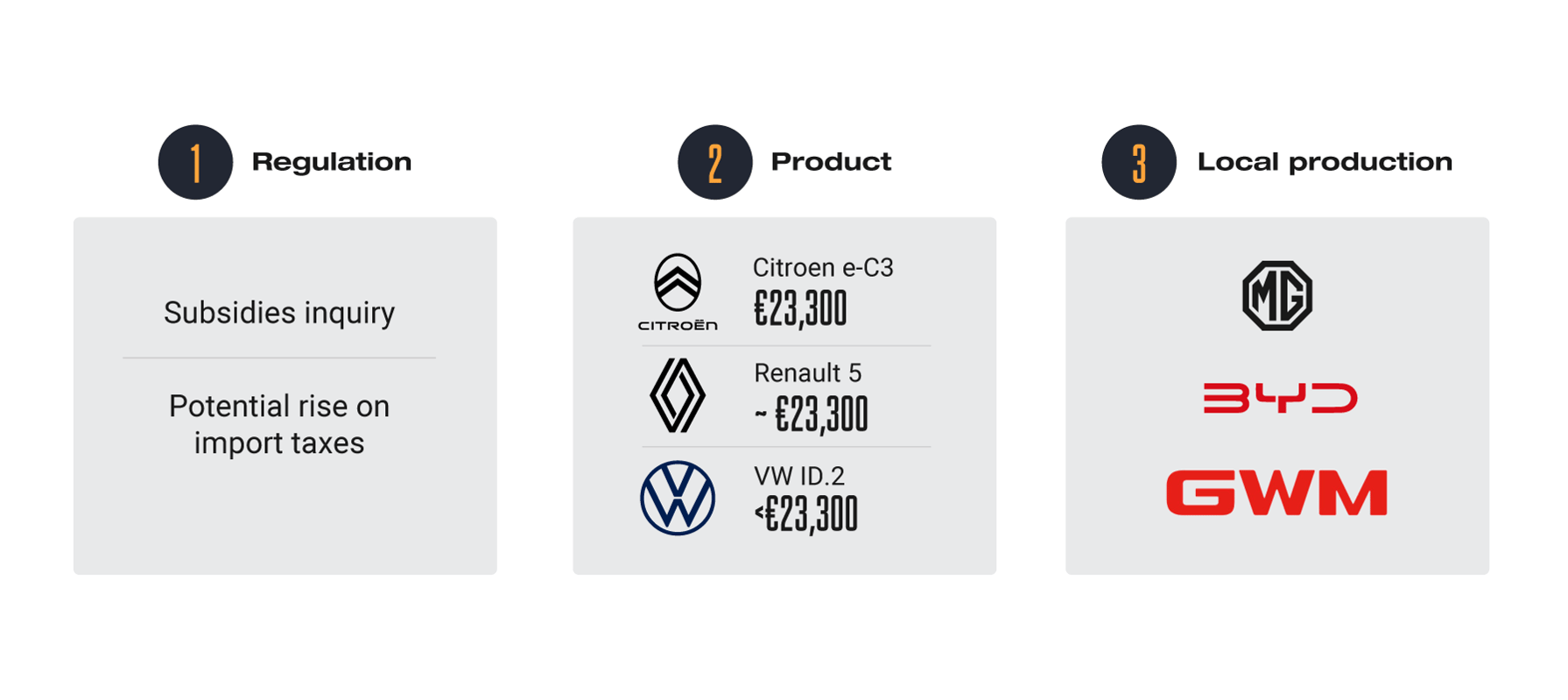

The response from Europe could then be at the trade level in the usual taxation way, but also through the enhancement of local production. Eventually the Chinese car manufacturers will need to localise part of their production in the markets where they want to sell properly. It is something that the Japanese and Koreans did to gain traction. The question is whether producing locally will affect their competitive prices.

In the meantime, the European carmakers are hurrying up to produce more affordable electric cars. The Citroen e-C3, Renault 5, and the upcoming Volkswagen ID.2 are examples of how much progress has been made regarding the affordability of these vehicles, but there is still a long way to go in terms of introducing competitive cars.

Written by Juan Felipe Muñoz-Vieira, Market Analyst & Senior PR Manager at JATO Dynamics.

Are you a franchised car dealership in the UK, Germany, Italy, Spain or France? As Chinese car brands continue to grow in Europe, they will add to our vast data within JATO Sales Link – a FREE data-driven insights tool exclusively for franchised car dealers. We have insights from hundreds and thousands of real-life transactions so that you can see what makes, models and trims are most popular, what options and packs are buyers choosing to add on, and details around pricing such as the final sales price and discounts applied.