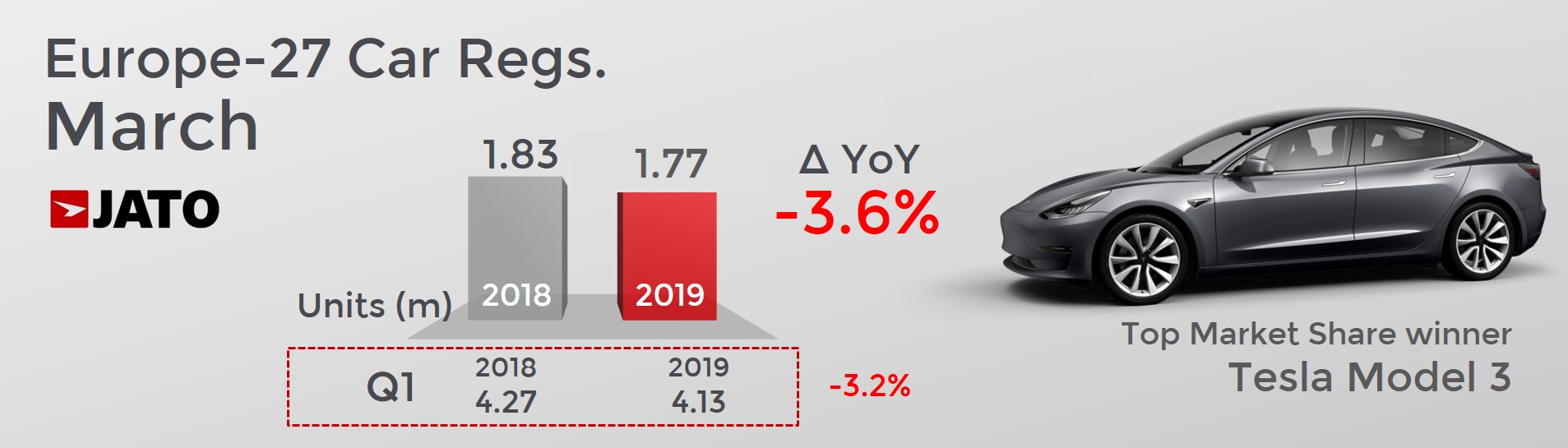

- Total registrations fell by 3.6% in March – the 7th consecutive monthly drop

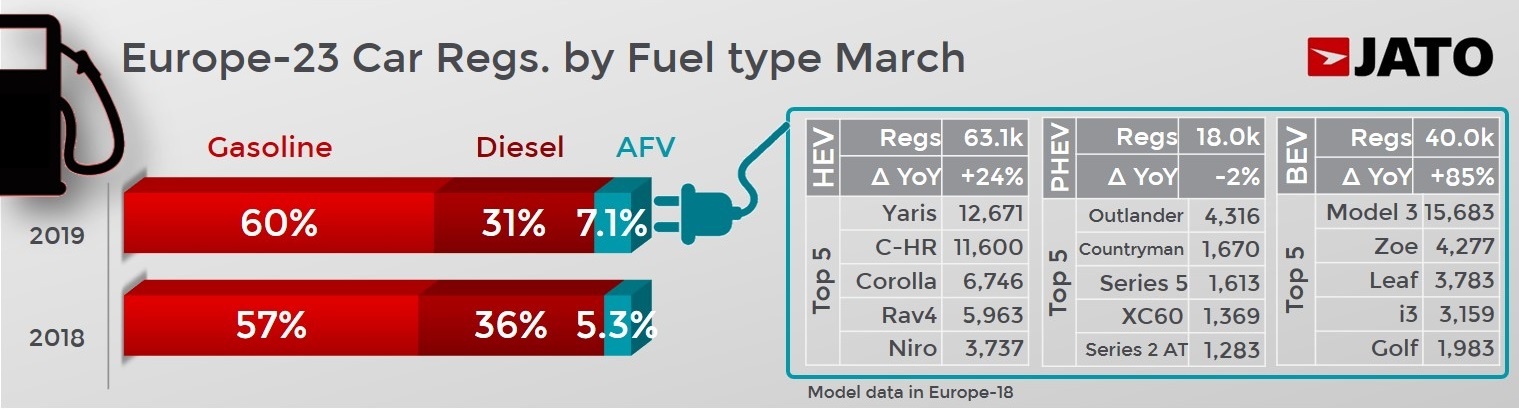

- Diesel cars counted for 31% of total registrations, the lowest monthly share since September 2000

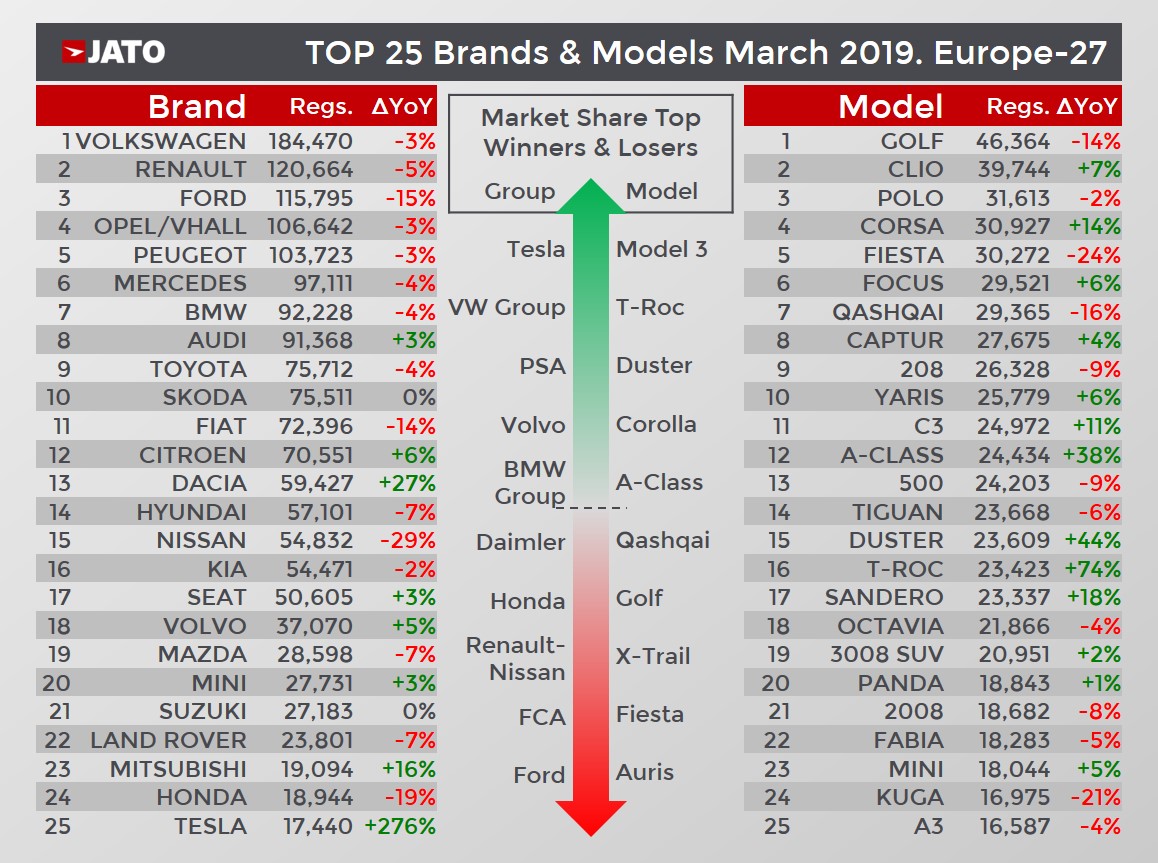

- The Tesla Model 3 was the top market share winner

- Q1 registrations totalled 4.13 million units, down by 3.2%

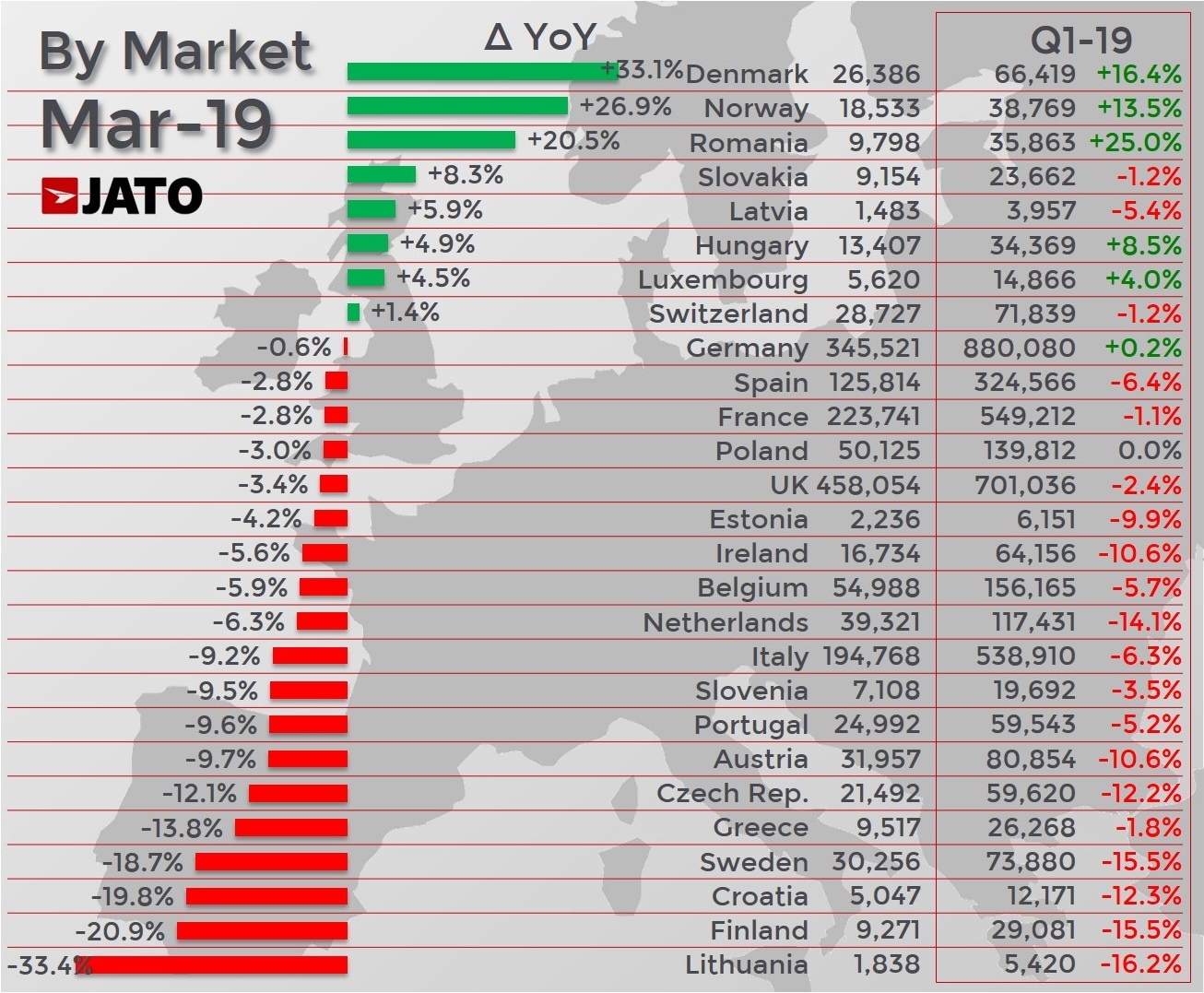

The European car market registered its seventh consecutive month of decline in March 2019. Ongoing political and economic uncertainty, including lack of clarity around Brexit, alongside consumer preoccupation with diesel bans in cities, meant that overall demand continued to decline. Last month, 19 of the 27 markets included in this release posted negative results – including the top 10 largest markets in Europe. The figures for Q1 provide a broader snapshot into the downward trend, with only 6 countries recording growth.

While overall demand may be on the decline, the good news is that the electrification shift continues at pace, with a significant result in March. It was the first time that registrations of electrified cars (BEV, PHEV, HEV) exceeded the 100,000 units mark, with a total of 125,400. Demand was up by 31% – mostly driven by German, Norwegian, Spanish and Dutch registrations. Electric and plug-in hybrids counted for almost half of that total, but the real driver of growth was the BEV, whose registrations increased by 85%.

Felipe Munoz, JATO’s global analyst, commented, “It was always going to be a challenge to maintain the growth rate we’ve seen in recent years thanks to recent events such as WLTP and legislation around diesel, as well as the impending CO2 targets. Despite the negative trend we’ve been seeing since September last year, the market is still strong in terms of volume and offer. In fact, a slow-down after many years of growth is not bad at all.”

The rapid volume growth of pure electric cars was mainly due to the outstanding results of Tesla. Thanks to strong demand for the Model 3 the brand entered the top 25 best-selling brands in Europe. Registrations of the Model 3 jumped from 3,747 units in February (revised) to 15,755 units in March – meaning it was Europe’s top selling electric car.

The Tesla Model 3 was also the top-selling premium midsize car in March. While it was able to outsell its rivals in the sedan category in February, the smallest Tesla was able to outsell all of its rivals in March, including all body-types.

At the same time, diesel cars continued to lose ground. Last month, they recorded the lowest monthly market share since September 2000. Total diesel registrations counted for 31.2% of total volume against 36.2% in March 2018, and 44.8% in March 2017. Despite the big drops posted last year it seems that concern among consumers is still affecting demand, and the trend has not hit rock bottom yet. The biggest drops were posted by Mercedes, Renault, Peugeot, Ford and Land Rover. In contrast, Volkswagen, Skoda and Seat saw increases in diesel registrations.

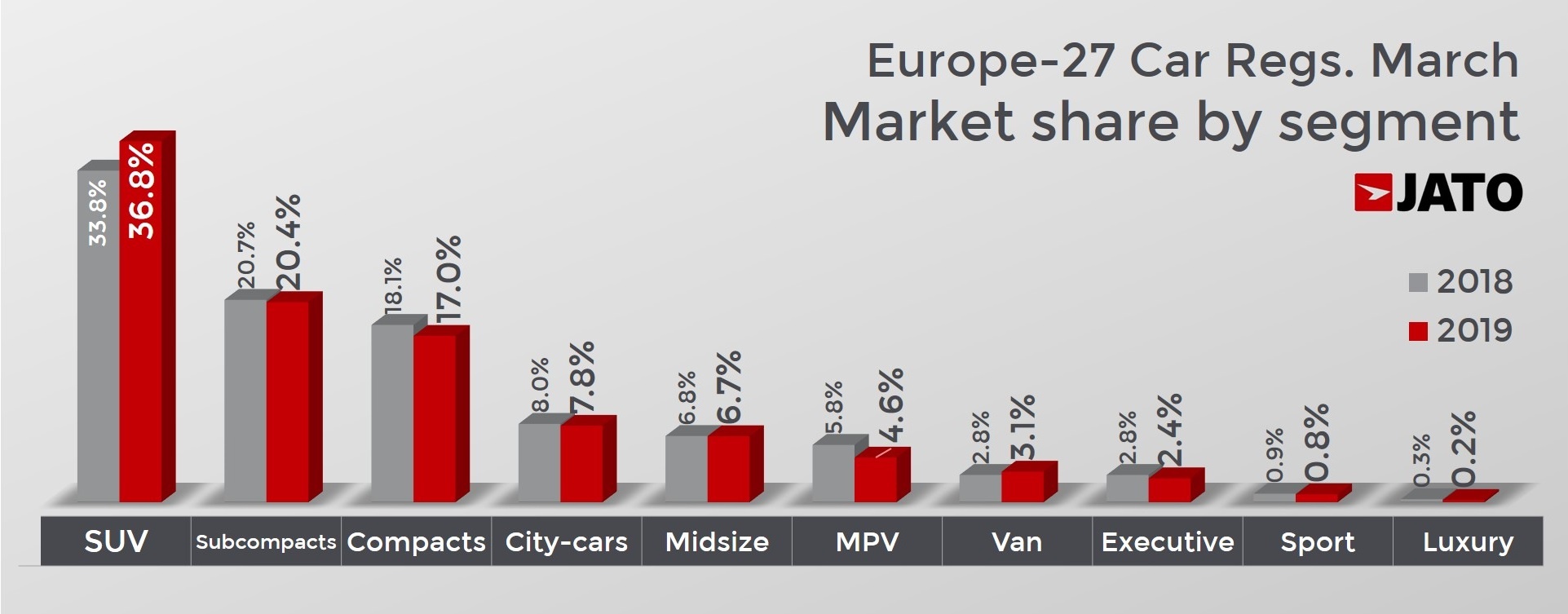

The market continues to be dominated by SUVs, but their growth is slowing. In March, SUV registrations totalled 650,300 units, or 36.8% of total volume. However, their sales performance is not as strong as it has been in the past, with volume growing by “only” 5%. Volume was up 11.7% for small SUVs, and 5.3% for compact SUVs. The rest of the SUV market posted declines. VW Group, Renault-Nissan and PSA led the SUV segment in March and in Q1.

The VW Golf continued to lead the European ranking by models, despite a 14% drop in volume in March. The best performer of the top 10 was the Opel/Vauxhall Corsa, which posted strong growth in the UK, Germany and France. The Corsa is an older product but sold almost the same quantity of units as the Volkswagen Polo, whose latest generation has been in the market for about a year.

It was also a good month for the Citroen C3, Mercedes A-Class, Dacia Duster, Volkswagen T-Roc. Outside the top 25, the Tesla Model 3 occupied the 27th position; the Opel/Vauxhall Crossland and Citroen C3 Aircross saw increases of 32% and 23%, respectively; the new Audi A1 was up by 31%. Other results included: Opel/Vauxhall Grandland +32%, Skoda Karoq +32%, Seat Arona +34%, Seat Ateca +35%, Hyundai Kona +86%, Volvo XC40 +209%, Opel/Vauxhall Adam +53%, Kia Niro +57%.

Registrations among the latest launches were as follows: Ford Focus, 29,521 units; Mercedes A-Class, 24,434; Tesla Model 3, 15,755; Audi A1, Q3 and A6 12,453, 9,743 and 9,173 respectively; Toyota Corolla, 8,943; Mercedes B-Class, 6,866; Citroen C5 Aircross, 6,357; BMW X5, 3,966 units.