PSA-Opel lost market share, as European car registrations increased by 1.2% in February 2017

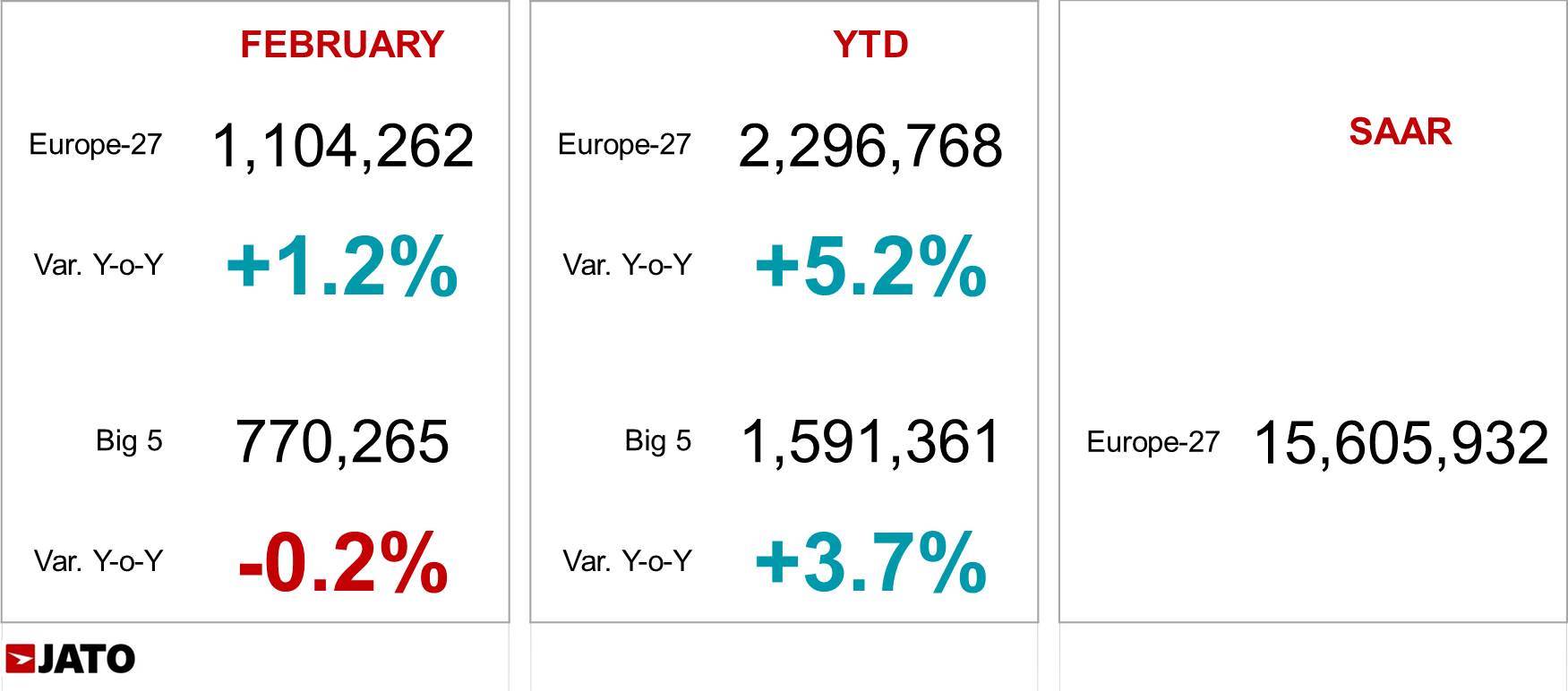

- European car registrations totalled 1.1 million units in February – which constitutes the second highest February result since 2008

- Key markets driving the growth were Italy, Poland, the Netherlands and Austria

- PSA-Opel posted the second highest market share drop among car groups, with their registrations counting for 16.5% of the total market in February

The European car industry has continued to grow in February 2017 – with new car registrations for the month totalling 1.1 million units, a 1.2% increase when compared to February 2016. This is the second highest February volume recorded since 2008, but there are signs that market growth has started to slow. Notably, this growth is dramatically lower than the 14% growth recorded in February 2016.

Three of Europe’s largest five markets posted a drop in registrations, with France, Germany, and the UK all experiencing a decline. The largest decline was posted by France, where the significant increase in registrations of SUVs was not enough to offset the drops posted by MPVs and compact cars. Germany’s registrations decreased by 2.6%, and registrations for Diesel cars fell by 10.5% compared to February 2016. This means that Diesel cars account for 43.4% of the German car market, which is the lowest level since February 2010. The decline in German Diesel registrations began midway through 2016, and can be expected to continue over the upcoming months.

Of Europe’s largest five markets, Italy and Spain were the only two to increase car registrations. The Italian market has begun to cool off after years of dramatic growth – with an increase in registrations of 6.2%. Spain’s spring break will take place in April, which will likely cause an uptick in rental car purchases over March. Poland’s performance is particularly notable as it signals the 23rd month of growth for the country, with a boost in registrations coming from company purchases.

“Despite the recent declines in certain markets across Europe, the outlook for the industry is still positive. This slowdown is expected – as we saw dramatic increases in registrations as markets recovered from the European recession. We now anticipate growth slowing down, and the market to stabilise over the coming months. PSA’s declining market share is notable in light of recent news of the manufacturer’s takeover of Opel/Vauxhall. PSA stands to benefit from the European reach of Opel/Vauxhall, particularly in the UK and German markets. But it will be interesting to see how the two companies’ ranges are integrated and what impact this consolidation has on the industry,” commented Felipe Munoz, Global Automotive Analyst at JATO Dynamics.

VW Group retained its leading position, despite losing market share. Notably, VW Group sold more SUVs than midsize cars, with its Seat brand posting a huge increase thanks to the performance of its Ateca SUV model.

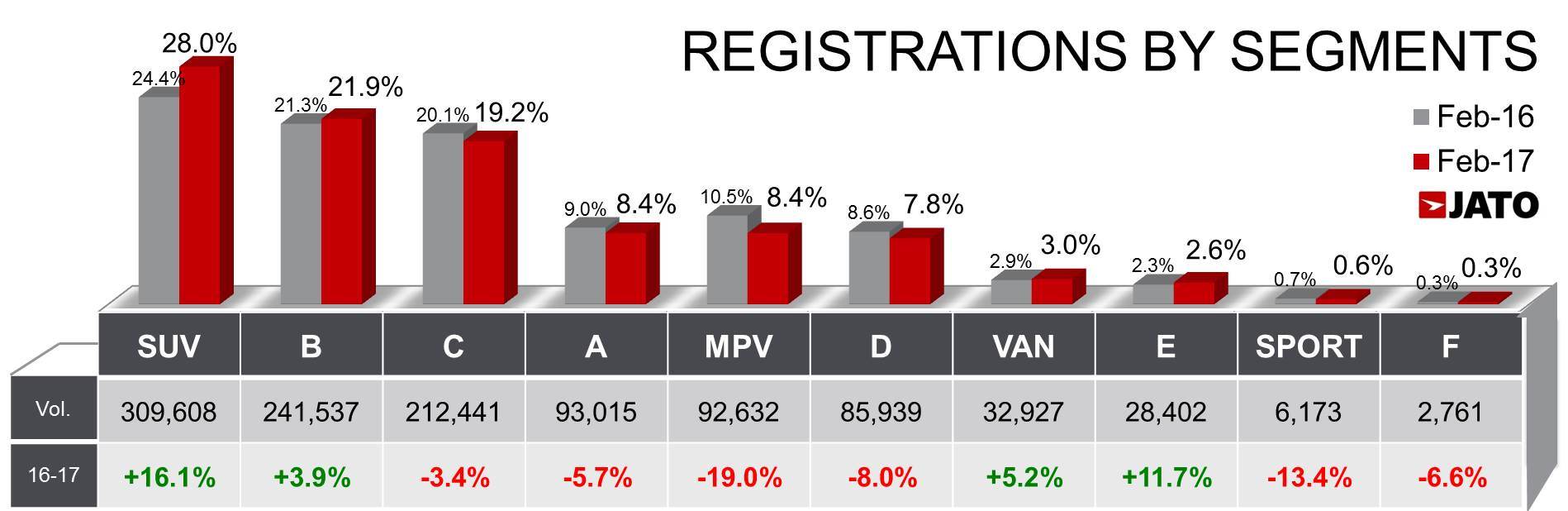

Both the SUV and Executive segment experienced double digit growth due to the performance of the latest launches – such as the VW Tiguan, Toyota C-HR, Mercedes E-Class and Volvo S90/V90.

Download file: march-2017-europe-reg-release-final.pdf